If your business’s annual pay bill is over £3 million, you’re liable for the Apprenticeship Levy — and from 2026, you’re dealing with its replacement, the Growth and Skills Levy. If your pay bill is under that threshold, you don’t pay it, but you still have access to funding for hiring and training apprentices, and some of that funding just got a lot more generous.

This guide walks through exactly who pays, how the calculation works, and what’s changed for 2026 — including several updates that most guides online still haven’t caught up with.

Quick answer: Does the Apprenticeship Levy apply to me? Yes, if your business’s annual pay bill exceeds £3 million, or you’re part of a connected group of companies or charities whose combined pay bill exceeds £3 million. If it doesn’t, you’re a non-levy payer, and a different funding system applies to you instead.

What is the UK Apprenticeship Levy?

The Apprenticeship Levy is a payroll charge on large UK employers, introduced in 2017 to fund apprenticeship training. Employers who owe it pay 0.5% of their annual pay bill, collected monthly through PAYE, into a digital account they use to pay for apprenticeship training and assessment.

It isn’t optional and it isn’t linked to whether you actually employ any apprentices. If your pay bill crosses the threshold, HMRC collects the levy regardless. Employers who never draw down the funds effectively lose them once they expire.

The Transition to the Growth and Skills Levy

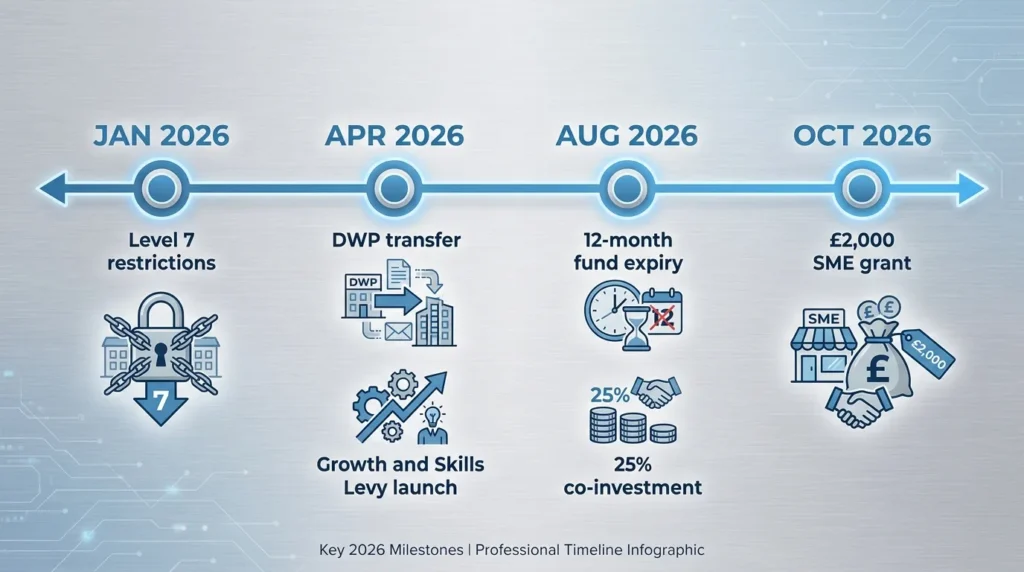

From 1 April 2026, the Apprenticeship Levy is being rebranded and restructured as the Growth and Skills Levy. The 0.5% rate and £3 million threshold haven’t changed. What has changed is flexibility: employers can now spend a portion of their funds on shorter “apprenticeship units” — modular courses lasting roughly 30 to 140 hours, in areas like AI, digital skills and engineering — rather than committing solely to full apprenticeship programmes.

Responsibility for the levy also moved departments. On 1 April 2026, apprenticeship policy transferred from the Department for Education (DfE) to the Department for Work and Pensions (DWP), as part of a wider machinery-of-government change. Day-to-day compliance is unaffected, but guidance, funding rules and the account portal now sit under the DWP.

Does the Apprenticeship Levy Apply to My Business? (The £3M Threshold)

You pay the levy if your annual pay bill is more than £3 million. This applies UK-wide, regardless of sector, business structure, or whether you’re a private company, public body, or charity. There’s no partial liability below that line — if your pay bill sits at £2.9 million, you owe nothing.

How the £15,000 Levy Allowance Works

Every liable employer gets a £15,000 annual allowance to offset against their levy bill. In practice, this means the levy only bites once your pay bill exceeds £3 million, because 0.5% of £3 million is exactly £15,000.

The allowance isn’t applied as one lump sum at the end of the year. It builds up monthly, at £1,250 (one-twelfth of £15,000), and offsets your levy liability cumulatively as you go. This detail matters for businesses with seasonal payroll swings — a spike in one month’s pay bill can trigger a levy charge that month even if your annual figure would otherwise stay under threshold, though any overpayment is corrected as the allowance accumulates across the tax year.

The Connected Companies Rule: Sharing the Allowance

If your business is part of a group of connected companies or charities, you don’t each get your own £15,000 allowance. The group must decide, at the start of the tax year, how to split a single £15,000 allowance between the connected entities — and that split must be declared to HMRC and can’t be changed until the following tax year.

Companies are “connected” for levy purposes broadly where one has control over another, using the same test HMRC applies for Employment Allowance. This catches parent-subsidiary structures and franchise groups more often than business owners expect, and getting the allocation wrong is a common compliance trip-up. If you’re restructuring or setting up a group, it’s worth reviewing how your company structure affects tax obligations before the new tax year starts.

How to Calculate Your Apprenticeship Levy Liability

Direct answer: Your monthly levy liability is 0.5% of that month’s pay bill, minus your monthly share of the £15,000 allowance (usually £1,250), calculated cumulatively across the tax year.

What Counts Towards Your “Annual Pay Bill”?

Your pay bill is based on the total earnings on which you pay Class 1 secondary National Insurance contributions (NICs) — the employer’s share, not the employee’s.

Included:

- Salaries and wages

- Bonuses and commissions

- Pension contributions that are subject to Class 1 NICs

- Most other earnings liable to Class 1 secondary NICs

Excluded:

- Benefits in kind (these fall under Class 1A NICs, not Class 1)

- Earnings of employees under 16

- Earnings not subject to UK National Insurance (for example, some overseas workers)

This distinction trips up a lot of employers, particularly around benefits in kind and pension contributions — get your employer National Insurance calculations right first, since your pay bill figure flows directly from them.

Step-by-Step Calculation Formula and Example

- Calculate your total annual pay bill (Class 1 secondary NIC earnings).

- Multiply by 0.5% to get your gross levy liability.

- Subtract your £15,000 annual allowance (or your allocated share if part of a connected group).

- The result is your annual levy liability, paid monthly and adjusted cumulatively.

Worked example: A business with an annual pay bill of £4,000,000.

- Levy at 0.5%: £20,000

- Minus the £15,000 allowance: £5,000

- Annual levy payable: £5,000, or roughly £416 a month after the allowance is applied

How to Pay and Report Your Levy Contributions

You don’t submit a separate levy return. The levy is calculated and paid automatically through your existing payroll process.

- Report your pay bill and levy liability through your normal Real Time Information (RTI) submission to HMRC each pay period.

- Where applicable, declare any adjustments through the Employer Payment Summary (EPS) — for example, if you’re part of a connected group, you use the EPS to confirm your share of the shared allowance.

- HMRC collects the levy alongside your other PAYE liabilities, such as Income Tax and NICs.

- Funds appear in your Growth and Skills Levy digital account (the Digital Apprenticeship Service, or DAS, account) roughly a month after your PAYE payment, ready to spend with a training provider on the Register of Apprenticeship Training Providers (RoATP).

If your payroll processes aren’t set up to track this accurately, it’s worth reviewing your payroll and PAYE reporting workflow so levy calculations aren’t an afterthought each month.

What If You Don’t Meet the Threshold? (Rules for SMEs and Non-Levy Payers)

If your pay bill is under £3 million, you don’t pay the levy — but you’re not excluded from apprenticeship funding. Non-levy payers access government support directly, without needing a DAS account balance to draw from.

Fully Funded Training for Under-25s

From the 2026/27 academic year, apprenticeship training for apprentices aged under 25 is fully funded by government for non-levy paying employers. You pay nothing towards the training costs for these apprentices — a significant improvement on the previous co-investment model, and one of the more generous parts of the 2026 reforms.

There’s also a new incentive: from 1 October 2026, non-levy paying employers can claim a payment of up to £2,000 when they recruit a new apprentice aged 16 to 24, provided the apprentice joined the business within the previous three months. It’s paid in two instalments, the first once the apprentice completes 90 days.

The Co-Investment System for Older Apprentices

For apprentices aged 25 and over, non-levy paying employers still use co-investment: government covers the majority of the training cost, and you pay the remainder directly to the training provider. This system remains broadly unchanged for 2026, so it’s the under-25 funding that represents the real shift for SMEs.

Levy Payers vs Non-Levy Payers: 2026 Comparison

| Levy Payers (Pay Bill over £3m) | Non-Levy Payers (SMEs) | |

|---|---|---|

| Levy rate | 0.5% of pay bill, minus £15,000 allowance | Not applicable |

| Funding for under-25 apprentices | Draws down from DAS account | 100% government funded from 2026/27 |

| Funding for apprentices 25+ | Draws down from DAS account | Government co-investment, employer pays remainder |

| Fund expiry | 12 months for funds accrued from August 2026 | Not applicable |

| New hiring incentive | Not applicable | Up to £2,000 grant per apprentice aged 16–24, from October 2026 |

| Managing body | DWP (from April 2026) | DWP (from April 2026) |

Critical 2026 Levy Changes Every Employer Must Know

The Move to the Department for Work and Pensions (DWP)

As of 1 April 2026, apprenticeship policy and funding sit with the DWP rather than the DfE, reflecting the government’s push to link skills funding more directly with employment outcomes. Guidance documents and the funding rules are now published under the DWP.

Shorter Expiry Window for Unused Funds (12 Months)

This is the change catching the most employers out. Funds entering your account from August 2026 onward expire after 12 months, down from the previous 24. Money you don’t commit to training within a year is lost. If your business has historically let levy funds accumulate and expire unused, this window closing faster makes proactive budget planning essential — treat your DAS balance the same way you’d treat any other deductible business expense with a use-it-or-lose-it deadline.

Removal of the 10% Government Top-Up

Previously, government added a 10% top-up to whatever employers paid into their levy account. From August 2026, that top-up is being removed, meaning employers get back only what they pay in, before any training costs are drawn down.

Increased Co-Investment Rates for Exhausted Accounts

If a levy-paying employer exhausts their account balance and needs to fund additional apprenticeship training directly, the co-investment rate they pay is rising from 5% to 25% for starts from August 2026. Government covers the remaining 75%. This is a substantial jump, and it changes the maths on whether it’s worth stretching your levy balance across more apprentices or fewer, higher-value ones.

How to Access and Spend Your Levy Funds Across the UK

Levy-paying employers manage their funds through their Growth and Skills Levy digital account, spending them with approved training providers on apprenticeship training, assessment, and — since April 2026 — apprenticeship units. Employers can also transfer up to 50% of their annual levy funds to other businesses, including smaller firms in their supply chain, which is a practical way to support SME partners who don’t have their own levy pot.

Devolved Nations: Variations in Scotland, Wales, and Northern Ireland

The levy is collected UK-wide, but how the money is spent is devolved. If you employ people in Scotland, Wales, or Northern Ireland, the proportion of your levy pot allocated to those nations is managed separately:

- England: Managed through your DAS account with the DWP.

- Scotland: Managed by Skills Development Scotland (SDS), which runs its own apprenticeship system rather than the DAS.

- Wales: Managed by the Welsh Government, with funding routed through its own apprenticeship programme.

- Northern Ireland: Managed by the Department for the Economy.

If you employ staff across more than one nation, your levy contribution is apportioned based on the home address of each employee, so your usable funds in England may be smaller than your total UK levy payment suggests.

Common Mistakes and Compliance Risks

- Miscalculating the pay bill by including benefits in kind, which belong under Class 1A NICs, not Class 1.

- Letting connected company allowances go undeclared, which can trigger HMRC queries during a payroll audit.

- Assuming last year’s 24-month expiry still applies, and losing funds that expire after 12 months under the new rules.

- Ignoring apprenticeship units as a way to use up funds that would otherwise expire before a full apprenticeship could start.

- Underestimating the 25% co-investment jump, which can make budget planning for the next intake noticeably more expensive from August 2026.

Summary and Checklist: Your Next Steps

- Confirm whether your pay bill exceeds £3 million — alone or combined with any connected companies.

- If liable, check your PAYE and RTI reporting correctly reflects your monthly levy calculation.

- If part of a group, confirm your allowance split has been declared for the current tax year.

- Review your DAS account balance and flag any funds due to expire under the new 12-month rule.

- If you’re a non-levy payer hiring under-25s, check eligibility for 100% funded training and the new £2,000 hiring grant from October 2026.

- Budget for the rise in co-investment to 25% if you expect to exhaust your levy account after August 2026.

Frequently Asked Questions

Is the Apprenticeship Levy a tax? It’s a mandatory payroll charge collected through PAYE, functioning like a tax, though HMRC and government literature describe it as a levy rather than a general tax since the funds are ring-fenced for apprenticeship training.

What happens to unused Apprenticeship Levy funds? Funds you don’t spend within the expiry window are lost. From August 2026, that window is 12 months for new funds, down from 24.

Do small businesses pay the Apprenticeship Levy? No. Only employers with an annual pay bill over £3 million pay it. Smaller businesses access apprenticeship funding through co-investment or, for under-25s from 2026/27, full government funding.

Can I transfer my levy funds to another business? Yes, up to 50% of your annual levy funds can be transferred to other employers, including smaller supply chain partners.

Managing apprenticeship costs alongside the rest of your payroll and HR admin is easier with the right systems in place — if you’re reviewing your setup, it’s worth comparing HR software built for UK small businesses and checking how apprentice pay rates align with the National Minimum Wage rules, since apprentice rates follow their own separate band. For SMEs weighing up whether to bring on an apprentice at all, our guide to apprenticeships for UK small businesses covers the practical hiring side in more detail, and it’s worth factoring training costs into your wider corporation tax planning too.

{kind=link}