The VAT registration threshold in the UK for 2026 is £90,000. That figure has been frozen since 1 April 2024 and has not changed for 2026/27.

If your taxable turnover crosses £90,000 in any rolling 12-month period, you must register for VAT with HMRC. Miss the deadline and you’ll owe backdated VAT on every sale made since the date you should have registered — whether or not you charged customers for it.

Many businesses miss the deadline not because they don’t know the number, but because they don’t understand how the calculation works or how quickly the clock starts ticking. This guide covers both registration triggers, the rolling 12-month rule, strict HMRC deadlines, penalty rates, and whether voluntary registration makes sense before you hit £90,000.

If you’re still getting to grips with how VAT works in practice for UK small businesses, that’s a useful starting point before reading on.

What Is the UK VAT Registration Threshold in 2026?

The UK VAT registration threshold for 2026/27 is £90,000 in taxable turnover, measured over any rolling 12-month period.

The figure was raised from £85,000 to £90,000 on 1 April 2024. It has not moved since. Some articles published in late 2024 predicted the threshold would fall to £60,000–£70,000 from April 2026. That did not happen. The £90,000 limit remains in place, and no change is currently planned.

“Taxable turnover” means the total value of sales that are not VAT-exempt. It includes:

- Standard-rated sales at 20% — most goods and services

- Reduced-rated sales at 5% — domestic energy, some children’s car seats

- Zero-rated sales at 0% — most food, children’s clothing, books, most exports

Zero-rated sales still count toward the threshold even though you charge 0% VAT on them. That catches a number of businesses — particularly food producers and wholesalers — by surprise.

Exempt sales do not count. Financial services, most insurance, and residential property letting are exempt from VAT, and that income is excluded from your threshold calculation entirely.

The Deregistration Threshold: £88,000

The registration threshold and the deregistration threshold are not the same number. The deregistration threshold for 2026/27 is £88,000.

Once VAT-registered, you can apply to cancel your registration — but only if your taxable turnover has fallen below £88,000 and you expect it to stay there for the next 12 months. You cannot deregister just because your turnover dips below £90,000; it must fall below that lower £88,000 mark.

The £2,000 gap is deliberate. Without it, businesses near the boundary would constantly be jumping in and out of the VAT system every time turnover moved slightly either side of one number.

How the Rolling 12-Month Rule Works

This is where most businesses get caught out.

The threshold is not measured against your accounting year. It’s not your tax year either. HMRC uses a rolling 12-month test, recalculated at the end of every calendar month.

At the end of each month, look back at the previous 12 months. If the total taxable turnover across that window exceeds £90,000, you’ve crossed the threshold — regardless of what your year-end accounts show.

Worked example:

Your turnover from 1 June 2025 to 31 May 2026 totals £93,500. At the end of May 2026, you’ve crossed the threshold. Your April 5 year-end shows £84,000 — that figure is irrelevant. The rolling 12-month total is what HMRC cares about.

Because the window moves forward one month at a time, you could cross the threshold in July, November, or any month of the year. Checking turnover once at your accounting year-end is not enough. Monthly monitoring is the only reliable approach.

Two Triggers That Require Registration

There are two separate legal tests that can make you liable to register for VAT. Both must be monitored.

Trigger 1 — The Backward-Look Test

At the end of any calendar month, if your taxable turnover for the previous 12 months has exceeded £90,000, you must notify HMRC. You have 30 days from the end of that month to do so.

This is the test most people know about.

Trigger 2 — The Forward-Look Test

This one catches people out more often. At any point, if you have reasonable grounds to believe your taxable supplies in the next 30 days alone will exceed £90,000, you must register from the start of that 30-day window.

The trigger is not receipt of payment. It’s the moment you have reasonable grounds to expect it — which could be the day you sign a large contract.

Example: You sign a £110,000 construction contract on 5 June 2026. You have reasonable grounds to believe that contract will push your taxable supplies over £90,000 within the next 30 days. Your obligation to notify HMRC starts on 5 June. You must register by 5 July. Your effective registration date is 5 June.

If you’re in discussions about a large contract that would push you over the threshold in a single month, take VAT advice before you sign. Committing to the contract first and asking questions later can be expensive.

Registration Deadlines and Your Effective Date

Once you cross the threshold via the backward-look test, the timetable is strict.

You must notify HMRC by the end of the 30-day period following the month in which you crossed.

Your effective date of registration — the date you must start charging VAT to customers — is the first day of the second month after you crossed the threshold.

Example:

At the end of August 2026, your rolling 12-month turnover has exceeded £90,000.

- Notify HMRC by: 30 September 2026

- Effective registration date: 1 October 2026

- All taxable sales from 1 October must include VAT

The 30-day notification window is not a grace period. You owe VAT from the effective registration date — not from the date you actually register or receive your VAT number.

Temporary Threshold Breaches — Applying for an Exception

Crossing £90,000 does not always result in mandatory registration. If the breach was temporary — caused by a one-off project, a seasonal spike, or a client paying multiple invoices at once — HMRC allows you to apply for an exception.

To qualify, you must show that your taxable turnover in the 12 months following the breach is expected to fall below the deregistration threshold of £88,000. This requires real evidence: contracts, order books, or revenue forecasts. HMRC may ask to see it.

You still have to notify HMRC of the breach. Submit form VAT1 along with form VAT5EXC to request the exception at the same time. HMRC will either confirm the exception in writing or register you for VAT regardless.

Do not ignore the breach and assume it will sort itself out. If your turnover does stay elevated and HMRC later identifies the missed registration, the exception that would have been available to you is gone — and the penalty clock has been running the whole time.

What Happens If You Register Late?

Late VAT registration carries a real financial cost. HMRC backdates registration to the date you became liable — and you owe VAT on every taxable sale made since then, even if you never charged customers any.

If you invoiced without VAT because you didn’t know you were registered, you absorb that 20% from your own margin. In most cases, going back to former customers to recover it is not realistic.

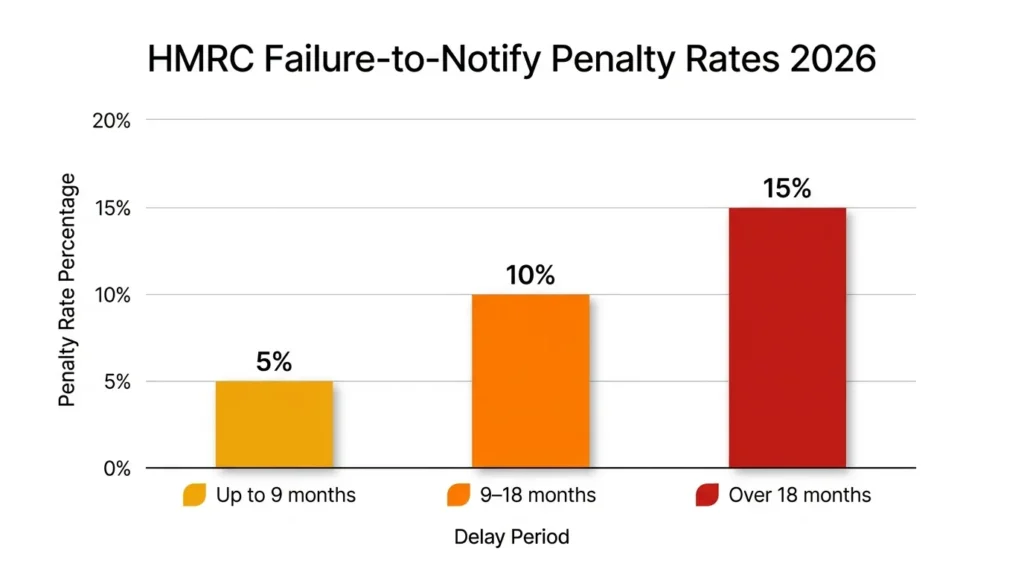

On top of the backdated VAT, HMRC charges a failure-to-notify penalty based on how late the registration is:

| Delay | Penalty Rate |

|---|---|

| Up to 9 months late | 5% of net VAT owed |

| 9 to 18 months late | 10% of net VAT owed |

| More than 18 months late | 15% of net VAT owed |

| Minimum penalty | £50 |

Real-money example: A business that owed £20,000 in backdated VAT and was 14 months late would face a 10% penalty — £2,000 on top of the £20,000 VAT liability. If that same business had ignored the position for over 18 months, the penalty climbs to 15%, or £3,000.

For deliberate non-registration, penalty rates range from 20% to 100% of the VAT owed.

There is one meaningful way to reduce the damage: voluntary disclosure. If you realise you should have registered earlier, contact HMRC before they contact you. An unprompted disclosure consistently attracts lower penalties than one discovered during an HMRC compliance check. The same principle applies across most HMRC obligations — understanding HMRC’s penalty escalation rules for late filings gives useful context for how the system treats voluntary compliance versus non-compliance generally.

Voluntary VAT Registration — Is It Worth It?

You can register for VAT below £90,000. There is no minimum turnover requirement for voluntary registration. For some businesses, registering early is the right commercial decision.

The main benefit is reclaiming input VAT — the 20% you pay on business purchases. Equipment, professional fees, software subscriptions, premises costs: if these carry standard-rate VAT, registration lets you recover that money quarterly. There’s a detailed breakdown of what qualifies in this guide to business expenses you can reclaim from HMRC.

Voluntary registration works well when your customers are predominantly VAT-registered businesses. They can reclaim whatever VAT you add to invoices, so your 20% addition doesn’t increase their real cost. For those clients, your net price hasn’t changed at all.

It rarely makes sense if you sell mainly to consumers or to small businesses that cannot recover VAT. In that case, adding 20% to your prices makes you more expensive, and you may need to absorb the VAT yourself to stay competitive.

One thing to factor in: once you’re registered, VAT must be collected on every eligible sale and paid to HMRC quarterly. There’s a timing gap between invoicing customers and making that quarterly payment, which can create a cash flow squeeze if you haven’t planned for it. Building that into your cash flow management from the start avoids unpleasant surprises.

VAT Rules for Sole Traders and Self-Employed

The VAT registration threshold for sole traders is the same £90,000 limit. There is no separate or lower figure.

A misconception worth addressing: if you run two separate trades as a sole trader — say, a cleaning round and a photography business — HMRC does not give each trade its own £90,000 allowance. You are the taxable entity, not the individual business activities. Both income streams are added together against a single £90,000 total.

Freelancers, consultants, and subcontractors operate under the same rule. The rolling 12-month test applies regardless of how you’re paid — invoiced project fees, day rates, retainers — it all counts.

If you’re at the stage of deciding which business structure is right for you, the VAT position is one factor among several. The tax treatment, liability, and admin requirements differ meaningfully between operating as a sole trader and incorporating as a limited company. This sole trader vs limited company comparison for 2026 lays out the key differences side by side. For those already trading as a sole trader and wanting a full picture of their tax obligations — including Self Assessment, National Insurance, and allowable expenses — the sole trader tax guide covers each area in detail.

How to Register for VAT with HMRC

Registration is completed online through your Government Gateway account. If you don’t have one, you’ll need to set one up first — the same account is used for Self Assessment, PAYE, and most other HMRC interactions.

The registration form is VAT1. You’ll enter your business details, taxable turnover figures, the date you crossed the threshold, and which VAT scheme you want to join.

Processing typically takes 30 working days, though some applications take 6–8 weeks. Your effective registration date is set by when you crossed the threshold — not by when HMRC processes your form. If you start charging VAT before your registration is processed, keep records so you can account for it accurately once your VAT number arrives.

Once registered, you’ll receive a VAT4 certificate confirming your VAT number and effective registration date.

From your very first return, Making Tax Digital for VAT is mandatory. You must keep digital records and submit VAT returns through MTD-compatible software. There is no option to file by post or enter figures manually through a Government Gateway spreadsheet. This is a requirement from day one, not something phased in later. The guide to preparing for Making Tax Digital explains which software is compatible and what digital record-keeping involves.

Frequently Asked Questions

Is the VAT registration threshold going up in 2026? No. The threshold is fixed at £90,000 for 2026/27. It was last changed in April 2024 when it rose from £85,000. No further increase has been confirmed for 2026 or 2027.

Does the rolling 12 months reset at the tax year end? No. It has nothing to do with 5 April. The test is recalculated at the end of every calendar month by looking back 12 months from that point.

What if I crossed £90,000 temporarily due to a one-off contract? You can apply for an exception using forms VAT1 and VAT5EXC, provided you can evidence that turnover will fall below £88,000 in the next 12 months. You still need to notify HMRC of the breach at the same time.

Do non-UK businesses need to register? Yes — and the threshold for them is zero. Non-Established Taxable Persons (NETPs), including overseas businesses storing goods in UK warehouses, must register from their very first UK sale.

How long does VAT registration take? Around 30 working days on average. Some applications take 6–8 weeks. Your effective registration date is not the date your application is approved — it’s the date you became liable, which may be weeks or months earlier.

Can I deregister if my turnover drops? Yes, once your taxable turnover falls below £88,000 and you expect it to remain there. Deregistration is voluntary — there’s no obligation to leave the VAT register the moment you dip below the threshold, but you can apply to HMRC if it makes commercial sense.

Summary

| Registration threshold 2026/27 | £90,000 (rolling 12-month turnover) |

| Deregistration threshold | £88,000 |

| Notification deadline | 30 days from end of month threshold was crossed |

| Effective registration date | First day of the second month after crossing |

| Late penalty — up to 9 months | 5% of net VAT owed |

| Late penalty — 9 to 18 months | 10% of net VAT owed |

| Late penalty — 18+ months | 15% of net VAT owed |

| MTD for VAT | Mandatory from first return |

| Threshold last changed | 1 April 2024 (from £85,000 to £90,000) |

| Non-UK sellers | Zero threshold — register from first sale |

The VAT registration threshold for 2026 is £90,000. The number itself is not the hard part. What trips businesses up is the rolling calculation, the two separate triggers, and the HMRC deadlines that start running the moment you cross the line. Check your rolling 12-month figure at the end of every month. If you’re close to the threshold and a large contract is on the table, take advice before you commit. And if you’ve already crossed without registering, get in touch with HMRC voluntarily — the penalty for a voluntary disclosure is considerably lower than the one waiting at the end of a compliance check.

{kind=link}