The 2025/26 self assessment tax return covers income earned between 6 April 2025 and 5 April 2026. If you received money during that period that wasn’t taxed at source — from self-employment, rental properties, savings above certain thresholds, or capital gains — you most likely need to file one. The online deadline is 31 January 2027. Miss it, and HMRC adds a £100 penalty immediately. No warnings issued. No grace period.

This guide covers every key date, who needs to file, what documents to gather, how to submit your return, and how to avoid the mistakes that cost people money every January. It also explains why 2025/26 is an especially significant return — for many sole traders and landlords, it may be the final traditional self assessment they ever submit.

For a broader overview of how tax returns fit into running a small business in the UK, see our guide to UK small business tax return obligations.

What Is the 2025/26 Tax Year?

The UK tax year runs from 6 April to 5 April the following year. The 2025/26 tax year ran from 6 April 2025 to 5 April 2026. Any income earned, expenses incurred, or gains made within those dates belong to this return. You are not reporting current earnings. You are reporting a period that has already closed.

Do You Need to File a 2025/26 Self Assessment Return?

Who Must File

You must file if any of the following applied to you during the 2025/26 tax year:

- You were self-employed with trading income above £1,000 (the trading allowance)

- You were a partner in a business partnership

- You were a company director receiving untaxed income

- Your total income exceeded £100,000

- You received rental income from UK or overseas property

- You had capital gains above the £3,000 annual exempt amount

- You received foreign income or held overseas investments

- You claimed Child Benefit and your income exceeded £60,000 (the High Income Child Benefit Charge)

- You had untaxed savings interest above £10,000

- HMRC wrote to you and formally asked you to file

If you’re still deciding how to structure your business, our comparison of running as a sole trader or limited company explains how your choice directly affects what and how you report to HMRC.

Who Does Not Need to File

If all your income came through PAYE and you earned under £100,000, you probably don’t need to file. But check carefully. HMRC won’t always tell you when you should have. The legal responsibility to register sits entirely with you.

Key Deadlines for 2025/26

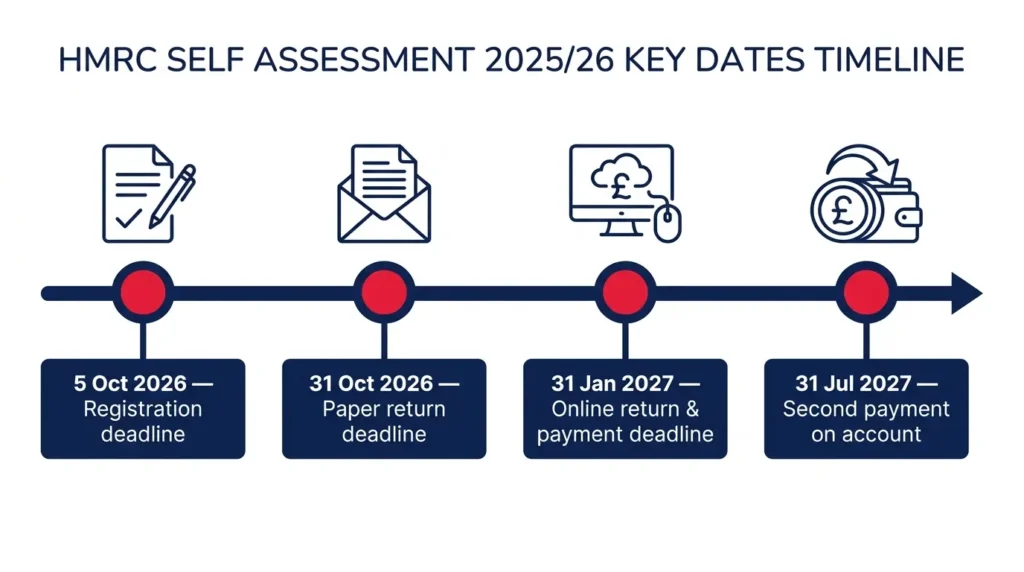

Registration Deadline: 5 October 2026

New to self assessment? You must register with HMRC by 5 October 2026. Self-employed individuals use form CWF1. Those with other untaxed income register via SA1. Business partners use SA401. After registering, allow 10–15 working days for HMRC to post your 10-digit Unique Taxpayer Reference (UTR). You cannot file without it, so do not leave this to the last minute.

Paper Return Deadline: 31 October 2026

Paper SA100 returns must reach HMRC by 31 October 2026. Filing online gives you three extra months. It also reduces errors significantly — the HMRC system calculates your bill automatically. After 31 October 2026, paper submissions are only accepted in exceptional circumstances with documented evidence.

Online Return and Payment Deadline: 31 January 2027

This is the critical date. Your online return must be submitted and any balancing tax payment must reach HMRC by 31 January 2027. Both fall on the same day. Filing early means you know your bill months in advance — which matters considerably if the number is larger than you expected.

Second Payment on Account: 31 July 2027

If you make payments on account (see below), your second instalment is due 31 July 2027.

What Documents Do You Need?

Gather these before opening HMRC’s online system:

- Your 10-digit UTR number and National Insurance number

- P60 or P45 from any employer during 2025/26

- P11D if you received any employee benefits

- Self-employment income records and expense receipts

- Bank statements showing savings interest received

- Dividend vouchers from any shares held

- Rental income and landlord expense records

- Capital gains calculations and disposal records

- Pension contribution statements

- Gift Aid donation totals

- Details of any Child Benefit payments received

Good records throughout the year make this process take two hours. Poor records make it take days — and risk mistakes that invite HMRC scrutiny. For practical guidance on setting up a simple record-keeping system, our small business accounting tips for UK owners covers the basics clearly.

How to Register and Get Your UTR

Visit GOV.UK and complete the registration form that fits your situation. Most self-employed people use CWF1. HMRC will post your UTR within 10 working days. Once it arrives, log into your Government Gateway account at gov.uk and activate your self assessment profile.

Do not wait until September or October. HMRC’s phone lines are overloaded in autumn. Postal delays happen. Starting early protects your deadline.

How to File Your Return

Online via Government Gateway

Go to gov.uk/log-in-file-self-assessment-tax-return. The system saves your progress automatically — you can leave and return before submitting. Once submitted, HMRC shows your calculated tax bill immediately and issues a confirmation reference number.

SA100 and Supplementary Pages

The main return is the SA100. Supplementary pages are added depending on your income sources:

- SA103 — self-employment income and expenses

- SA105 — UK rental property income

- SA104 — partnership income

- SA106 — foreign income

- SA108 — capital gains

HMRC’s online system generates the right pages based on your answers. You do not have to select them manually.

Allowable Expenses That Reduce Your Tax Bill

Allowable expenses reduce your taxable profit — which directly reduces what you pay. Only expenses that are wholly and exclusively for business purposes qualify. Common ones for self-employed people include:

- Office supplies, software subscriptions, and business phone costs

- Business mileage at 45p per mile for the first 10,000 miles, 25p after

- Use of home as office (HMRC flat rate or a calculated proportion)

- Professional subscriptions and job-specific training

- Staff wages and subcontractor fees

- Stock, materials, and equipment

For landlords, allowable expenses include letting agent fees, repairs (not improvements), landlord insurance, and a 20% basic rate tax credit on mortgage interest.

Claiming the right expenses can make a substantial difference to your bill. For more strategies across the full tax year, see our guide to smart tax strategies for small businesses.

Understanding Your Tax Bill: Rates and a Worked Example

2025/26 Income Tax Bands

| Band | Taxable Income | Rate |

|---|---|---|

| Personal allowance | Up to £12,570 | 0% |

| Basic rate | £12,571 – £50,270 | 20% |

| Higher rate | £50,271 – £125,140 | 40% |

| Additional rate | Above £125,140 | 45% |

National Insurance for Self-Employed

Class 2 NI was abolished from April 2024. For 2025/26, self-employed people pay only Class 4 NI: 6% on profits between £12,570 and £50,270, then 2% above that. No flat weekly charge applies.

Worked Example

A sole trader with £45,000 turnover and £8,000 allowable expenses has taxable profit of £37,000.

- Income tax: (£37,000 – £12,570) × 20% = £4,886

- Class 4 NI: (£37,000 – £12,570) × 6% = £1,466

- Total self assessment bill: approximately £6,352

Any payments on account made in the previous year reduce the January balancing payment.

Payments on Account Explained

If your self assessment bill exceeds £1,000 and less than 80% of your income was taxed at source, HMRC requires payments on account. These are advance payments toward next year’s expected tax liability.

Two instalments are due: the first on 31 January 2027 (paid alongside your balancing payment) and the second on 31 July 2027. Each is 50% of your prior year’s tax bill.

If your income will be significantly lower next year, you can apply to reduce payments on account using form SA303. Overpaying is not money lost — HMRC refunds it — but it does hit your cash flow hard in January.

Managing cash flow ahead of your tax bill becomes far easier when you plan for both the balancing payment and the first POA as a single January cost.

HMRC Penalties for Late Filing and Late Payment

Filing Penalty Schedule

| Delay | Penalty |

|---|---|

| 1 day late | £100 automatic penalty |

| 3 months late | £10 per day, up to 90 days (max £900 additional) |

| 6 months late | 5% of tax due or £300 — whichever is greater |

| 12 months late | Further 5% of tax due or £300 — whichever is greater |

Payment Penalties

Late payment attracts daily interest on the outstanding amount. After 30 days, HMRC adds a 5% surcharge. Further surcharges of 5% apply at six months and twelve months. These accumulate.

If you genuinely cannot pay by 31 January 2027, contact HMRC before the deadline — not after. A Time to Pay arrangement spreads the debt into monthly instalments. Interest still accrues, but the surcharges do not apply when you arrange this proactively.

Keep your expense records clean and accurate year-round. Errors and overclaims are the most common triggers for HMRC enquiries. Understanding how HMRC tax audits work helps you stay prepared if one ever lands.

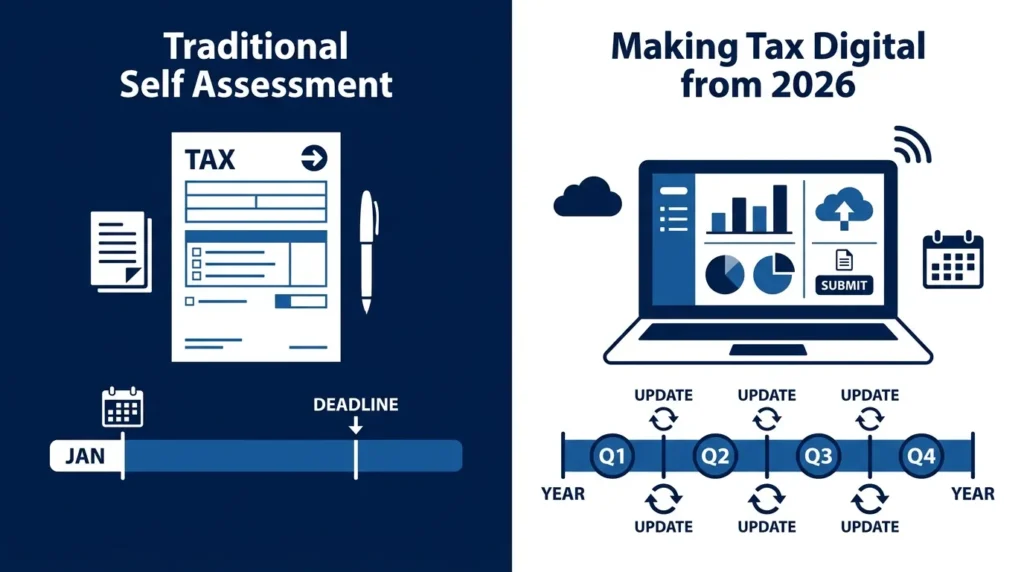

Making Tax Digital — Why 2025/26 Matters

From 6 April 2026, Making Tax Digital for Income Tax (MTD for ITSA) became mandatory for self-employed individuals and landlords with combined gross income above £50,000. For those people, the 2025/26 return is the last traditional self assessment they will ever submit.

The 2025/26 return itself is still filed under the standard SA system. The 31 January 2027 deadline applies as normal. But from the 2026/27 tax year onward, taxpayers above the £50,000 threshold must use MTD-compatible accounting software and submit quarterly digital updates to HMRC. The annual January filing is replaced by four quarterly submissions plus a year-end declaration.

The threshold drops to £30,000 from April 2027, drawing more taxpayers into mandatory MTD. If your income sits between £30,000 and £50,000, your next traditional SA deadline will be January 2028 — not 2027.

One thing MTD does not change: payment dates. Payments on account still fall on 31 January and 31 July. That part of the system stays the same.

Common Mistakes That Cost Money

Forgetting smaller income sources. Bank interest, dividend payments, and occasional freelance income all count. HMRC receives data directly from banks and companies — discrepancies flag your return for review.

Overclaiming expenses. Including personal costs as business ones is the fastest route to an HMRC compliance check. When in doubt, leave it out.

Missing the HICBC. If you or your partner received Child Benefit and either of you earned above £60,000, you owe the High Income Child Benefit Charge. Many people only find out when HMRC writes to them — often years later, with interest added.

Underestimating the January bill. First-time filers often don’t account for payments on account. In January, you may owe your balancing payment for 2025/26 plus the first POA for 2026/27 — potentially 150% of what you expected.

Property capital gains reporting errors. Gains from UK residential property require a separate 60-day CGT return filed with HMRC and inclusion on your self assessment return. Not one or the other — both.

Filing without paying. Submitting your return on time is only half the obligation. If the tax remains unpaid, HMRC’s payment penalties apply regardless.

Frequently Asked Questions

Can I file my 2025/26 return already? Yes. HMRC opened the 2025/26 return window on 6 April 2026. Filing early means you know your bill months before the payment deadline — which is useful for cash flow planning.

What if I can’t pay by 31 January 2027? Contact HMRC before the deadline. A Time to Pay arrangement allows monthly payments. Interest applies, but the 5% surcharges do not when you arrange this proactively and in advance.

Does MTD mean I skip my 2025/26 return? No. Even if you are now filing quarterly under Making Tax Digital, your 2025/26 self assessment return must still be submitted by 31 January 2027 in the traditional format.

Where do I find my UTR number? Your Unique Taxpayer Reference appears on previous HMRC letters, past tax returns, and within your Government Gateway account. If you’ve lost it, HMRC can reissue it — but allow time for this.

Are accountant fees tax-deductible? Yes. Fees paid for preparing your self assessment return are an allowable business expense. They reduce your taxable profit for the year in which they are paid.

{kind=link}