Making Tax Digital for Income Tax isn’t something coming in the distant future. For sole traders earning over £50,000, the start date is 6 April 2026. That’s now less than a year away.

If you’re self-employed and haven’t looked at this properly yet, now is the right time. The rules change how you report your income to HMRC — not just once a year, but four times. And if you miss deadlines, there are real financial penalties.

Here’s exactly what’s changing, who it affects, and what you need to do about it.

What Is Making Tax Digital for Income Tax?

Making Tax Digital for Income Tax — usually called MTD for IT or MTD ITSA — is HMRC’s programme to move self-employed income reporting away from an annual tax return and onto a system of quarterly digital updates.

It does not change how much tax you pay. It changes how and when you report your income.

Right now, you file a Self Assessment return once a year by 31 January. Under MTD, you’ll send HMRC a summary of your income and expenses four times a year, then confirm your final tax position with a year-end declaration.

The Self Assessment tax return is not being abolished. The Final Declaration replaces it in function — but the process becomes digital and more frequent.

Does Making Tax Digital Apply to You?

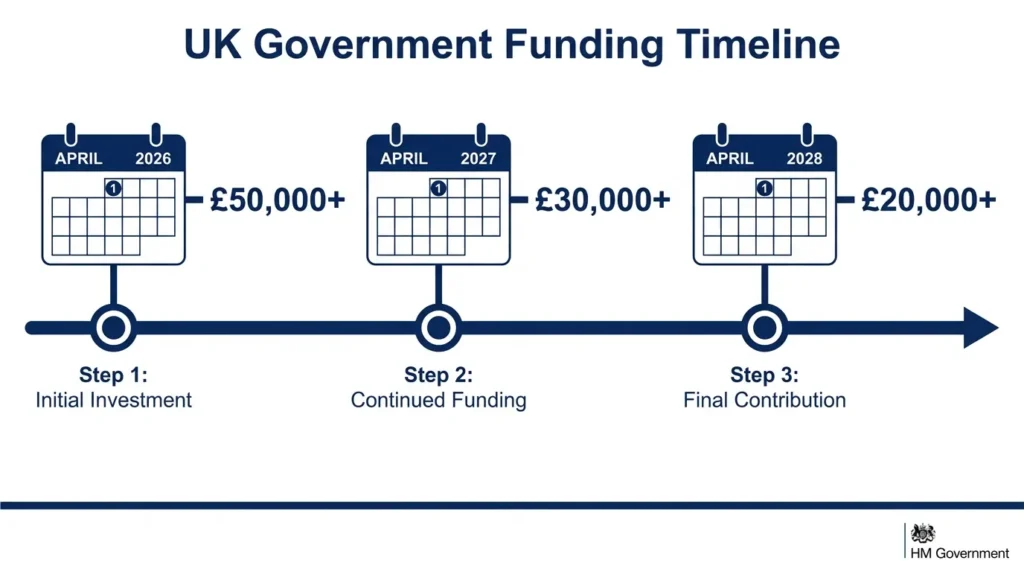

MTD for Income Tax applies to sole traders whose qualifying income exceeds a set threshold. The rollout happens in three phases.

| Start Date | Income Threshold |

|---|---|

| 6 April 2026 | Over £50,000 |

| 6 April 2027 | Over £30,000 |

| 6 April 2028 | Over £20,000 |

Qualifying income is your gross income — before expenses — from self-employment and/or UK property rental. It’s assessed using figures from the tax year two years before your start date. So eligibility for April 2026 is based on your 2024/25 tax year gross income.

What counts as qualifying income?

Qualifying income includes:

- Gross self-employment income (sole trader turnover)

- UK property rental income

It does not include PAYE employment income.

What if you have a job as well as a side business?

This is a very common situation and often misread. If your sole trader income is £15,000 and your PAYE salary is £40,000, your qualifying income for MTD purposes is just £15,000 — well below the current threshold. But if you also earn £8,000 from a rental property, your qualifying income becomes £23,000. Still under £30,000, but you’ll be in scope when the third phase arrives in April 2028.

Employment income doesn’t count. Self-employment and property income do. That distinction matters for anyone earning from multiple sources.

What Changes Under MTD for Sole Traders?

Three things change: how you keep records, how often you report, and what your year-end submission looks like.

1. Digital record-keeping

You must record all business income and expenses using HMRC-recognised software. Paper records and standalone spreadsheets no longer meet the requirement. You can still use spreadsheets, but only if they’re connected to bridging software that submits data to HMRC in the correct digital format.

Every invoice raised, every expense incurred — recorded digitally throughout the year.

2. Quarterly updates

Four times a year, you send HMRC a cumulative summary of your income and expenses. These are reporting submissions, not tax payments. No money changes hands when you file them.

The cumulative nature is worth understanding. By the time you submit your Q3 update, it includes all income and expenses from April through January. You’re not re-entering data from scratch each quarter.

Each quarterly period covers:

- Q1: 6 April – 5 July

- Q2: 6 July – 5 October

- Q3: 6 October – 5 January

- Q4: 6 January – 5 April

3. End of Period Statement and Final Declaration

After the tax year ends, you submit an End of Period Statement (EOPS) for each income source. This is a step most guides skip over entirely. The EOPS is where you make final adjustments — claiming allowable reliefs, correcting figures — before closing the year for that income source.

Then comes the Final Declaration, which performs the same function as your current Self Assessment return. This is where you include any additional income (bank interest, dividends, capital gains) and confirm your overall tax position. The Final Declaration deadline is 31 January — same as the current Self Assessment deadline.

Quarterly Update Deadlines — Exact Dates

If you’re in the first cohort starting 6 April 2026, these are your submission deadlines:

| Quarter | Period | Submission Deadline |

|---|---|---|

| Q1 | 6 Apr – 5 Jul 2026 | 7 August 2026 |

| Q2 | 6 Jul – 5 Oct 2026 | 7 November 2026 |

| Q3 | 6 Oct 2026 – 5 Jan 2027 | 7 February 2027 |

| Q4 | 6 Jan – 5 Apr 2027 | 7 May 2027 |

The Final Declaration deadline remains 31 January each year.

Your first real deadline — 7 August 2026 — is the one to anchor everything around.

How to Register for MTD as a Sole Trader

You sign up through your HMRC online account via the Government Gateway. Voluntary sign-up is open now through MTD-compatible software providers.

Steps to follow:

- Check your 2024/25 Self Assessment figures — add your gross self-employment income plus any UK property income

- Choose HMRC-recognised software and get it set up

- Register for MTD for Income Tax through your Government Gateway account or via your software provider’s sign-up flow

- Start recording transactions digitally from 6 April 2026

- Submit your first quarterly update by 7 August 2026

Don’t leave registration until March 2026. Software setup takes time, and transferring existing records always takes longer than expected.

What Software Do You Need?

You need HMRC-recognised software that submits updates directly via HMRC’s API. There are three categories to consider.

Full accounting software handles everything — invoicing, expense logging, VAT (if applicable), and quarterly MTD submissions. QuickBooks, Xero, Sage, and FreeAgent all offer sole trader plans. Costs typically run between £15 and £35 per month, with introductory discounts widely available.

Bridging software connects your existing spreadsheets (Excel or Google Sheets) to HMRC’s system. You maintain records the way you always have, and the bridging tool handles the digital submission. This suits sole traders with simple income structures who don’t want to switch platforms.

Free options do exist. HMRC’s approved software list includes a handful of free tools, primarily for sole traders with one income source and straightforward expenses.

Always check HMRC’s official software list on Gov.uk for current options. If your records are currently scattered across emails and a spreadsheet, getting them into a single digital system now is the most useful thing you can do before April 2026. A good starting point is reviewing free file management and sharing tools for UK small businesses to understand what’s available before committing to paid accounting software.

MTD Penalties for Sole Traders

HMRC uses a points-based penalty system for late quarterly submissions.

Each missed quarterly update earns 1 penalty point. Once you accumulate 4 points, HMRC issues a £200 financial penalty. Points reset after a 24-month period of full compliance — but only once all outstanding submissions are filed.

Late or inaccurate Final Declarations fall under HMRC’s existing tax penalty regime, which operates separately and can be significantly more costly depending on the nature of the error.

First-year grace period: HMRC has indicated it will not charge penalty points for late quarterly updates during the first 12 months for the April 2026 cohort. This is an administrative concession — it is not written into legislation and could be withdrawn. Treat it as goodwill breathing room, not a reason to delay your compliance setup.

Who Is Exempt from Making Tax Digital?

HMRC has confirmed exemptions for the following groups:

- Digitally excluded individuals — those with no reliable internet access or a disability that prevents digital filing

- Those with no National Insurance number

- Trustees and personal representatives (executors) managing estates

- Non-UK residents with no UK property income

- Those whose income comes entirely from sources not covered by MTD (investments only, for example)

If you believe you qualify for an exemption, apply through your Government Gateway account directly to HMRC. Approval is not automatic.

Making Tax Digital sits within a broader wave of regulatory change affecting UK sole traders and small businesses. The Workers’ Rights Bill changes that came into force in 2026 are another example of how the compliance landscape is shifting — understanding which obligations apply to you now is far less stressful than scrambling to catch up.

Common Questions About MTD for Sole Traders

Does MTD change how much tax I owe? No. MTD changes the frequency and format of reporting, not the calculation of your tax liability. Your bill is still worked out the same way — the Final Declaration is simply where you confirm it.

Can I still use spreadsheets? Yes, but not on their own. Spreadsheets must be connected to HMRC-recognised bridging software that handles the digital submission. Keeping records in Excel and emailing a copy to HMRC won’t meet the requirement.

What if my income fluctuates below the threshold year to year? If your qualifying income drops below the relevant threshold after you’ve enrolled, you can apply to HMRC to exit MTD. Eligibility is reassessed each tax year. Voluntary enrolment also remains open if you want to get ahead of your mandated start date.

What’s the difference between a quarterly update and a tax payment? Quarterly updates are information-only submissions. No money changes hands. Your actual tax bill is calculated through the Final Declaration, with payment due 31 January.

What is the End of Period Statement and is it separate from the Final Declaration? Yes — the EOPS is a distinct step between quarterly updates and the Final Declaration. Most accounting software handles it within the same workflow, but it is a separate submission for each income source. Missing it would be a compliance error, and it’s a step many MTD guides fail to mention.

How to Prepare for MTD: 5-Step Checklist

Getting ahead of this now removes significant pressure when April 2026 arrives.

- Check your qualifying income. Pull up your 2024/25 Self Assessment return. Add your gross self-employment turnover and any UK property income. If the total exceeds £50,000, you’re in the first cohort.

- Choose your software. Review the HMRC-approved software list on Gov.uk. Match the tool to your income complexity — full accounting software for mixed or growing income, bridging software if your structure is simple and you’re comfortable with spreadsheets.

- Migrate your records digitally. Don’t wait until April 2026. Start now. Get income and expenses logged in your chosen system so the quarterly habit is in place before the obligation begins.

- Register with HMRC. Sign up for MTD for Income Tax through your Government Gateway account at least 6–8 weeks before your start date to allow for any account issues.

- Set deadline reminders. Your first submission is due 7 August 2026. Block all four quarterly deadlines and 31 January in your calendar today.

Building consistent admin habits before MTD goes live makes compliance feel routine rather than reactive. If you want to tighten up how your business operates more broadly, this guide to building a free workflow for your UK small business covers practical systems that work well alongside an MTD setup.

Summary

Making Tax Digital for Income Tax affects sole traders from 6 April 2026 if your gross income from self-employment or property exceeds £50,000. The threshold drops to £30,000 in April 2027 and £20,000 in April 2028 — meaning most sole traders will be in scope within two years.

The core change is four quarterly digital submissions per year, plus an End of Period Statement and a Final Declaration. Tax owed doesn’t change. The reporting process does.

The first quarterly deadline is 7 August 2026. The most useful thing you can do right now is check your qualifying income, choose your software, and start recording transactions digitally. The sole traders who sort this out before April will have nothing to worry about when the deadlines arrive.

: HMRC Steps, NI Rates & Deadlines")

{kind=link}