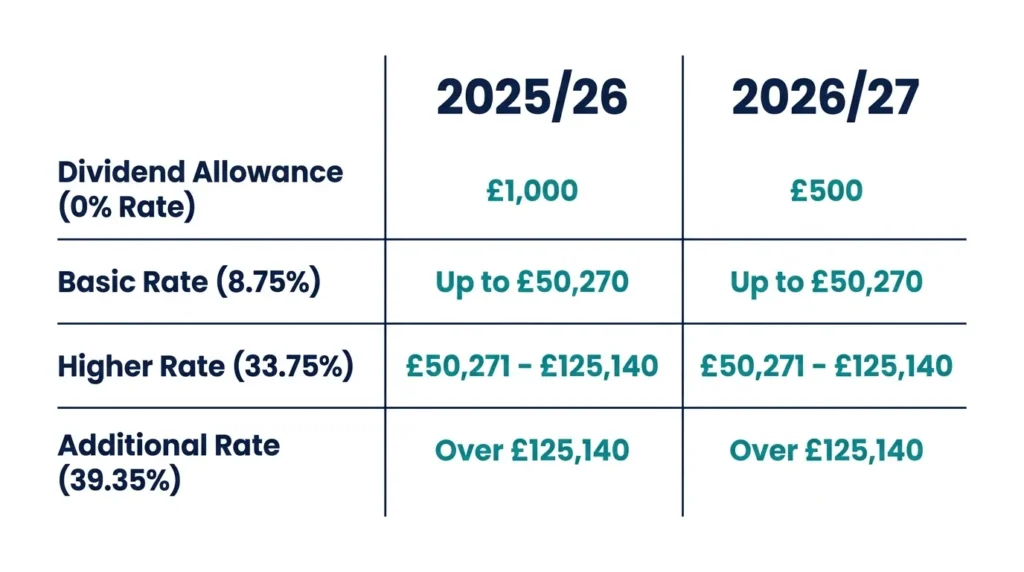

For the 2026/27 tax year (6 April 2026 to 5 April 2027), the dividend allowance stays at £500 — the same as the previous two years. What’s changed is the rate you pay above it. Following Autumn Budget 2025, the basic and higher dividend tax rates each rose by two percentage points: from 8.75% to 10.75%, and from 33.75% to 35.75%. The additional rate holds at 39.35%.

Same dividend, higher bill, even though the tax-free slice hasn’t moved. If you’re a director or investor drawing dividends this year, that rate rise is the number to plan around.

| 2025/26 | 2026/27 | |

|---|---|---|

| Dividend allowance | £500 | £500 |

| Basic rate | 8.75% | 10.75% |

| Higher rate | 33.75% | 35.75% |

| Additional rate | 39.35% | 39.35% |

| Personal Allowance | £12,570 | £12,570 |

| Higher rate threshold | £50,270 | £50,270 |

| Additional rate threshold | £125,140 | £125,140 |

Personal Allowance and Income Tax thresholds are frozen at these levels until April 2031, following the extension confirmed at Autumn Budget 2025. That freeze matters almost as much as the rate rise: as wages and dividends grow, more income gets pulled into higher bands even though the bands themselves stand still. See our Personal Allowance guide for how this interacts with your salary specifically.

What Is the Dividend Allowance for 2026/27?

The dividend allowance is the amount of dividend income you can receive each tax year before dividend tax applies. For 2026/27, that’s £500, renewing every 6 April, and it applies regardless of which Income Tax band you’re in.

It isn’t extra tax-free income stacked on top of your other allowances — it’s a 0% rate on the first slice of your dividends. It still counts toward working out which tax band you’re in, even though nothing is charged on it.

Dividend Allowance vs. Personal Allowance

Mixing these two up is the most common error in DIY dividend tax estimates. Your Personal Allowance (£12,570) is the total income — salary, pension, dividends, anything — you can earn tax-free. Your dividend allowance (£500) only ever applies to dividends, and only after your Personal Allowance is used up elsewhere.

If dividends are your only income, both apply together: £12,570 tax-free under your Personal Allowance, plus £500 under your dividend allowance, giving £13,070 tax-free in total. If a salary or pension already uses your Personal Allowance, only the £500 dividend allowance remains.

Dividend Tax Rates and Bands for 2026/27

| Tax band | Taxable income range | Dividend tax rate 2026/27 |

|---|---|---|

| Basic rate | £12,571 – £50,270 | 10.75% |

| Higher rate | £50,271 – £125,140 | 35.75% |

| Additional rate | Over £125,140 | 39.35% |

These rates and thresholds are the same in England, Wales and Northern Ireland. Scottish taxpayers use Scottish bands for salary and other non-savings income, but dividend income still follows the UK-wide rates and thresholds above. For the full rate breakdown by band, see our dedicated UK dividend tax rates guide.

How Dividends Stack on Top of Other Income

HMRC always taxes dividends as the top slice of income, after salary, self-employment profit, pensions and savings interest. This is the rule most self-calculations get wrong.

The order is fixed: non-savings income first, then savings income, then dividends last. So the band your dividends land in depends on how much other income you already have — not on the size of the dividend itself. A £5,000 dividend is tax-free for someone with no other income, and taxed at 35.75% for someone with a £60,000 salary.

How to Calculate Your Dividend Tax: Worked Examples

Case Study 1: The Company Director

Salary of £12,570 (matching the Personal Allowance, so no tax or NI on it) plus £40,000 in dividends.

- First £500 of dividends: dividend allowance, 0%

- Next £37,700: basic rate band, 10.75% = £4,051.75

- Remaining £1,800: higher rate band, 35.75% = £643.50

Total dividend tax: £4,695.25, leaving take-home income of £47,874.75 on £52,570 total. This is illustrative only — your actual liability depends on your full income picture. Our guide on paying yourself as a limited company director covers structuring this properly.

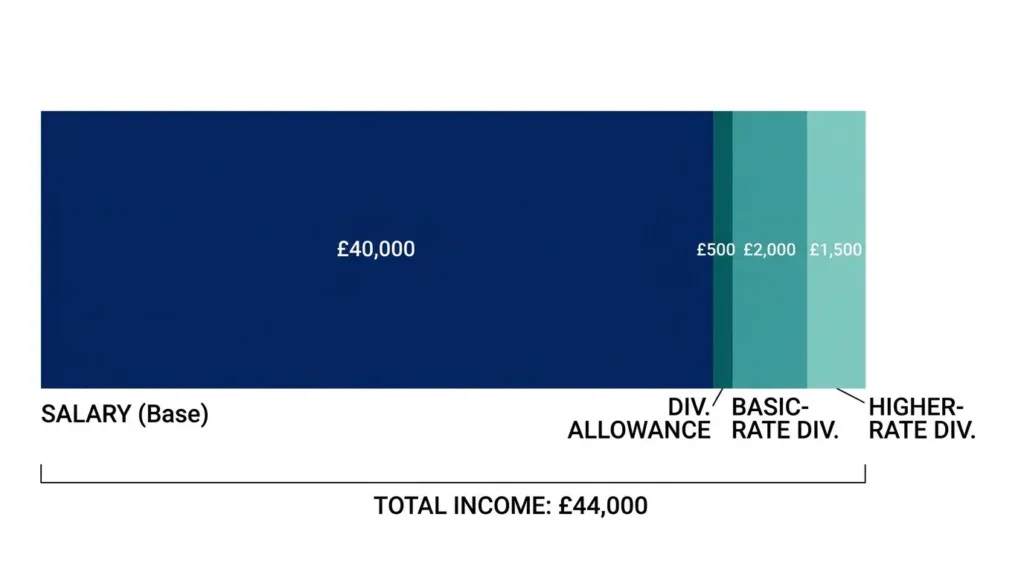

Case Study 2: The Investor With Salary and Shares

£45,000 salary plus £8,000 in dividends from shares held outside an ISA.

- Personal Allowance covers the first £12,570 of salary; the remaining £32,430 is taxed at the normal 20% rate

- That leaves £5,270 of basic rate band before dividends start

- £500 dividend allowance uses the first slice at 0%

- Next £4,770 of dividends: 10.75% = £512.78

- Remaining £2,730: crosses into higher rate, 35.75% = £976.10

Total dividend tax: roughly £1,489. Because total dividend income is under £10,000, this investor doesn’t automatically need to register for Self Assessment — more on that below.

The Double Taxation Trap: Corporation Tax Plus Dividend Tax

If you run a limited company, dividends come from profit that’s already been taxed once. Corporation Tax applies first — 19% on profits up to £50,000, 25% above £250,000, with marginal relief tapering the rate in between — and only what’s left can be distributed as dividends. You then pay dividend tax on top as a shareholder.

Quoting dividend tax alone understates what a director really loses. Here’s what it takes to deliver £1,000 net into a shareholder’s pocket in 2026/27:

| Scenario | Corporation Tax | Dividend tax | Pre-tax profit needed for £1,000 net |

|---|---|---|---|

| Small profits, basic-rate shareholder | 19% | 10.75% | approx. £1,383 |

| Larger profits, higher-rate shareholder | 25% | 35.75% | approx. £2,075 |

In the second scenario, over half of the original profit is gone before the shareholder sees anything. Model this combined bite before deciding how much to extract and when — see our Corporation Tax rates guide for the full band breakdown.

How to Pay Tax on Dividends to HMRC

Dividend tax is reported and paid through Self Assessment, using the dividends section of the standard SA100 form.

- Add up total dividend income, excluding anything from a Stocks and Shares ISA

- Deduct unused Personal Allowance, then the £500 dividend allowance

- Work out which band the remainder falls into

- Declare the full dividend income (not just the taxable portion) on your return

- Pay by 31 January following the tax year end — 31 January 2028 for 2026/27 dividends

Do You Need to Register for Self Assessment?

You must register and file if dividend income is over £10,000 in the tax year — even if it’s your first return, and even if the tax owed is small.

Under £10,000 but still above your allowances? Registration isn’t automatic, but you must tell HMRC by 5 October following the tax year so it can adjust your PAYE code or arrange payment. Miss that window and a late-notification penalty can apply even on a small bill. Check our guides to completing a Self Assessment return and late filing penalties before assuming you can leave it until January.

ISA dividends don’t need reporting at all — they’re outside the tax system entirely.

Legal Strategies to Reduce Your Dividend Tax Bill

1. Use your Stocks and Shares ISA. Shelter up to £20,000 a year for 2026/27. Dividends earned inside it are entirely tax-free and never reportable. This doesn’t cover your own private company’s shares, but it’s the simplest fix for a personal investment portfolio.

2. Split shares with a spouse or civil partner. If they pay tax at a lower rate, transferring shares moves dividend income into their allowance and band instead of yours. Spousal transfers are exempt from Capital Gains Tax, but HMRC expects the transfer to be genuine — they must actually hold the shares and be entitled to the income.

3. Redirect dividends into pension contributions. Company pension contributions are usually paid from pre-tax profit, sidestepping both Corporation Tax and dividend tax on that portion. It’s an alternative to taking dividends, not a way to shelter ones you’ve already drawn.

4. Get your salary-to-dividend ratio right. Most directors do best paying a salary around the Personal Allowance or NI threshold, then taking dividends — which avoid National Insurance entirely. But pushing dividends past £50,270 total income tips a chunk into the 35.75% band, so model the split before the tax year starts rather than after. If you’re comparing structures altogether, our sole trader vs limited company guide covers when incorporation is actually worth it.

The £100,000 Trap: Watch the Personal Allowance Taper

Between £100,000 and £125,140 of total income, your Personal Allowance is withdrawn at £1 for every £2 earned above £100,000. For salary taxed at 40%, this creates the well-known 60% effective marginal rate. For dividends already in the higher-rate band, the same mechanic pushes the effective marginal rate to roughly 53.6% — every extra pound drags an extra 50p of previously tax-free allowance into the 35.75% band.

If your income sits in this range, pension contributions that bring you back under £100,000 can restore your Personal Allowance and meaningfully cut your effective rate. This is worth a proper calculation rather than a rule of thumb.

Common Mistakes to Avoid

Using an outdated allowance figure. The allowance has fallen sharply since 2017 — from £5,000, to £2,000, to £1,000, and now £500. Always confirm you’re working from the current £500 figure.

Forgetting the allowance still uses up your band. The first £500 is taxed at 0%, but it still occupies space in your band. Near the higher rate threshold, that £500 can decide whether all your dividends stay basic rate or a slice tips into higher rate.

Ignoring Corporation Tax already paid. Dividends come from post-tax company profit. Quoting only the personal dividend rate understates your real burden as a business owner.

Missing the 5 October registration deadline. If you owe dividend tax and don’t already file Self Assessment, tell HMRC by 5 October following the tax year — even a small liability can trigger a penalty if you miss it.

Assuming dividends work like salary for expenses. You can’t deduct expenses against dividend income. It’s taxed on the full amount received, with only the allowances above to offset it.

Frequently Asked Questions

How much dividend can I pay myself tax-free in 2026/27? Up to £13,070 if dividends are your only income — £12,570 Personal Allowance plus £500 dividend allowance. If salary or pension already uses your Personal Allowance, only £500 remains tax-free.

What are the dividend tax rates for 2026/27? 10.75% basic rate, 35.75% higher rate, 39.35% additional rate, applied above your allowances.

Does the dividend allowance reduce my Personal Allowance? No. They’re separate and work together — the dividend allowance applies only to dividends, on top of whatever Personal Allowance is left after other income.

How do I report dividend income under £10,000? Registration isn’t automatic below £10,000, but contact HMRC by 5 October after the tax year ends; it can usually collect what’s owed through your PAYE tax code.

Do I pay National Insurance on dividends? No — one reason many directors take a low salary and top up with dividends.

Are dividends from ISA shares taxable? No. Dividends inside a Stocks and Shares ISA are completely tax-free and don’t need reporting, regardless of amount.

Do dividend tax rates differ in Scotland? No. Scottish bands apply to salary, but dividend tax follows the same UK-wide rates and thresholds shown in this guide.

This article is for general guidance only and reflects UK tax rules for the 2026/27 tax year as confirmed at Autumn Budget 2025. It isn’t personal tax advice. Speak to a qualified accountant or tax adviser about your specific circumstances before making decisions based on it.

{kind=link}