If your rates bill looks different this year, the 2026 revaluation is almost certainly why. Every non-domestic property in England had its rateable value reassessed from 1 April 2026, using rental values from 1 April 2024. That single change has knocked some businesses out of Small Business Rates Relief altogether, while others have picked up relief for the first time. This guide sets out exactly where you stand.

What is Small Business Rates Relief (SBRR)?

Small Business Rates Relief is a discount on your business rates bill, available to ratepayers who occupy one main property (or, in limited cases, more than one) below a set rateable value. It’s administered by your local council under Section 47 of the Local Government Finance Act 1988, using rateable values set by the Valuation Office Agency (VOA). At its most generous, it removes your rates bill entirely.

Your rateable value isn’t your rent. It’s the VOA’s estimate of the property’s annual open market rental value on a fixed valuation date — for the current list, that’s 1 April 2024. You can look yours up for free via the GOV.UK Find a Business Rates Valuation service.

Small Business Rates Relief Eligibility & Thresholds for 2026/27 (England)

Quick answer: properties with a rateable value up to £12,000 get 100% relief. Between £12,001 and £14,999, relief tapers down to zero. Above £15,000, SBRR doesn’t apply, though other support may.

Under £12,000 Rateable Value: 100% Relief

If your only property has a rateable value of £12,000 or less, you pay nothing in business rates, provided you apply through your local council. This threshold has held since April 2017 and wasn’t changed by the 2026 revaluation — what changed is which properties now fall under it.

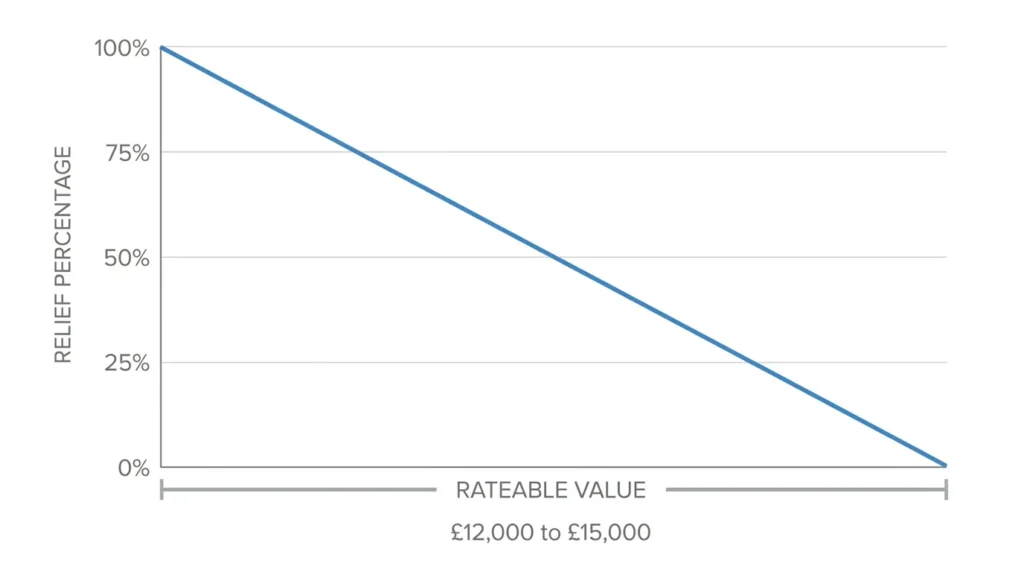

£12,001 to £15,000 Rateable Value: Tapered Relief

Relief reduces by roughly 1% for every £30 of rateable value above £12,000. So a property with a rateable value of £13,500 sits halfway between the two thresholds and gets 50% relief.

| Rateable Value | Approx. Relief |

|---|---|

| £12,000 | 100% |

| £12,750 | ~75% |

| £13,500 | ~50% |

| £14,250 | ~25% |

| £15,000 | 0% |

Over £15,000 Rateable Value: What Are Your Options?

You lose SBRR entirely above £15,000, but you’re not necessarily paying full whack. If your rateable value stays below £51,000, you’re still billed on the lower small business multiplier rather than the standard one — a saving worth having even without relief. Properties that just tipped over the SBRR threshold because of the revaluation should also check the Supporting Small Business Relief scheme covered below, and retail, hospitality or leisure businesses should check whether they now qualify for the lower RHL multiplier instead.

SBRR Rules for Multiple Properties: The New 3-Year Grace Period

You can still claim SBRR on your main property if you occupy others, as long as each additional property has a rateable value below £2,900 and the combined rateable value of everything you occupy is under £20,000 (£28,000 if you’re in Greater London).

The bigger change is what happens if you take on a second property that breaches those limits. Previously, you kept your existing relief for just 12 months before losing it. Following the Autumn Budget on 26 November 2025, that grace period has been extended to three years for any property taken on from 27 November 2025 onwards. If you took on the second property before that date, the old 12-month grace period still applies. This is a genuine gap in a lot of the advice still circulating online — plenty of guides haven’t caught up with the change.

The 2026 Revaluation: How Does It Impact Your Rates?

Every three years, the VOA updates rateable values across England and Wales to reflect current rents. The 2026 revaluation, effective from 1 April 2026, uses rental evidence from 1 April 2024 — meaning your new bill reflects rents from two years before it started applying.

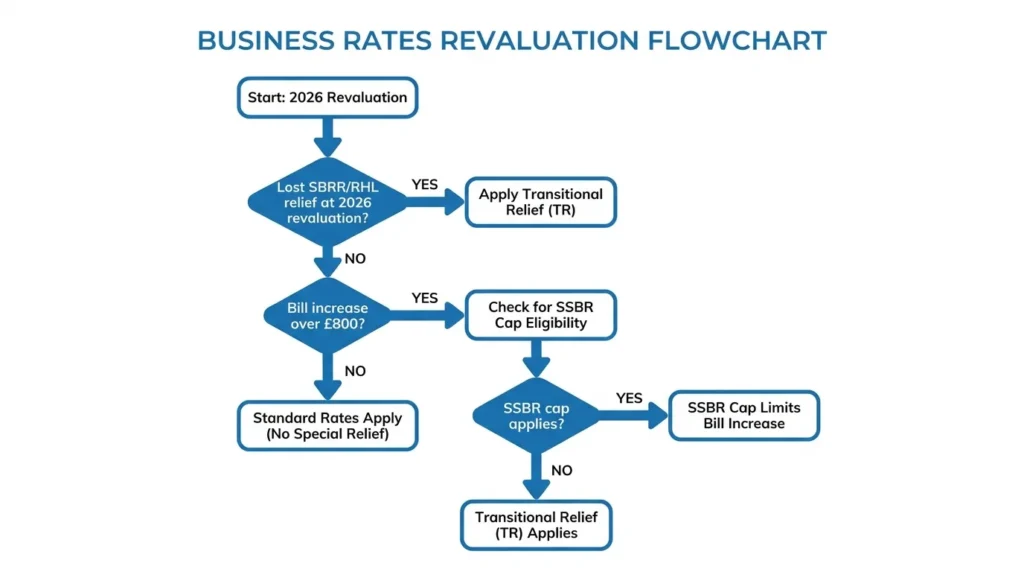

If your rateable value rose sharply, you might have crossed the £12,000 or £15,000 threshold and lost some or all of your SBRR. If it fell, you may have gained relief you didn’t have before, or moved from tapered to full relief. Either way, the change isn’t backdated to your circumstances before 1 April 2026 — it takes effect from the date the new list applies, or from whenever your rateable value is later corrected on appeal.

To cushion sudden increases, the government has also brought in a redesigned Transitional Relief scheme, capping bill rises for 2026/27 at 5% for smaller properties (rateable value up to £20,000), 15% for medium properties (£20,001–£100,000), and 30% for larger ones (above £100,000). This is applied automatically, before other reliefs.

Supporting Small Business Relief (SSBR) 2026: Protecting Lost Relief

Quick answer: if you lost some or all of your SBRR because of the 2026 revaluation, SSBR caps how much your bill can rise this year — at whichever is higher: £800, or the relevant Transitional Relief percentage cap.

Who Qualifies for the 2026 SSBR Scheme?

You’re covered if, because of the revaluation, you’ve lost some or all of your Small Business Rates Relief, Rural Rate Relief, or retail, hospitality and leisure relief you were getting in 2025/26. It’s applied automatically by your local council to your account — you don’t need to apply.

How the £800 Annual Bill Increase Cap Works

Say a business loses 100% SBRR entirely from 1 April 2026. Rather than facing the full new bill in one jump, SSBR limits the increase to £800 for the year (or more, if the Transitional Relief percentage cap for their property size works out higher). The government funds councils to apply this cap via the calculation set out in the Non-Domestic Rating (Chargeable Amounts) (England) Regulations 2026, so there’s no separate transitional relief supplement stacked on top — you don’t pay £800 plus extra charges.

Rules for Transitioning from the 2023 SSBR Scheme

If you were already receiving Supporting Small Business Relief under the 2023 scheme on 31 March 2026, that support has been extended for one further year and your eligibility for the 2026 SSBR runs out on 31 March 2027. Everyone else moving into the 2026 scheme stays protected until they either reach the bill they’d pay without relief, or for up to three years, whichever comes first.

One caveat worth knowing about: if you lose eligibility for the 2026 SSBR scheme for even a single day — other than becoming empty and getting empty property relief — you can’t re-enter it later if your circumstances change again.

Because these reliefs count as subsidies, there’s a ceiling on how much any one business (including group companies) can receive: £315,000 in Minimal Financial Assistance under the Subsidy Control Act across the 2026/27 year and the two years before it. Most small businesses never get close to this, but it matters if you’re claiming relief across several trading entities.

Small Business Rates Relief in Scotland, Wales, and Northern Ireland

Business rates are devolved, so if you’re outside England, different rules apply entirely.

| Nation | Scheme | 100% Relief Threshold | Tapered Relief Band |

|---|---|---|---|

| England | SBRR | Up to £12,000 RV | £12,001–£14,999 |

| Scotland | Small Business Bonus Scheme | Up to £12,000 RV | £12,001–£20,000 |

| Wales | Non-Domestic Rates Relief | Up to £6,000 RV | £6,001–£12,000 |

| Northern Ireland | SBRR (NAV-based) | No 100% band | £2,001–£15,000 (20–25% relief); up to 50% under £2,000 |

Scotland: the Small Business Bonus Scheme gives 100% relief up to £12,000 rateable value, tapering to zero at £20,000. If you occupy more than one property, you can still get relief where each has a rateable value of £20,000 or less and the combined total across all your properties doesn’t exceed £35,000.

Wales: relief is 100% up to £6,000 and tapers to zero at £12,000 — noticeably lower thresholds than England. It’s capped at a maximum of two qualifying properties per business within each local authority area, and Wales runs its own three-tier multiplier system (0.350 retail, 0.502 standard, 0.515 for properties above £100,000).

Northern Ireland: SBRR is based on Net Annual Value (NAV) rather than rateable value, and there’s no 100% band. Properties with an NAV up to £2,000 get 50% relief, £2,001–£5,000 gets 25%, and £5,001–£15,000 gets 20%. It’s applied automatically — no application needed.

2026/27 Business Rates Multipliers (The 5-Multiplier System)

England moved from two multipliers to five from 1 April 2026, under the Non-Domestic Rating (Multipliers and Private Schools) Act 2025. Which one applies depends on your rateable value and whether your property qualifies as retail, hospitality or leisure (RHL).

| Multiplier | Rate | Applies to |

|---|---|---|

| Small business RHL | 38.2p | RHL properties, RV below £51,000 |

| Small business (standard) | 43.2p | Non-RHL properties, RV below £51,000 |

| Standard RHL | 43p | RHL properties, RV £51,000–£499,999 |

| Standard | 48p | Non-RHL properties, RV £51,000–£499,999 |

| High-value | 50.8p | All properties, RV £500,000 and above |

If you don’t receive Transitional Relief or SSBR, a 1p supplement is added to your multiplier for 2026/27 only, to help fund the Transitional Relief scheme. It’s shown separately on your bill but doesn’t apply if you’re already getting one of those reliefs.

How to Check Your Rateable Value & Secure Your Relief

- Look up your rateable value using the GOV.UK Find a Business Rates Valuation service — search by postcode or address.

- Check it against the thresholds above for your nation, to see whether you qualify for full or tapered relief.

- Apply through your local council, not central government — SBRR in England isn’t automatic; you need to submit an application, though SSBR and Transitional Relief are applied automatically.

- Challenge the valuation if it looks wrong, via your VOA Business Rates Valuation Account, before your relief entitlement is locked in for the year.

- Report changes within four weeks — taking on a new property, extending your premises, or a change of use can all affect your relief, and late reporting can mean losing relief you were entitled to.

Getting your rates position right matters for cash flow planning generally — it’s worth reading alongside our broader guide to business rates relief in the UK and our cash flow tips for UK small businesses if you’re managing a tight budget through the transition.

Frequently Asked Questions (FAQs)

How do I qualify for Small Business Rate Relief in 2026?

In England, you qualify with a rateable value up to £15,000 on your main property (100% relief below £12,000, tapered above it), provided any additional properties stay under the £2,900/£20,000 combined limits.

What are the business rate thresholds for 2026/27?

100% relief up to £12,000 RV, tapered relief from £12,001 to £14,999, no SBRR from £15,000, though the small business multiplier still applies below £51,000.

What happens to my relief if my rateable value went up at the 2026 revaluation?

You may lose some or all of your SBRR, but the Supporting Small Business Relief scheme caps your bill increase at the higher of £800 or the relevant Transitional Relief percentage cap for 2026/27.

Can I get business rates relief on a second shop?

Yes, if the second property has a rateable value under £2,900 and your combined rateable value stays under £20,000 (£28,000 in London). If you exceed these limits, you keep existing relief on your main property for three years if you took on the second property from 27 November 2025 onwards.

Do I need to apply for Small Business Rates Relief, or is it automatic?

SBRR itself needs an application through your local council. SSBR and Transitional Relief are applied automatically if you’re eligible.

Are the rules the same across the whole UK?

No. England, Scotland, Wales and Northern Ireland each run separate schemes with different thresholds and different relief percentages — see the comparison table above.

{kind=link}