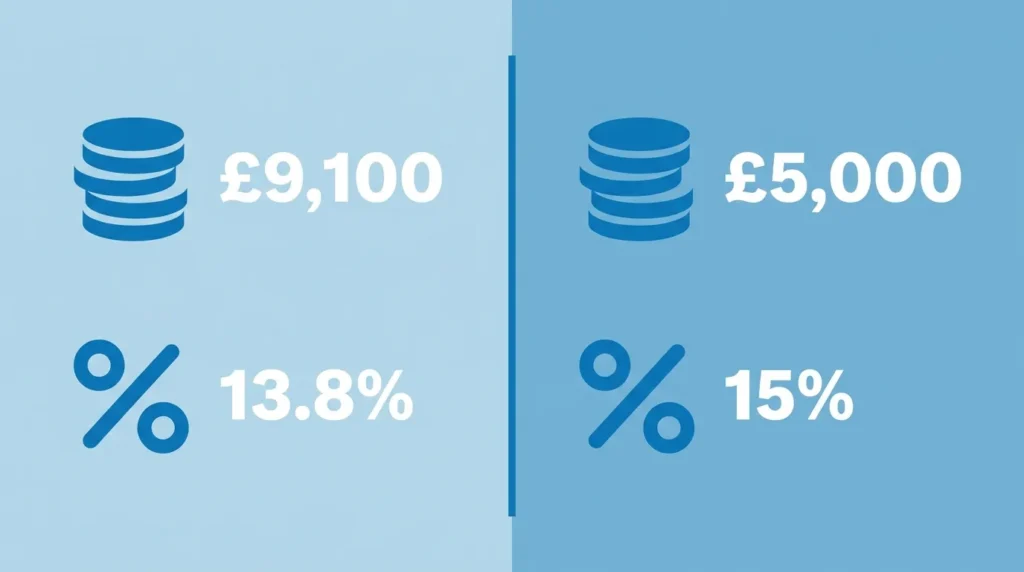

The employer National Insurance rate for 2025/26 is 15%. That is up from 13.8% — a rise that took effect on 6 April 2025, following the Autumn Budget 2024.

At the same time, the secondary threshold dropped from £9,100 to £5,000 a year. That is the point at which employer contributions start. A higher rate kicking in on a lower threshold means most UK employers are paying substantially more per employee this tax year.

On an employee earning the UK average salary of £37,000, the combined impact adds roughly £950 to the employer NI bill compared to 2024/25. Across a team of ten, that is close to £10,000 in additional annual cost.

This guide covers the exact rates, how to calculate what you owe, which employees attract reduced or zero rates, and the most effective steps to bring the bill down legally.

What Is the Employer NI Rate for 2025/26?

The standard employer National Insurance rate for 2025/26 is 15%.

This applies to secondary Class 1 National Insurance contributions — the amount employers pay on top of wages. It does not appear on the employee’s payslip. It is a direct cost to the business.

The rate rose from 13.8% on 6 April 2025. HMRC has confirmed the 15% rate continues into 2026/27. This was described as a structural change, not a temporary measure. Employers should plan their payroll budgets around this figure long term.

| 2024/25 | 2025/26 | |

|---|---|---|

| Standard employer NI rate | 13.8% | 15% |

| Secondary threshold (annual) | £9,100 | £5,000 |

| Secondary threshold (monthly) | £758 | £417 |

| Secondary threshold (weekly) | £175 | £96 |

| Employment Allowance | £5,000 | £10,500 |

The Secondary Threshold: What Changed and Why It Matters

Before any employer NICs apply, earnings must exceed the secondary threshold.

From April 2025, that figure is £5,000 a year — down from £9,100. That is a 45% reduction. In monthly payroll terms, contributions now start on earnings above £417, not £758. Part-time and lower-paid staff who previously cost nothing in employer NI may now fall inside the bracket.

The lower threshold compounds the rate increase. Even if the rate had stayed the same, the drop from £9,100 to £5,000 alone would have raised employer costs. Combined, the two changes hit payroll budgets from both sides.

An employee on £25,000 in 2024/25 generated an employer NI bill of £2,194. The same salary in 2025/26 costs £3,000 in employer NI — an additional £806 per year. That figure scales with headcount.

Understanding this impact is essential for managing cash flow in your small business, especially if you have multiple employees on modest salaries.

How to Calculate Employer National Insurance

The calculation is straightforward. Subtract the secondary threshold from the employee’s annual gross earnings, then multiply by 15%.

Step-by-step:

- Take the employee’s annual gross salary — e.g. £30,000

- Subtract the secondary threshold: £30,000 − £5,000 = £25,000

- Multiply by 15%: £25,000 × 0.15 = £3,750

That is your annual employer NI cost for that employee before any allowances.

Worked Example 1 — Employee earning £25,000:

- £25,000 − £5,000 = £20,000

- £20,000 × 15% = £3,000

- In 2024/25, the same salary cost £2,194 in employer NI

- Year-on-year increase: £806

Worked Example 2 — Employee on UK average salary of £37,000:

- £37,000 − £5,000 = £32,000

- £32,000 × 15% = £4,800

- In 2024/25, the same salary cost approximately £3,850 in employer NI

- Year-on-year increase: £950

Payroll software handles these calculations per pay period — weekly or monthly — automatically. One exception is directors. HMRC calculates director NI on an annual earnings period rather than per payrun, which affects when contributions fall due within the year.

Employment Allowance 2025/26: Up to £10,500 Off Your Bill

The Employment Allowance for 2025/26 is £10,500. That is more than double the £5,000 limit that applied in 2024/25.

The allowance is a credit applied against your employer Class 1 NI bill. It is claimed through payroll software and reduces your payments to HMRC each month until the full £10,500 is used up or the tax year ends. You do not receive it as a cash payment.

Example: Monthly employer NI bill of £1,100. The Employment Allowance covers that amount for the first nine months. From month ten, normal payments resume.

The £100,000 eligibility cap — which previously prevented larger businesses from claiming — has been removed from 2025/26. That means businesses that could not access the allowance before may now qualify.

Who can claim:

- Most UK employers with a PAYE scheme and at least one eligible employee

- Businesses of all sizes (the previous £100k cap no longer applies)

Who cannot claim:

- Limited companies where a director is the only employee

- Employers of domestic staff (nanny, cleaner, gardener) unless the worker is a certified care or support worker

- Certain public bodies and charities in specific structures

Unused allowance at the end of the tax year does not carry over. If you have not claimed yet, do so now — it applies retrospectively to 6 April and reduces payments going forward.

For many small employers with NI bills under £10,500, the allowance eliminates the liability entirely. This is one of the most impactful reliefs available.

Zero-Rate and Reduced Employer NI: Full Exemptions by Category

Not every employee triggers the standard 15% rate. HMRC operates a system of NI category letters, and getting them right can save thousands each year.

NI Category Letter Reference — 2025/26

| Employee type | Category | Employer rate | 0% threshold |

|---|---|---|---|

| Standard employee | A | 15% above £5,000/yr | — |

| Employee under 21 | M | 0% up to UST | £50,270/year |

| Apprentice under 25 | H | 0% up to AUST | £50,270/year |

| Armed forces veteran (first 12 months) | V | 0% up to VUST | £50,270/year |

| Freeport employee | F / I / S / L | 0% up to FUST | £25,000/year |

| Investment Zone employee | N | 0% up to IZUST | £25,000/year |

Employees under 21 (Category M): You pay 0% employer NI on their earnings up to the Upper Secondary Threshold (UST) of £50,270. Above that, the standard 15% applies. The relief ends on the employee’s 21st birthday — your payroll software should flag this automatically.

Apprentices under 25 (Category H): Same threshold — 0% on earnings up to £50,270. An apprentice earning £25,000 costs nothing in employer NI. If you have not considered using the UK small business apprenticeship scheme, the NI saving alone makes it worth reviewing.

Armed forces veterans (Category V): Zero employer NI during the veteran’s first 12 months of civilian employment, up to £50,270. You must verify the individual qualifies before applying this category. Evidence of qualifying service is your responsibility to hold.

Freeport and Investment Zones (Categories F, I, N, S, L): Businesses in designated Freeport or Investment Zone tax sites pay 0% employer NI on eligible staff earnings up to £25,000. The relief applies for up to 36 months per employee, but the worker must spend at least 60% of their time working within the designated site. Check HMRC’s official Freeport list to confirm your location qualifies.

Category letters must be correctly assigned in your payroll system. Miscategorisation either triggers underpayment (HMRC penalties and interest) or overpayment (money left on the table).

Class 1A and Class 1B: NI on Benefits in Kind

Employer NICs are not limited to wages.

Class 1A NI applies to taxable benefits in kind you provide to employees. Company cars, private medical insurance, gym memberships, and similar perks all attract Class 1A NI at 15% for 2025/26. It is calculated on the total taxable value of benefits reported on P11D forms. Payment deadline: 19 July by cheque, 22 July by BACS.

Class 1B NI applies when you have a PAYE Settlement Agreement (PSA) with HMRC. A PSA lets you pay the tax and NI on minor or irregular benefits — staff gifts, team events — on behalf of employees, so they do not have to. The 2025/26 rate is also 15%, applied to the grossed-up value of those benefits.

Neither class appears in payroll software automatically. Both need to be calculated separately and paid to HMRC on their own deadlines.

How to Reduce Your Employer NI Bill

There are four effective and HMRC-compliant routes to lower what you pay.

1. Salary sacrifice schemes

When an employee gives up part of their gross salary in return for a non-cash benefit — pension contribution, cycle-to-work scheme, or ultra-low emission vehicle lease — the sacrificed portion is removed from their gross pay. You do not pay employer NI on it.

At 15%, every £1,000 sacrificed saves £150 in employer NI. A company with 20 employees each sacrificing £3,000 per year into a pension scheme saves £9,000 annually in employer NI alone. Many employers pass part of that saving back to the employee as an enhanced pension contribution — a genuine win on both sides.

2. Hire under-21s and apprentices

Zero employer NI up to £50,270 makes younger workers significantly cheaper to employ. An apprentice earning £28,000 generates no employer NI at all. Add the Employment Allowance on top, and the effective NI cost of a growing team can be minimal. Factor this into your next hire.

3. Review director salary structure

Directors of limited companies often draw a salary at or just below the primary threshold of £12,570, with the rest taken as dividends. Dividends are not subject to employer NI. This strategy reduces the NI liability substantially. If you are weighing up your business structure, the sole trader vs limited company comparison explains how this plays out in practice. One important note: sole directors with no other employees cannot claim the Employment Allowance.

4. Check Freeport and Investment Zone eligibility

If your business operates — or could base staff — within a designated Freeport or Investment Zone, the 0% threshold of £25,000 dramatically cuts your NI per qualifying employee. The 36-month cap means this is a medium-term planning opportunity, not just a year-by-year benefit.

Beyond payroll, there are further options worth exploring across your wider cost base — the guide to reducing costs in your UK small business covers both payroll and operational savings strategies.

Payroll Compliance Checklist for 2025/26

Run through these before the next payroll cycle:

- Payroll software rates updated — confirm it is using 15% and £5,000 secondary threshold, not the old figures

- NI category letters checked — especially employees under 21 (M), apprentices under 25 (H), veterans (V), and Freeport workers (F/I/S/L)

- Employment Allowance claimed — if not yet claimed, do it now via your payroll software; it applies from 6 April

- Benefits in kind reviewed — estimate Class 1A liability before the 19/22 July deadline

- RTI submissions accurate — Real Time Information errors trigger HMRC queries; verify each payrun before submitting

- Director NI basis confirmed — directors use annual earnings period calculations, not the standard per-period method

Payroll errors also create problems when completing year-end accounts and self-assessment. Getting contributions right from the start avoids corrections later — something worth noting if you are also working through your UK small business tax return.

Frequently Asked Questions

What is the employer NI rate for 2025/26? The standard employer National Insurance rate is 15%. It applies to secondary Class 1 NICs on employee earnings above the secondary threshold of £5,000 per year.

What is the secondary threshold for 2025/26? £5,000 per year — down from £9,100 in 2024/25. In monthly terms that is £417, or £96 per week.

When did the rate increase take effect? 6 April 2025, the start of the 2025/26 tax year. It was announced at the Autumn Budget on 30 October 2024.

Do small businesses have to pay the full 15%? Not necessarily. The Employment Allowance reduces employer Class 1 NI by up to £10,500. Businesses with a total NI bill under that amount may owe nothing after the allowance is applied.

Is the 15% rate permanent? It continues into 2026/27 and beyond. HMRC has not indicated a planned reduction. Treat it as the long-term baseline.

Do I pay employer NI on all employees? No. Employees under 21, apprentices under 25, and qualifying veterans pay 0% employer NI up to £50,270. Freeport and Investment Zone employees have a 0% band up to £25,000.

What happens if I apply the wrong NI category? You either underpay (HMRC can charge penalties and interest on arrears) or overpay (you are entitled to reclaim, but the process takes time). Both outcomes are avoidable with accurate setup.

Summary

The employer National Insurance rate for 2025/26 is 15%, up from 13.8%. The secondary threshold dropped to £5,000 per year. Together, these changes add between £800 and £950 per year to the employer NI cost of an average-wage employee.

The Employment Allowance, doubled to £10,500 with no eligibility cap, offsets a large share of that for most small employers. Category exemptions for under-21s, apprentices, and veterans, combined with salary sacrifice schemes and director salary planning, can reduce the bill further.

The priority actions are: confirm your payroll software has the correct rate and threshold, check every employee’s NI category letter, and claim the Employment Allowance if you have not already.

For broader financial planning alongside these changes, both smart tax planning strategies for UK small businesses and how to budget your small business costs are useful starting points.

: Step-by-Step Guide")

{kind=link}