In 2025/26, a sole trader with £40,000 profit pays roughly £7,965 in combined income tax and National Insurance. That number surprises people. Most expect it to be lower. This guide shows exactly where it comes from.

Sole trader tax has two main components: income tax on profits above £12,570 and Class 4 National Insurance at 6% on profits between £12,570 and £50,270. Both are reported and paid through Self Assessment, with the main deadline on 31 January each year.

Whether you’re in your first year of trading or you’ve been doing this for a while, getting these numbers right matters. Underpaying leads to unexpected bills. Overpaying is just money left on the table.

What HMRC Actually Taxes

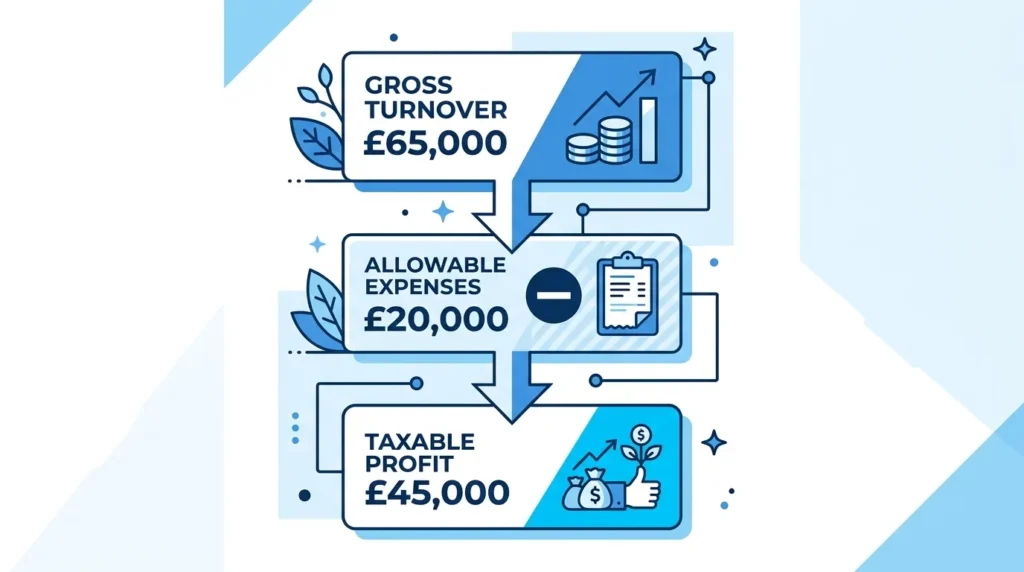

HMRC taxes your taxable profit — not your turnover. This is the single most important distinction in sole trader tax.

A plumber who invoices £65,000 in a year but spends £20,000 on materials, tools, insurance and fuel has a taxable profit of £45,000. Tax starts at £45,000, not £65,000. Every legitimate expense you claim reduces that figure pound for pound.

There’s also a quick win many low-income sole traders overlook: the £1,000 trading allowance. If your gross trading income is £1,000 or less in the tax year, you owe nothing and don’t need to register for Self Assessment. If it’s higher, you can deduct the £1,000 flat allowance instead of actual expenses — but only if your real expenses come to less than £1,000.

If you’ve recently started a business and haven’t registered with HMRC yet, the sole trader registration process in the UK covers every step you need to take, including the 5 October deadline for new traders.

Income Tax Rates and Bands for 2025/26

Once you know your taxable profit, income tax is applied in bands.

The Personal Allowance sits at £12,570. Profit up to that level is tax-free. This threshold has been frozen since 2021 and will remain so until April 2031. That freeze matters because as profits grow over time, more of your income gets pulled into taxable bands — a process HMRC economists call fiscal drag.

| Band | Taxable Profit | Rate |

|---|---|---|

| Personal Allowance | Up to £12,570 | 0% |

| Basic Rate | £12,571 – £50,270 | 20% |

| Higher Rate | £50,271 – £125,140 | 40% |

| Additional Rate | Over £125,140 | 45% |

One figure worth knowing: the Personal Allowance tapers above £100,000. You lose £1 of allowance for every £2 earned above that level. The allowance disappears completely at £125,140. For anyone whose profit is approaching six figures, the effective marginal rate in that range is 60%, not 40%.

Scotland applies different rates. Scottish taxpayers face additional bands at the intermediate and higher levels. The rates in the table above apply to England, Wales and Northern Ireland only.

National Insurance for Sole Traders in 2025/26

National Insurance is the part of the bill most sole traders underestimate. Understanding how self-employed National Insurance contributions work can save you from a significant surprise when your Self Assessment bill arrives.

Two classes apply.

Class 4 NI — The Main Charge

This is where the bulk of your NI bill sits:

- 6% on profits between £12,570 and £50,270

- 2% on profits above £50,270

It’s worth highlighting the rate change here. HMRC reduced Class 4 NI from 9% to 6% in April 2024. If you’re using an old calculator, spreadsheet, or article that predates that cut, your estimate will be too high.

Class 2 NI — What Changed

From April 2024, Class 2 NI no longer requires a cash payment for most sole traders. If your profits exceed the Small Profits Threshold (£6,725 in 2025/26), HMRC treats you as having paid Class 2 automatically. That credit counts toward your State Pension without you paying anything.

If your profits fall below £6,725, you can pay Class 2 voluntarily at £3.45 per week to protect your NI record. For traders above the threshold, Class 2 is no longer an expense.

Real Tax Bills at Three Profit Levels

The figures below assume a UK resident in England with no other income and the standard Personal Allowance. No pension contributions. No additional reliefs.

| Annual Profit | Income Tax | Class 4 NI | Total Bill | Effective Rate |

|---|---|---|---|---|

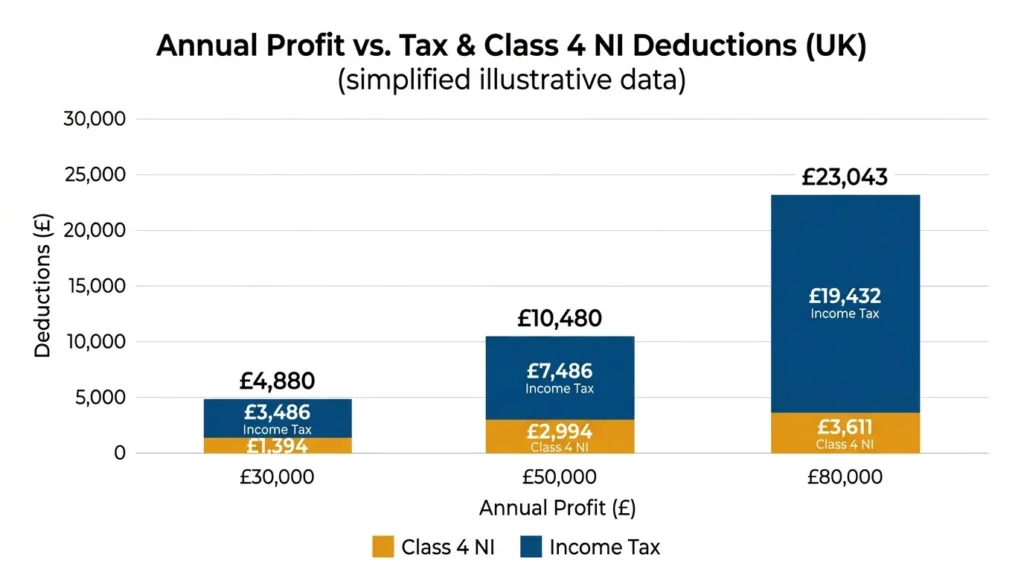

| £30,000 | £3,486 | £1,046 | £4,532 | 15.1% |

| £50,000 | £7,540 | £2,262 | £9,802 | 19.6% |

| £80,000 | £21,432 | £3,134 | £24,566 | 30.7% |

Look at the £50,000 row. Income tax takes £7,540. Class 4 NI adds £2,262. The combined bill is close to £10,000 on a £50,000 profit. A sole trader who hasn’t set money aside through the year faces that in one January payment — plus, potentially, a payment on account on top (more on that below).

The effective rate climbs steeply past the basic rate band. A sole trader earning £80,000 pays over 30p in every £1 to HMRC.

How to Legitimately Reduce Your Bill

The lower your taxable profit, the lower your tax bill. These are the most effective legal ways to reduce it.

Allowable Business Expenses

HMRC permits the deduction of genuine business costs. Common categories include:

- Office costs — stationery, software subscriptions, the business portion of your mobile phone bill

- Travel — business mileage at 45p per mile for the first 10,000 miles, then 25p per mile; train and bus fares for business trips

- Equipment — laptops, tools, cameras, machinery used primarily for business

- Marketing — website hosting, paid advertising, design

- Professional fees — accountancy, legal costs related to the business

- Training — courses that directly relate to your current trade

Mixed-use items — a phone you use for both personal and business, or a vehicle — can only be claimed at the business-use proportion.

Working From Home

If you regularly work from home, HMRC’s flat rate is: £10/month for 25–50 hours, £18/month for 51–100 hours, £26/month for over 100 hours. You can instead calculate the actual business proportion of your bills, but that requires more detailed records.

Pension Contributions

This is the most underused saving for higher-earning sole traders. Contributions to a personal or SIPP pension reduce your taxable profit directly.

If your profit is £53,000 — £2,730 into the higher rate band — a £2,730 pension contribution pulls your taxable income back below £50,270. You save 40% on that slice instead of 20%. On a £3,000 contribution, the combined tax saving and basic rate relief is roughly £1,200. The money sits in your pension, not with HMRC.

Self Assessment Deadlines for 2025/26

Sole trader tax is reported and paid through Self Assessment. Every key date for the 2025/26 year:

- 5 October 2025 — deadline to register for Self Assessment if you started trading in 2025/26

- 31 January 2026 — online filing deadline for 2024/25 returns; also the payment deadline for your 2024/25 balancing payment

- 31 July 2026 — second payment on account for 2025/26

Our step-by-step guide on completing your Self Assessment tax return takes you through the full process, from logging into your HMRC account to submitting the final return.

Payments on Account — The Cash Flow Trap Nobody Warns You About

This is what blindsides most people in their second year of trading.

Once your tax bill tops £1,000 and less than 80% was collected at source, HMRC requires advance payments. You pay your bill in two instalments — 31 January and 31 July — with each instalment set at 50% of the previous year’s bill.

Here’s what it looks like in practice. Your first full year of trading, your tax bill comes to £5,000. On 31 January:

- £5,000 due for the previous year

- £2,500 due as the first payment on account for the current year

Total: £7,500 in one month. The second £2,500 follows in July.

New sole traders who aren’t expecting this find year two extremely difficult. The fix is straightforward: set aside 25–30% of every payment you receive into a separate account throughout the year.

Missing the 31 January deadline triggers an automatic £100 penalty from day one, with further charges applied at three months, six months, and twelve months. You can see the full penalty escalation in our guide to late Self Assessment penalties and how to appeal.

VAT: When It Becomes Mandatory

VAT and income tax are separate obligations. You can owe income tax without being VAT-registered.

VAT registration is mandatory when your taxable turnover exceeds £90,000 in any rolling 12-month period. The threshold is based on gross income, not profit. Once registered, you charge VAT on eligible sales, typically at 20%, and pay the net amount to HMRC quarterly.

If your turnover is approaching £90,000, read our VAT guide for UK small businesses before you cross the threshold. Registering late can result in back-charges and penalties.

Making Tax Digital for Income Tax — Live Now for £50,000+ Traders

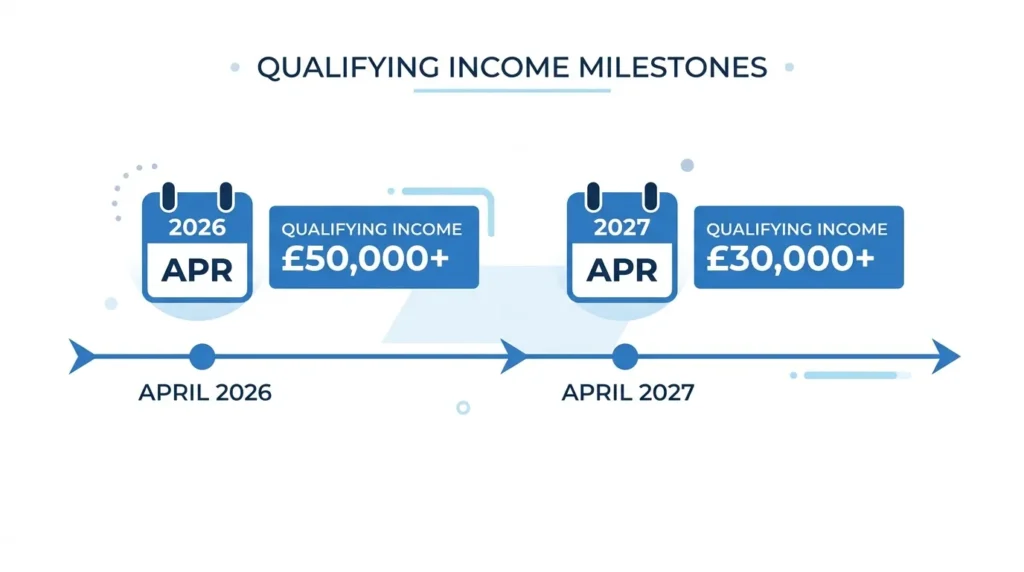

Making Tax Digital for Income Tax (MTD for ITSA) is no longer a future change for higher-earning sole traders. It is live.

From April 2026, sole traders with qualifying income above £50,000 must submit quarterly digital updates to HMRC using approved software. A single annual Self Assessment return is no longer sufficient.

The rollout then continues:

- April 2027 — mandatory for qualifying income above £30,000

“Qualifying income” includes trading profit plus property income. If you receive rental income alongside self-employment earnings, both count toward the threshold.

In practice, this means four quarterly submissions per year instead of one annual return. Each quarterly update reports your income and expenses for that period. A final declaration at year end confirms the totals.

If you’re above the £50,000 threshold and haven’t set up compatible software, you’re already in the window. Our dedicated guide to Making Tax Digital for sole traders covers which software qualifies, how the quarterly process works, and what HMRC checks at each stage.

Sole Trader vs Limited Company: When the Numbers Shift

At lower profit levels, staying sole trader is usually the simpler and often cheaper choice when accountancy costs are included.

Above £50,000–£60,000 in profit, a limited company structure becomes increasingly worth looking at. Corporation Tax rates are 19% on profits up to £50,000, rising to 25% on profits above £250,000. Directors can draw income as a combination of salary and dividends rather than taking everything as profit — a split that reduces the NI burden significantly.

The right answer depends on your profit level, how much income you need to draw from the business each year, and whether you plan to retain earnings. Our sole trader vs limited company comparison for 2026 puts the numbers side by side at different income levels so you can see the actual difference for your situation.

What to Do Before the January Deadline

Five practical actions worth taking now:

- Set aside 25–30% of every payment received into a separate account. Treat it as untouchable. It covers income tax, NI, and the payments on account.

- Keep a record of every business expense, however small. Missing receipts means missed deductions.

- Check your National Insurance record on the HMRC website to confirm State Pension contributions are being credited.

- Register for Self Assessment by 5 October if this is your first trading year — missing that deadline attracts immediate penalties.

- Make a pension contribution before 5 April 2026 to reduce this year’s taxable profit. Even a modest contribution makes a measurable difference.

If your profit is above £50,000 and you haven’t looked at MTD-compatible software, that needs to happen this year. Quarterly submissions are already a legal requirement.

{kind=link}