R&D tax relief lets UK limited companies reduce their Corporation Tax bill, or claim a cash credit, for money spent solving genuine scientific or technological problems. Since April 2024, almost every company claims through one of two routes: the merged R&D expenditure credit (RDEC) scheme, or Enhanced R&D Intensive Support (ERIS) for loss-making, R&D-intensive SMEs. This guide walks through eligibility, qualifying costs, the current rates, and the exact submission steps HMRC expects you to follow.

Understanding UK R&D Tax Relief: What It Is & Why It Matters

R&D tax relief is a government incentive that reduces the cost of innovation for UK companies. It exists because private companies tend to under-invest in research relative to the benefit it creates for the wider economy — HMRC’s own guidance frames this as correcting a market failure. If you’re weighing this against other funding routes, it’s worth comparing it with UK startup grants, since grant funding can affect which R&D scheme applies to your claim.

Key Reforms for Accounting Periods from April 2024

For accounting periods starting on or after 1 April 2024, the old SME scheme and the old RDEC scheme were replaced by two reliefs:

- The merged RDEC scheme — the default for most companies, regardless of size.

- ERIS — a more generous route reserved for loss-making SMEs that spend heavily on R&D.

HMRC introduced this change to simplify a system that had become a target for fraudulent and inflated claims, and to bring SME and large-company rules closer together. If your accounting period started before 1 April 2024, the old SME and RDEC rules still apply to that period — don’t apply 2024-onwards rates retrospectively.

The Financial Benefit: Lower Corporation Tax or a Cash Credit

Under the merged scheme, you receive a taxable credit worth 20% of qualifying R&D spend. Because that credit is itself subject to Corporation Tax, the real-world net benefit is typically 15% to 16.2% of qualifying expenditure, depending on your tax rate. Loss-making SMEs that qualify for ERIS can receive a payable credit worth up to roughly 27p for every £1 spent, because ERIS combines an enhanced 86% deduction with a 14.5% payable credit on the resulting loss.

Eligibility for R&D Tax Relief: Does Your Project Qualify?

Only limited companies liable to UK Corporation Tax can claim — sole traders and partnerships cannot. If you haven’t yet incorporated, it’s worth reading up on how to register a company in the UK before pursuing a claim, and comparing structures via sole trader vs limited company if you’re still deciding.

What Counts as Qualifying R&D for Tax Purposes

A project qualifies when it seeks an advance in science or technology and involves resolving scientific or technological uncertainty — meaning a competent professional in the field couldn’t readily work out the solution in advance. This is a technical test, not a commercial one. A project can fail commercially and still qualify; equally, a commercially successful product built entirely from known techniques won’t qualify.

The competent professional — typically a senior engineer, scientist, or technical lead — is central to a strong claim. HMRC expects their judgement, and their account of what was uncertain and how it was resolved, to run through the technical narrative.

What Does NOT Qualify

- Routine software configuration, bug fixes, or applying existing techniques with no genuine uncertainty

- Market research, design for aesthetic (non-technical) reasons, or commercial trial and error

- Work that simply follows a known, published method

Identifying & Tracking Qualifying R&D Expenditure

You can typically claim for:

| Cost category | What’s included |

|---|---|

| Staff costs | Salaries, employer NICs, pension contributions for staff directly engaged in R&D |

| Externally Provided Workers (EPWs) | Agency staff working directly on R&D, subject to connected-party rules |

| Subcontracted R&D | Costs paid to a subcontractor, now subject to new “who claims” rules based on who initiated the R&D |

| Consumables | Materials and utilities consumed or transformed during R&D |

| Software & cloud computing | Licences, data, and cloud costs directly used for R&D |

| Clinical trial volunteers | Payments to participants in clinical trials |

Capital expenditure, rent, patent filing costs, and production/distribution costs are excluded. Since 2024, relief for overseas subcontractors and EPWs is largely restricted to UK-based work, with narrow exceptions where the conditions needed for the R&D (specific expertise, environment, or legal requirements) genuinely don’t exist in the UK.

If you’re building your record-keeping around this, it’s worth cross-referencing your wider approach to claiming business expenses in the UK, since R&D costs still need to tie back to your normal accounting records.

Choosing the Right Scheme: Rates & Rules for 2026

| Scheme | Who it’s for | Headline rate | Typical net benefit |

|---|---|---|---|

| Merged RDEC scheme | Most companies, profitable or loss-making, accounting periods from 1 April 2024 | 20% taxable credit | ~15–16.2% |

| ERIS | Loss-making SMEs with R&D spend ≥30% of total expenditure | 86% enhanced deduction + 14.5% payable credit | up to ~27% |

You only need to meet the 30% R&D intensity threshold in the claim period itself, or in the prior 12-month period if you met it then. Companies eligible for ERIS can still choose to claim under the merged scheme instead, but not both for the same expenditure.

Grants and subsidies used to complicate SME claims under the old rules. Under the merged scheme and ERIS, grants no longer restrict which scheme you use in the way they once did — though how a grant is structured can still affect your total qualifying spend, so it’s worth checking with an adviser if you’ve received public funding.

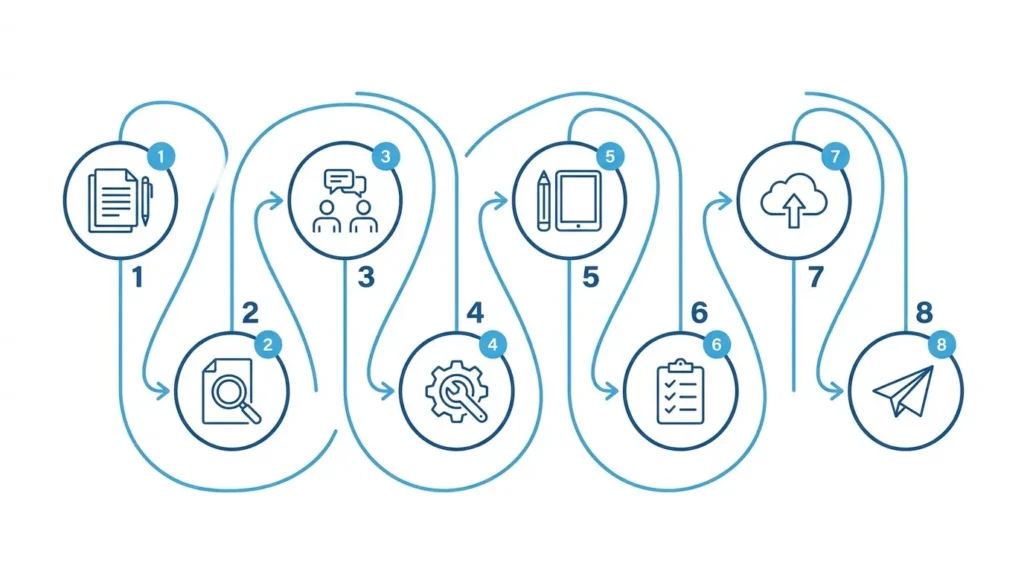

Your 8-Step Process to Making a UK R&D Tax Relief Claim

- Document your qualifying projects and costs systematically, as the work happens — not retrospectively.

- Confirm which scheme applies — merged RDEC or ERIS — based on your profit position and R&D intensity.

- Submit a Claim Notification to HMRC if this is your first claim, or you haven’t claimed in the previous three years. This is due within six months of the end of your accounting period, and missing it means you lose the right to claim for that period entirely.

- Complete the Additional Information Form (AIF), covering your projects, the technical uncertainty involved, and a cost breakdown.

- Prepare a technical report setting out the advance sought and uncertainty resolved — not mandatory, but the single strongest defence against an enquiry.

- Finalise your Corporation Tax computations, incorporating the R&D credit or enhanced deduction.

- Submit your CT600, with the CT600L supplementary page for R&D claims.

- Wait for processing. HMRC’s standard target is 40 days for the majority of claims, though claims flagged for review take considerably longer.

Crucial submission order: the AIF must be submitted before or alongside your CT600 — never after. A CT600 filed without a linked AIF will have its R&D claim automatically stripped out, usually without warning.

Essential Considerations for a Compliant Claim

Build your audit trail as you go. Contemporaneous notes — meeting minutes, technical logs, timesheets — carry far more weight with HMRC than a narrative reconstructed months later.

Know the red flags that trigger enquiries: vague technical descriptions, round-number cost estimates with no supporting workings, claims that read like a product spec rather than a technical account of uncertainty, and R&D intensity figures that shift suspiciously close to the 30% threshold.

Deadlines: claims must be submitted within two years of the end of the relevant accounting period. For a period ending 31 March 2025, that’s 31 March 2027.

Advance assurance is available to smaller, first-time claimants and offers HMRC pre-approval of your approach, though take-up has been limited given eligibility restrictions.

If you’re not confident preparing this yourself, it sits alongside other compliance-heavy areas like Making Tax Digital and self assessment tax returns where getting professional input early tends to save money later. A specialist adviser is particularly worth it if your R&D spans multiple projects, involves subcontractors, or if you’ve had a claim queried before — see our broader guide to R&D tax credits for UK small businesses for a wider view of when specialist support pays for itself.

R&D Tax Relief FAQs (2026)

Can I claim if my company is loss-making? Yes. Loss-making companies can claim under the merged scheme (carrying the credit forward if it exceeds the PAYE cap) or, if R&D-intensive, under ERIS for a larger payable credit.

How far back can I claim R&D tax relief? Within two years of the end of the accounting period the expenditure relates to. You cannot claim for older periods once that window closes.

What happens if HMRC queries my claim? HMRC opens a compliance check, requesting further evidence of the technical uncertainty and cost calculations. Strong contemporaneous documentation resolves most enquiries without adjustment; weak evidence can lead to the claim being reduced, rejected, or penalised.

Is software development eligible? Yes, where it involves genuine technical uncertainty — for example, building novel algorithms or architecture that existing tools and methods can’t readily achieve. Standard app development using established frameworks generally doesn’t qualify.

What is the PAYE cap? It limits how much payable credit you can receive to £20,000 plus 300% of your relevant PAYE and NIC liabilities for the period. Amounts above the cap under the merged scheme carry forward to the next period rather than being lost.

Getting your Corporation Tax position right alongside an R&D claim matters too — see our guide to the current UK Corporation Tax rate for how the credit interacts with your overall tax bill.

{kind=link}