The way you report your taxes in the UK is changing. HM Revenue and Customs (HMRC) is introducing a new system. It is called Making Tax Digital for Income Tax Self Assessment. This new system replaces the traditional annual tax return for many self-employed individuals and landlords. Instead of filing once a year, you will need to keep digital records and send updates every three months.

What is Making Tax Digital for Income Tax?

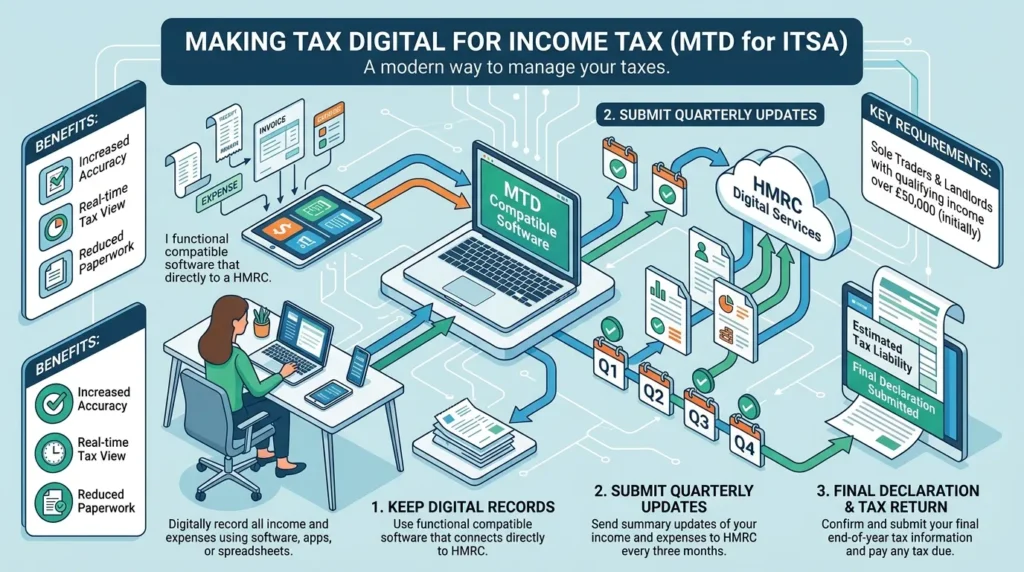

Making Tax Digital is a government plan to modernise the tax system. The goal is to make tax reporting more accurate and reduce manual mistakes.

Under the old system, you collected all your paper receipts and invoices at the end of the year. Then, you filled out a single Self Assessment tax return by January 31.

Under the new system, paper books are no longer enough. You must use software that connects directly to HMRC. You will use this software to:

- Record every business sale and expense digitally.

- Send a summary of your income and costs to HMRC every quarter.

- Submit a final declaration at the end of the tax year to fix your total tax bill.

Your actual tax payment deadlines will not change. You will still pay your tax bills by January 31 and July 31 each year.

Who Must Follow the New Rules?

The new rules apply to sole traders, self-employed individuals, and landlords who are registered for Self Assessment. However, the system is starting in stages based on your total annual gross income. Gross income means your total earnings before you subtract any expenses.

If you have multiple businesses or rent out multiple properties, you must add all these income sources together to find your total gross income.

The Income Thresholds and Timelines

The rollout moves in three main phases:

- From 6 April 2026: You must follow the rules if your total gross income from self-employment and property was over £50,000 in the 2024/25 tax year.

- From 6 April 2027: You must follow the rules if your total gross income is over £30,000.

- From 6 April 2028: The government plans to lower the threshold to include everyone making over £20,000.

If your income is below these amounts, you do not have to join yet. You can still choose to sign up early on a voluntary basis to practice using the system.

Key Deadlines for Your Calendar

If you match the £50,000 threshold, your digital tracking begins on 6 April 2026. You will have to submit four quarterly updates. Each update is a running total of your income and expenses from the start of the tax year.

Quarterly Update Deadlines

You must submit each quarterly report by the 7th day of the second month after the period ends. Here are the exact deadlines for the tax year:

- Quarter 1 (6 April to 5 July): Deadline is 7 August.

- Quarter 2 (6 July to 5 October): Deadline is 7 November.

- Quarter 3 (6 October to 5 January): Deadline is 7 February.

- Quarter 4 (6 January to 5 April): Deadline is 7 May.

After these four updates, you must submit your final declaration by 31 January of the following year. This final step replaces the old tax return.

What Do You Need to Do to Prepare?

To get ready for the new system, you should take action early. Do not wait until the first deadline to set up your workflow.

First, look at your past tax returns to check your gross income. This tells you exactly when you must join the system.

Second, select an HMRC-approved software tool. You cannot use normal spreadsheets unless they link to HMRC through special software. The software should link directly to your business bank account to track money automatically.

Third, start recording your receipts and invoices digitally right away. Getting into the habit of updating your records every week will save you time later.

How Do Penalties Work?

HMRC is changing how they punish late submissions. They are introducing a points-based system.

If you miss a quarterly deadline, you will receive one penalty point. You will not get an automatic financial fine for your first few mistakes. However, if you collect too many points, you will face a fixed financial fine. For quarterly filers, the fine applies once you reach four points. The current fine amount is £200.

The points can reset back to zero if you submit all your updates on time for a specific period. This system gives you a chance to learn the new process without facing immediate heavy fines. Note that standard late payment penalties still apply if you do not pay your actual tax bill on time.

Final Thoughts

Making Tax Digital changes how self-employed workers and landlords manage their accounts. Moving from a single yearly task to regular quarterly updates requires a change in your routine. By choosing the right software early and tracking your numbers every week, you can keep your records accurate and avoid penalty points. This regular review will also help you understand your business cash flow much better throughout the year.

{kind=link}