The business rates system changed significantly from 1 April 2026. The 40% Retail, Hospitality and Leisure relief ended. A full revaluation took effect. Five new multipliers replaced the old two-tier system. If your bill looks different this year, there is a reason — and there may be relief you can still claim. This guide covers every active scheme, who qualifies, what is automatic, and what requires an application.

Important: All changes covered here apply to England only. Scotland and Wales operate separate business rates systems with different relief arrangements.

What Changed on 1 April 2026

The 2026 Business Rates Revaluation

The Valuation Office Agency (VOA) updated all rateable values on 1 April 2026. New values are based on rental market data from 1 April 2024 — not the pandemic-era figures used in 2023. Rents in retail and hospitality recovered strongly after 2021. Many properties have seen their rateable values rise as a result.

Your rateable value is not your rent. It is the VOA’s estimate of what your property could have fetched on the open rental market on the valuation date. The revaluation happens every three years. The next one is due in 2029.

Why the 40% RHL Relief Ended

The Retail, Hospitality and Leisure relief scheme ran for years as a temporary measure. In 2025/26 it gave eligible businesses 40% off their bill, capped at £110,000 per business. That scheme ended on 31 March 2026. The government announced at Autumn Budget 2024 that permanent lower multipliers would replace it from 2026. So the relief has not disappeared — it has been baked into the system instead.

The Five New Business Rates Multipliers for 2026/27

From 1 April 2026, five multipliers apply in England. The one used for your property depends on its rateable value and whether it qualifies as a Retail, Hospitality and Leisure (RHL) premises.

| Property Type | Rateable Value | Multiplier |

|---|---|---|

| Small business RHL | Under £51,000 | 38.2p |

| Standard RHL | £51,001–£499,999 | 43.0p |

| Small business (non-RHL) | Under £51,000 | 49.9p |

| Standard (non-RHL) | £51,001–£499,999 | 54.7p |

| Higher (all property types) | £500,000 and above | 50.8p |

Your rates bill is calculated as: rateable value × multiplier. A café with a rateable value of £40,000 using the small business RHL multiplier pays £15,280 before any additional relief. At the old standard non-RHL rate, the same property would have paid considerably more. The new RHL multipliers represent a permanent cut — not a time-limited discount.

Who Pays the 1p Supplement?

A 1p supplement is added to multipliers for ratepayers who do not receive Transitional Relief or Supporting Small Business Relief in 2026/27. It applies for this one year only, and it part-funds the Transitional Relief scheme. If you qualify for SSBR or Transitional Relief, you do not pay it.

Small Business Rate Relief in 2026

The core thresholds for Small Business Rate Relief (SBRR) remain the same. Properties with a rateable value below £12,000 receive 100% relief — nothing to pay. Between £12,001 and £14,999, relief tapers down at 1% for every £30 of rateable value. Properties with a rateable value between £15,000 and £51,000 do not receive a percentage discount but pay on the lower small business multiplier rather than the standard rate.

Understanding sole trader tax obligations alongside business rates is useful here — both affect your overall cost base, and managing one well creates headroom for the other.

The New 3-Year Rule for Second Properties

Previously, if you took on a second property, you lost SBRR on your first property after just one year. From 1 April 2026, that changes. You can now keep SBRR on your original property for three years after acquiring a second. This matters for expanding businesses — you will not lose relief the moment you sign a second lease.

What Replaces RHL Relief — The New RHL Multipliers

The 40% discount is gone. In its place are two permanently lower multipliers for qualifying RHL properties. The government estimates this affects over 750,000 RHL properties and is worth nearly £1 billion per year in ongoing tax relief.

38.2p vs 43.0p — Which Applies to You?

The small business RHL multiplier of 38.2p applies if your property’s rateable value is under £51,000. The standard RHL multiplier of 43.0p applies for properties valued between £51,001 and £499,999. Both are 5 pence below their non-RHL equivalents. The shift to permanent multipliers gives businesses certainty going forward — no more annual budget-by-budget decisions about whether relief would be extended.

Which Businesses Qualify?

Your property must be occupied and wholly or mainly used for qualifying retail, hospitality or leisure purposes. The test is on use, not the VOA description on your valuation list.

Qualifying uses include:

- Shops, market stalls, and post offices

- Restaurants, cafés, pubs, bars, and takeaways

- Hotels, guesthouses, boarding houses, and holiday lets

- Gyms, spas, sports venues, and leisure centres

- Cinemas, theatres, live music venues, museums, and exhibition halls

Excluded uses include nightclubs used primarily for drinking without live entertainment, storage-only premises, and offices. If you are unsure whether your property qualifies, contact your local billing authority.

Supporting Small Business Relief 2026 (SSBR)

The 2026 Supporting Small Business Relief scheme is entirely separate from the 2023 scheme. It targets businesses hit hardest by the revaluation — those whose bills rose sharply because they lost existing reliefs.

Who Qualifies?

You qualify for 2026 SSBR if your rates bill increased following the April 2026 revaluation and you have lost some or all of:

- Small Business Rate Relief

- Rural Rate Relief

- The 40% Retail, Hospitality and Leisure relief

- 2023 Supporting Small Business relief

The £800 Annual Cap

If eligible, your bill will not go up by more than £800 in 2026/27 — or the relevant Transitional Relief percentage cap, whichever is greater. This compares your new bill against what you paid in 2025/26. Sudden bill spikes create serious cash flow pressure for small businesses. The cap is there to prevent exactly that.

Automatic — No Application Needed

SSBR is applied automatically by your local council. You do not need to apply. Check your revised bill to confirm the relief is showing. If you believe you qualify and it has not been applied, contact your billing authority in writing. Relief is recalculated if circumstances change — such as vacating the property or a change in rateable value.

Transitional Relief Scheme 2026

Transitional Relief limits how much your bill can rise in percentage terms following the revaluation. The government redesigned the scheme for 2026, with total support worth £3.2 billion.

Bill Increase Caps by Property Size

The upwards caps for 2026/27 are:

| Property Size | Rateable Value | 2026/27 Cap | 2027/28 Cap | 2028/29 Cap |

|---|---|---|---|---|

| Small | Up to £20,000 (£28,000 in London) | 5% | 10% + inflation | 25% + inflation |

| Medium | £20,001–£100,000 | 15% | 25% + inflation | 40% + inflation |

| Large | Over £100,000 | 30% | 25% + inflation | 25% + inflation |

There are no downward caps. If your rateable value fell at the 2026 revaluation, you get the full benefit immediately from 1 April 2026.

15% Relief for Pubs and Live Music Venues

On 27 January 2026, the government announced a separate additional relief for pubs and live music venues. Eligible businesses receive a further 15% reduction on top of any other relief they already get. This applies to occupied public houses and live music venues that are openly accessible to the general public. Bills for qualifying venues are also frozen in real terms for a further two years. The scheme runs through 2026/27. It is automatic — no application is needed.

Other Relief Schemes Still Available

Several existing schemes continue in 2026:

Charitable Rate Relief — Registered charities get 80% mandatory relief. Local councils can top this up to 100%.

Rural Rate Relief — Sole general stores, post offices, pubs, and petrol stations in rural settlements with a population under 3,000 can receive up to 100% relief.

Empty Property Relief — No rates for the first 3 months a property is empty (6 months for industrial properties). Full rates apply after that.

Improvement Relief — Businesses that make qualifying improvements receive 12 months of protection from bill increases resulting from those improvements.

Heat Networks Relief — Properties used as heat network stations receive 100% mandatory relief.

EV Charging Point Relief — New from 2026. Properties that install eligible electric vehicle charging points receive 100% relief for 10 years. This is one of the most underreported reliefs currently available. If your business premises have installed or plan to install EV charge points, contact your council.

Hardship Relief — Discretionary. Your local authority can grant this if severe financial difficulty can be demonstrated. Not guaranteed — apply directly to your council.

Staying on top of allowable business expenses matters here. Business rates count as a deductible expense against profit, which partially offsets the cost through your tax bill.

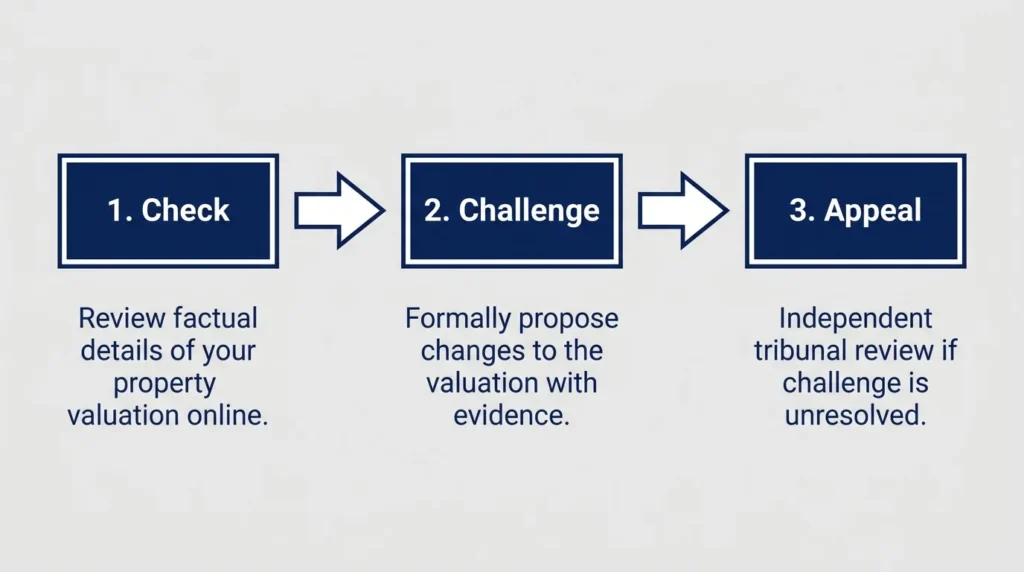

How to Check and Challenge Your Rateable Value

Your rateable value is set by the VOA. Use the “Find a business rates valuation” tool on GOV.UK to view your 2026 figure. If you think it is too high, the process is:

- Check — Submit a formal Check case to the VOA. This is an information-sharing step required before proceeding.

- Challenge — If the Check does not resolve it, submit a formal Challenge with supporting evidence.

- Appeal — If the Challenge is rejected, appeal to the independent Valuation Tribunal.

Important deadline: The window to challenge 2023 assessments closed on 31 March 2026. For the 2026 list, you can start a Check now. Acting early matters — getting your rateable value corrected reduces your bill permanently, not just for one year.

How to Apply — Quick Reference

| Relief Scheme | Application Required? |

|---|---|

| Small Business Rate Relief | Yes — contact your local council |

| RHL Multipliers | No — applied automatically to eligible properties |

| Supporting Small Business Relief 2026 | No — automatic |

| Transitional Relief | No — automatic |

| Pubs and Live Music Venue Relief | No — automatic |

| Charitable Rate Relief | Yes — contact your local council |

| Rural Rate Relief | Yes — contact your local council |

| Improvement Relief | Yes — contact your local council |

| EV Charging Point Relief | Yes — contact your local council |

| Hardship Relief | Yes — discretionary, apply to your council |

Key Dates at a Glance

| Date | What Happened or Happens |

|---|---|

| 1 April 2024 | Valuation date for the 2026 revaluation |

| 31 March 2026 | 40% RHL relief ended; 2023 SSBR ended; deadline to challenge 2023 assessments |

| 1 April 2026 | New multipliers, 2026 revaluation, SSBR 2026, and Transitional Relief all took effect |

| 27 January 2026 | Government announced 15% pub and live music venue relief |

| 2026/27 only | 1p supplement applies for non-relief ratepayers |

| 1 April 2029 | Next scheduled business rates revaluation |

What to Do If Your Bill Looks Wrong

Check it line by line. Confirm which multiplier was applied. Look for SSBR and Transitional Relief entries. If a relief is missing that you believe you qualify for, contact your billing authority in writing. Errors are not uncommon during major revaluations — councils are processing large volumes of bills and reliefs at the same time.

If your rateable value looks too high, start a VOA Check case as soon as possible. A corrected valuation has a permanent effect on your bill, not just a one-year fix.

Understanding your broader tax planning options for small businesses is also worth doing this year. Business rates interact with corporation tax, income tax, and VAT in ways that can affect your overall tax position.

Conclusion

Business rates in 2026 are more complex than in any recent year. The revaluation, the end of 40% RHL relief, five new multipliers, and a bundle of transitional schemes all landed at the same time. Most reliefs are applied automatically — but check your bill to make sure they have been. The new permanent RHL multipliers are a genuine long-term saving for retail, hospitality and leisure businesses. For those losing SBRR or RHL relief, SSBR and Transitional Relief are designed to cushion the impact through 2029. If your rateable value is wrong, challenge it. And if you are in any doubt about eligibility, contact your local council directly — they are responsible for administering every scheme covered here.

{kind=link}