Choosing your business structure in the UK is not a one-time decision you make when you start. It changes what you pay in tax, how much National Insurance you owe, what admin lands on your plate every year, and what happens if things go wrong.

For 2026/27, three things have shifted the calculation. Class 2 National Insurance is now fully abolished as a mandatory charge. Making Tax Digital for Income Tax has started rolling out for sole traders earning above £50,000. And Corporation Tax remains at 19% for profits below £50,000 — still lower than the basic Income Tax rate plus Class 4 NI that sole traders pay on the same profit. If you are starting your first business in the UK or wondering whether it is time to incorporate, this guide gives you the numbers to decide.

The Core Difference

Sole trader: you are the business

As a sole trader, you and your business are legally the same. Every penny of profit belongs to you — and every debt belongs to you too. You report your income and expenses through Self Assessment each year and pay Income Tax and National Insurance on whatever is left after allowable expenses. There is no company. There is no separate legal entity. It is just you.

Registration is straightforward. You notify HMRC that you are self-employed, set up a Self Assessment account, and keep records of your income and expenses. The process takes around 20 minutes online. Registering your business in the UK as a sole trader costs nothing.

Limited company: a separate legal entity

A limited company is distinct from you as an individual. It is registered with Companies House, has its own legal identity, pays Corporation Tax on its profits, and files its own accounts each year. You can be the sole director and only shareholder. The company owns its assets and owes its debts — not you personally.

To understand everything this structure involves, the full breakdown of what a limited company is in the UK covers the legal and administrative picture in detail. What matters here is how the two structures compare on tax and National Insurance — and at what profit level one starts to beat the other.

National Insurance for Self-Employed UK 2026/27

This is the part most people get wrong. National Insurance for self-employed individuals works very differently from PAYE employment — and 2026/27 brings a cleaner picture than previous years.

Class 2: what happened and what you now pay

Mandatory Class 2 NI was abolished from April 2024 under the National Insurance Contributions (Reduction in Rates) Act 2023. Before that, self-employed people paid a flat weekly charge of around £3.45–£3.50. That obligation is gone.

For 2026/27, the position is:

- Profits above £7,105 (Small Profits Threshold): Class 2 credits are awarded automatically. No payment required. Your State Pension record is protected.

- Profits below £7,105: You receive no automatic credit. You can make voluntary Class 2 contributions of £3.65 per week (£189.80 for the full year) to keep your State Pension record intact.

That voluntary £3.65/week matters. The alternative is paying Class 3 voluntary contributions later, which cost £18.40 per week in 2026/27 — nearly five times more. If your profits are low, it is almost always worth paying the voluntary amount now.

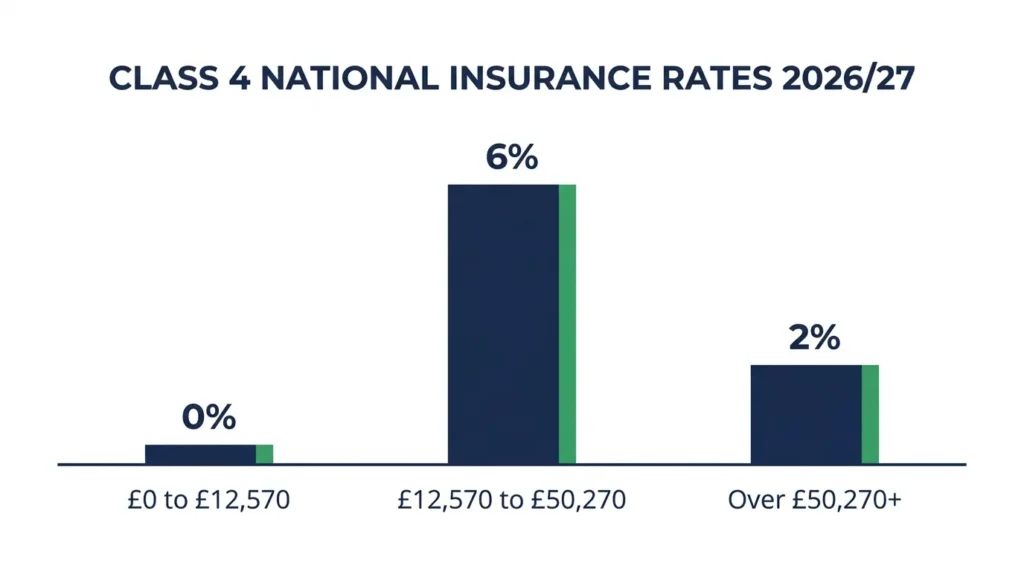

Class 4 rates, thresholds, and what they cost you

Class 4 is the main NI charge for sole traders. It is calculated on your profits and collected through your Self Assessment return — not paid separately throughout the year.

| Profit Band | Class 4 Rate 2026/27 |

|---|---|

| Up to £12,570 | 0% |

| £12,570 – £50,270 | 6% |

| Above £50,270 | 2% |

Example: On £40,000 profit, you pay Class 4 NI on £27,430 (£40,000 minus £12,570). At 6%, that is £1,645.80 in Class 4 NI for the year.

Class 4 does not build State Pension entitlement. Only Class 2 credits (automatic or voluntary) do that.

What limited company directors pay in NI

This is where the structures diverge sharply — and where the tax saving comes from.

As a limited company director drawing a salary of £12,570 (the standard tax-efficient approach for 2026/27), you pay:

- Employee NI (Class 1): £0 — because the salary sits exactly at the Primary Threshold

- Employer NI (Class 1): Around £478 on the salary (15% on amounts above £5,000) — but note: the Employment Allowance of £10,500, which reduces employer NI for eligible businesses, is not available to sole director companies with no other employees. This is a planning factor most guides miss.

The rest of your income comes as dividends. Dividends are not subject to National Insurance at all. On £12,570 salary plus dividends, a limited company director paying themselves £50,000 total would pay significantly less NI than a sole trader with the same profit. That gap is one of the main drivers of the incorporation decision.

Tax Comparison at Three Real Profit Levels

These figures use 2026/27 rates. They assume full personal allowance (£12,570), basic and higher rate Income Tax, Class 4 NI for the sole trader, and an optimal salary-plus-dividends strategy for the limited company director. England/Wales tax rates apply. No VAT registration assumed.

£30,000 profit

Sole trader: Income Tax at 20% on profits above £12,570 = £2,886. Class 4 NI at 6% on £17,430 = £1,045.80. Total tax and NI: approximately £3,931.

Limited company: Corporation Tax at 19% on £30,000 = £5,700. But the director draws £12,570 salary (no Income Tax or NI at this level) and takes the remainder as dividends after CT. After the £500 dividend allowance, dividend tax at 8.75% applies. Total tax burden: approximately £4,100–£4,400 depending on exact extraction, plus £500–£800/year in additional accountancy costs.

Verdict at £30k: Sole trader wins. The extra accountancy cost of a limited company is not recovered through tax savings at this profit level.

£50,000 profit

Sole trader: Income Tax 20% on £12,570–£37,700 = £5,026, then 40% on £37,701–£50,000 = £4,920. Class 4 NI: 6% on £37,700 = £2,262, plus 2% on £12,300 = £246. Total: approximately £12,454.

Limited company: Corporation Tax at 19% = £9,500. Salary £12,570 (no tax, minimal NI). Remaining funds distributed as dividends with dividend tax at 8.75% above the £500 allowance. Total tax including CT and personal dividend tax: approximately £12,100–£12,800 — roughly comparable, before accountancy fees of £800–£1,500/year.

Verdict at £50k: Close to break-even. The sole trader can still come out ahead once accountancy costs are factored in. The advantage of incorporating at this level depends heavily on whether you need all the profit personally each year or can leave some in the company.

£80,000 profit

Sole trader: Significant higher-rate tax exposure. Income Tax at 40% on earnings above £50,270. Class 4 NI at 2% above the upper profits limit. Total tax and NI: approximately £26,000–£28,000.

Limited company: Corporation Tax at 19% on profits up to £50,000 (small profits rate), with marginal relief between £50,000 and £250,000. Optimal extraction via salary and dividends keeps more of the profit in the lower 8.75% dividend tax band rather than 40% Income Tax. Tax saving versus sole trader: typically £3,000–£6,000 per year at this profit level, even after accountancy fees.

Verdict at £80k: The limited company wins on tax. The gap widens further as profits increase.

Personal Liability: Why This Matters More Than Tax

Sole traders carry unlimited personal liability. If your business owes money — to a supplier, a client, a lender — and cannot pay, that debt becomes yours. Your personal savings, your car, potentially your home are all exposed.

A limited company separates you from the business legally. The company’s debts belong to the company. As a director, you can lose what you invested in shares, but your personal assets are generally protected — unless you have personally guaranteed loans or HMRC pursues director liability for misconduct.

For anyone working in a sector where disputes, professional negligence claims, or significant contracts are part of daily life, this protection is often worth the extra admin on its own. The decision is not purely about tax. That said, for a freelancer with low overheads and no staff, the liability risk may be modest enough that sole trader status remains the right call. You can explore affordable business insurance in the UK as one way to mitigate this risk as a sole trader.

Admin and Accountancy Costs: The Full Picture

Sole traders file one Self Assessment return per year. That covers Income Tax and Class 4 NI together. Many sole traders do this themselves using HMRC’s online system. An accountant for a straightforward sole trader typically costs £200–£600 per year.

Limited companies carry more filing obligations: annual accounts to Companies House, a Confirmation Statement, a Corporation Tax return, and potentially a Director’s personal Self Assessment return on top. Most limited company directors use an accountant. Costs typically run £800–£1,500 per year for a small single-director company, rising to £2,000+ for more complex arrangements.

That £800–£1,500 annual cost is a real outgoing that has to be covered before the tax saving counts as a saving. At £50,000 profit, a £1,000 accountancy bill narrows the apparent tax advantage significantly. Small business accounting tips for UK owners can help you keep costs down regardless of your structure.

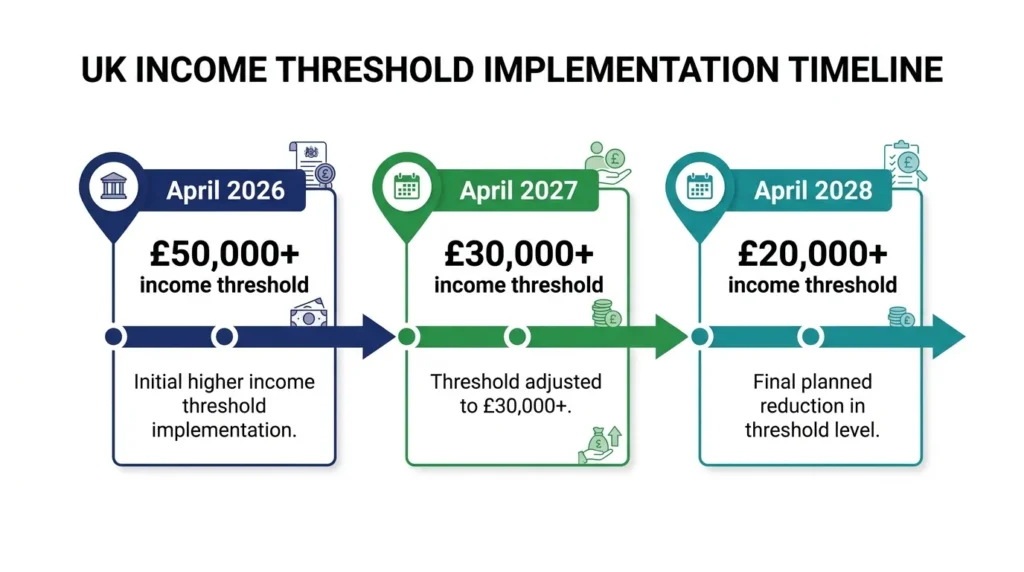

Making Tax Digital from April 2026

Making Tax Digital for Income Tax (MTD) launched on 6 April 2026. It changes the reporting requirements for sole traders — not for limited companies, which already operate under a separate Corporation Tax framework.

Who is affected now:

- Sole traders and landlords with total qualifying gross income above £50,000 must use HMRC-compatible software, keep digital records, and submit quarterly updates. That is four submissions per year, plus a final declaration — five in total.

- From April 2027, the threshold drops to £30,000.

- From April 2028, it extends to £20,000 (announced at Spring Budget 2025).

Qualifying income includes self-employment turnover plus rental income combined. It is based on gross income, not profit. A sole trader with £45,000 in business turnover and £8,000 in rental income has qualifying income of £53,000 and falls inside Phase 1 now.

MTD adds admin work for affected sole traders. You need compatible software — typically £10–£30/month for accounting packages — and must submit quarterly summaries by specific deadlines. The penalty system uses a points-based model: four missed deadlines triggers a £200 fine. Our full guide to Making Tax Digital for Income Tax explains the compliance steps in detail.

Limited companies are not inside MTD for Income Tax. They file Corporation Tax returns separately. This is one reason some sole traders above the £50,000 threshold are accelerating their decision to incorporate — removing themselves from the MTD obligation in the process.

IR35: When the Limited Company Tax Advantage Disappears

IR35 (the off-payroll working rules) applies to contractors who work through a limited company but whose working arrangement resembles employment with one client. HMRC tests whether, if the contract were directly between you and the end client rather than via your company, you would be classed as an employee.

If IR35 applies to your contracts, income from those contracts is taxed as employment income — not via the salary-and-dividends approach that generates the tax saving. The Corporation Tax still applies, but the dividend extraction advantage is eliminated for that income stream.

From April 2021, for contracts with medium and large private-sector clients, the responsibility for determining IR35 status shifted to the client, not the contractor. If your client determines your contract is inside IR35, they apply PAYE to your payments. The limited company wrapper does not protect you.

For contracts genuinely outside IR35 — where you have multiple clients, control over how you work, and the right to substitute — the limited company structure works as intended. But if IR35 risk is high or your entire income comes from one client, the tax advantage of incorporating may be significantly reduced or lost entirely.

When to Switch from Sole Trader to Limited Company

The profit threshold guide:

- Below ~£40,000 profit: Sole trader is usually simpler, cheaper, and roughly tax-equivalent. Extra accountancy cost typically outweighs any tax saving.

- £40,000–£60,000 profit: The break-even zone. The answer depends on how much profit you extract personally each year, your IR35 position, and whether you have a family member who could hold shares in the company (which can shift income into a lower-rate taxpayer’s hands).

- Above ~£60,000 profit: A limited company typically saves £1,500–£6,000+ per year after all costs. The gap grows with profit.

Other factors beyond profit:

Profit level is not the only reason to incorporate. Consider a limited company if:

- Clients require it (some larger businesses and public sector organisations will not contract with sole traders)

- You want to protect personal assets from business risk

- You plan to bring in investors or issue shares

- You want to retain profits in the company for future investment rather than taking everything out each year

The sole trader vs limited company comparison covers this decision in broader detail if you want to map it against your specific situation.

Quick Comparison Table

| Sole Trader | Limited Company | |

|---|---|---|

| Legal status | You and business are one | Separate legal entity |

| Income Tax | 20% / 40% / 45% on profits | Via salary + dividends |

| Corporation Tax | None | 19% (under £50k profit) |

| Class 4 NI | 6% / 2% on profits | Not applicable to dividends |

| Personal liability | Unlimited | Limited to shares |

| Companies House filing | None | Yes – annual accounts + confirmation |

| Self Assessment | Yes | Yes (personal return for director) |

| MTD (from April 2026) | Yes if income >£50k | Not applicable (separate CT framework) |

| Accountancy cost | £200–£600/year | £800–£1,500/year |

| Typical tax advantage | Simpler below £40k | Saves £1,500–£6,000+ above £60k |

Three Questions to Ask Before You Decide

Rather than a generic “consult an accountant” sign-off, here are the three questions that actually determine the right answer:

1. What is your realistic annual profit for the next 12 months — not turnover, profit? Below £40,000, sole trader is likely better. Above £60,000, limited company is worth the admin. In between, the answer is marginal and depends on questions two and three.

2. Do you need every pound of profit personally each year, or can you leave some in the business? A limited company’s tax advantage partly comes from leaving profits inside the company and only drawing what you need. If you must extract everything annually, the Corporation Tax layer reduces the gain.

3. Is your income from one client in a way that could attract IR35 scrutiny? If yes, get a proper IR35 assessment before you incorporate. Incorporating and then being caught inside IR35 gives you extra admin with none of the tax benefit.

If you are earning above £60,000, your income comes from multiple clients, and you do not need every pound personally each year, incorporation is likely the right move. If you are below £40,000 and just starting out, read through your UK small business tax return obligations first — then revisit the decision when your profit grows.

Making the structure decision and getting your Self Assessment tax return right from the start saves money and avoids HMRC penalties. Tax rules change. The rates and thresholds in this guide apply to 2026/27 and reflect current HMRC rules. Always confirm figures with a qualified accountant before making structural changes to your business.

")

{kind=link}