Yes, you can claim Marriage Allowance if you’re self-employed. There’s no rule that excludes sole traders, partners, or company directors. What changes is how the saving reaches you — instead of a tax code adjusting your payslip, the £252 reduction shows up in your Self Assessment calculation, and getting the paperwork right matters more than it does for employees on PAYE.

This guide covers who qualifies, how the transfer affects your tax bill (and what it doesn’t touch), how to claim without duplicating your application, and how to backdate a claim worth up to £1,260.

What is the UK Marriage Allowance?

Marriage Allowance lets one spouse or civil partner transfer part of their unused Personal Allowance to the other, cutting the recipient’s Income Tax bill by up to £252 a year. It’s only available to married couples and civil partners — not cohabiting partners, however long you’ve lived together.

How the Personal Allowance Transfer Works

Every UK taxpayer gets a Personal Allowance — income you can earn before paying tax. For 2026/27 that’s £12,570, frozen until at least April 2028. If one partner doesn’t use their full allowance because their income sits below that figure, they can transfer 10% of it to their spouse or civil partner, who then pays tax on less of their income. The transfer isn’t flexible — you give up exactly 10% of the standard allowance, not a smaller amount of your choosing.

What is the Financial Value of the Claim? (Current & Backdated Rates)

For 2026/27, the transferable amount is £1,260 (10% of £12,570). Because the saving is calculated at the 20% basic rate, that’s a maximum of £252 a year (£1,260 × 20%). The Personal Allowance has been frozen at £12,570 since 2021/22, so the £252 saving has stayed identical for every year since — useful when backdating, because you don’t need to recalculate figures year by year.

Eligibility Rules: Can You Claim if You Are Self-Employed?

Self-employment doesn’t disqualify you. What matters is your income after allowable expenses — your taxable profit — not whether you’re on a payslip. HMRC applies the same three tests to a sole trader as to an employee: you’re married or in a civil partnership; one partner’s income is below the Personal Allowance; and the other is a basic-rate taxpayer, not higher or additional-rate.

The Income Thresholds Explained (2026/27)

| Test | England, Wales & Northern Ireland | Scotland |

|---|---|---|

| Transferring partner’s income | Below £12,570 | Below £12,570 |

| Receiving partner’s income (qualifying range) | £12,571 – £50,270 (basic rate) | £12,571 – roughly £43,662 (starter, basic or intermediate rate) |

| Disqualifying rate for the recipient | Higher (40%) or additional (45%) | Higher (42%) or top |

For a self-employed transferring partner, “income” means net taxable profit — turnover minus allowable business expenses — not gross revenue. This trips people up more than anything else in the eligibility test: a sole trader with £25,000 turnover and £14,000 of legitimate expenses has a taxable profit of £11,000, comfortably under the threshold, even though the turnover figure looks nowhere near it.

Scenario A: One Partner is Employed (PAYE), One is Self-Employed

This is the most common self-employed case. If the self-employed partner has low profits and the employed partner is a basic-rate taxpayer, the self-employed partner transfers the allowance, and HMRC adjusts the employed partner’s PAYE code — the saving appears automatically through payroll, no Self Assessment adjustment needed. If it’s the other way round, and the self-employed partner is the recipient, the saving instead has to land inside their Self Assessment calculation rather than a payslip — covered in the claiming section below.

Scenario B: Both Partners Are Self-Employed

Both of you can be sole traders, partners, or a mix of self-employment and other income, and still qualify, as long as one partner’s taxable profit is below £12,570 and the other’s sits within the basic-rate band. The complication is volatility: self-employed profits swing year to year in a way PAYE salaries don’t. A good year for the lower-earning partner can push them over the threshold and invalidate the whole claim, sometimes without either of you noticing until you prepare your returns the following January. If your household has two self-employed incomes, check projected profits before the tax year ends rather than assuming last year’s numbers still apply — business expenses you can legitimately claim can shift which partner ends up under the threshold.

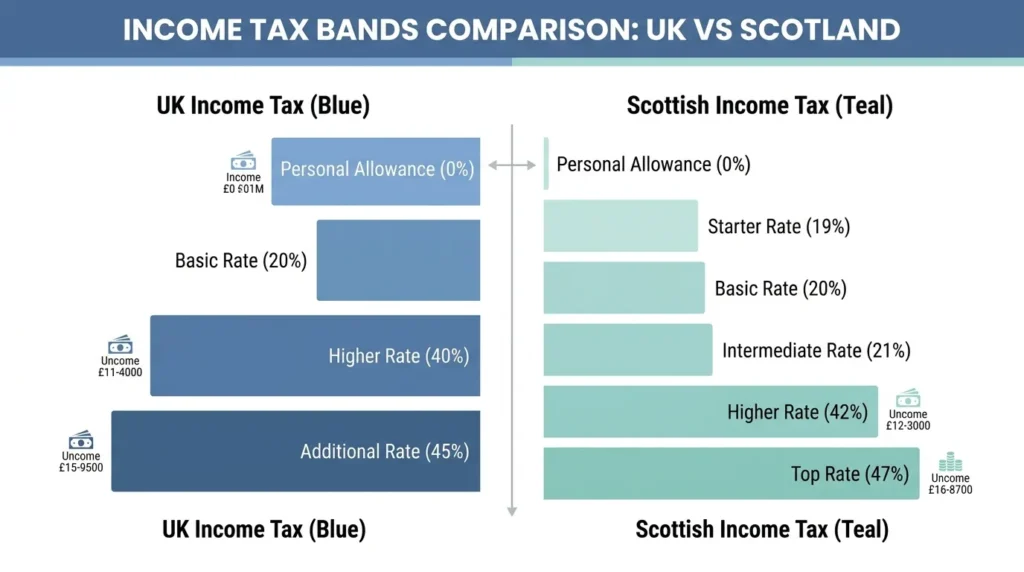

The Scottish Exception: How Different Tax Bands Affect Claims

Scotland uses its own Income Tax bands, which changes who counts as a “basic-rate taxpayer” for Marriage Allowance purposes. A Scottish-resident recipient still qualifies if they pay the starter, basic, or intermediate rate — broadly, income up to around £43,662 in 2026/27. Once they move into the Scottish higher rate (42%), they lose eligibility, even though the same income would still qualify someone in England, Wales, or Northern Ireland (higher-rate threshold £50,270).

This gap catches out Scottish sole traders with profits between roughly £43,662 and £50,270 — high enough to disqualify them under Scottish rates, though someone south of the border at the same income would still be eligible. Always check your Scottish tax band before assuming a claim will go through.

How to Claim Marriage Allowance When Self-Employed

There are two ways to apply, and they lead to the same result but suit different situations.

Method 1: Applying Online via Government Gateway (The Recommended Route)

This is HMRC’s preferred method and works whether you’re employed, self-employed, or both. The transferring partner (the lower earner) makes the application, not the recipient:

- Go to GOV.UK and sign in with a Government Gateway account (or create one).

- Confirm both partners’ National Insurance numbers.

- Provide ID verification details for the transferring partner if requested.

- Submit the application — HMRC typically processes it within a few weeks.

Once approved, HMRC updates both partners’ tax codes and, for the self-employed recipient, feeds the reduction directly into their next Self Assessment calculation. You don’t need to do anything further on your return once this is done — see the double-claim warning below.

Method 2: Claiming Directly on Your Self Assessment Tax Return (Form SA100)

If you haven’t already registered online, you can claim through your Self Assessment return instead. The recipient partner declares the amount received in the tax reliefs section of the main SA100 form (paper filers use the supplementary SA101 pages; the online return builds this section in automatically), and HMRC applies the reduction to that year’s calculation. This route suits people filing their return anyway, or backdating a claim for a year they’ve already missed.

How Your Tax Codes (M and N) Will Change

Everyone who registers for Marriage Allowance gets an updated tax code, even if that code isn’t actually applied to a payslip:

- The recipient’s code gains an M suffix. Their Personal Allowance rises from £12,570 to £13,830, giving a code like 1383M.

- The transferring partner’s code gains an N suffix. Their allowance falls from £12,570 to £11,310, giving a code like 1131N.

If you’re purely self-employed with no PAYE income, this code exists on HMRC’s system but has nothing to attach to — the saving simply appears as a lower liability on your SA302 calculation. If you also have part-time employment, the code applies to that income through PAYE, and the Self Assessment calculation adjusts to avoid double-counting.

Backdating Your Claim: How to Retrieve Up to £1,260

Marriage Allowance can be backdated for up to four previous tax years, as long as you were eligible in each one. Because both the Personal Allowance and the £252 saving have been unchanged since 2021/22, every eligible year is worth the same amount — no recalculating required.

The 4-Year Backdating Rule and Previous Tax Year Thresholds

A claim made during 2026/27 can currently be backdated as far as the 2022/23 tax year. Here’s what that’s worth:

| Tax year | Personal Allowance | Maximum saving |

|---|---|---|

| 2022/23 | £12,570 | £252 |

| 2023/24 | £12,570 | £252 |

| 2024/25 | £12,570 | £252 |

| 2025/26 | £12,570 | £252 |

| 2026/27 (current year) | £12,570 | £252 |

Claim all five eligible years in one application and the total comes to £1,260 — a single lump sum for the four backdated years plus the ongoing saving for the current one. The backdating window moves forward each April, so a year you were eligible for eventually drops out of scope if you don’t claim it — there’s no way to recover it later.

Step-by-Step Guide to Filling Out Your Self Assessment with Marriage Allowance

For self-employed taxpayers, this is where most of the confusion in Marriage Allowance guidance actually lives — and where most generic guides go quiet.

- Check whether you’re already registered. Log into your Government Gateway personal tax account and check your Marriage Allowance status before touching your return.

- If you’re not registered, decide which route to use. Apply online first if you want the saving to flow through to any PAYE income too; use the SA100 tax reliefs section if you’d rather deal with it entirely within your return.

- Complete your self-employment pages (SA103) as normal. Marriage Allowance doesn’t change how you report income or expenses — it’s applied afterwards, at the calculation stage.

- Enter your Marriage Allowance details only once, using whichever method you haven’t already used elsewhere.

- Check your SA302 tax calculation once submitted to confirm the £252 reduction (or backdated total) has actually been applied.

- Review your payments on account for the following year — this is where an easy extra saving hides, covered below.

What Happens if You Already Registered Online?

If you’ve already applied through Government Gateway, HMRC’s systems already know about the transfer and build it into your Self Assessment calculation automatically. You do not need to also declare it again on your SA100.

Avoiding Double Claims and Calculation Errors on Your Tax Bill

This is the single most common mistake self-employed claimants make, and it’s almost never mentioned in general guidance: completing the Marriage Allowance section on your SA100 after you’ve already registered online.

When this happens, HMRC’s system sometimes attempts to process two separate adjustments for the same transfer. The usual outcome is a calculation error flagged for manual review — delaying your tax calculation and occasionally your refund — rather than an actual double benefit, since HMRC’s systems are built to catch genuine duplication. But it still means extra correspondence, a slower turnaround, and sometimes a corrected calculation you’ll need to accept or dispute.

The rule to remember: claim once, through one method, and check your personal tax account before you touch your Self Assessment return.

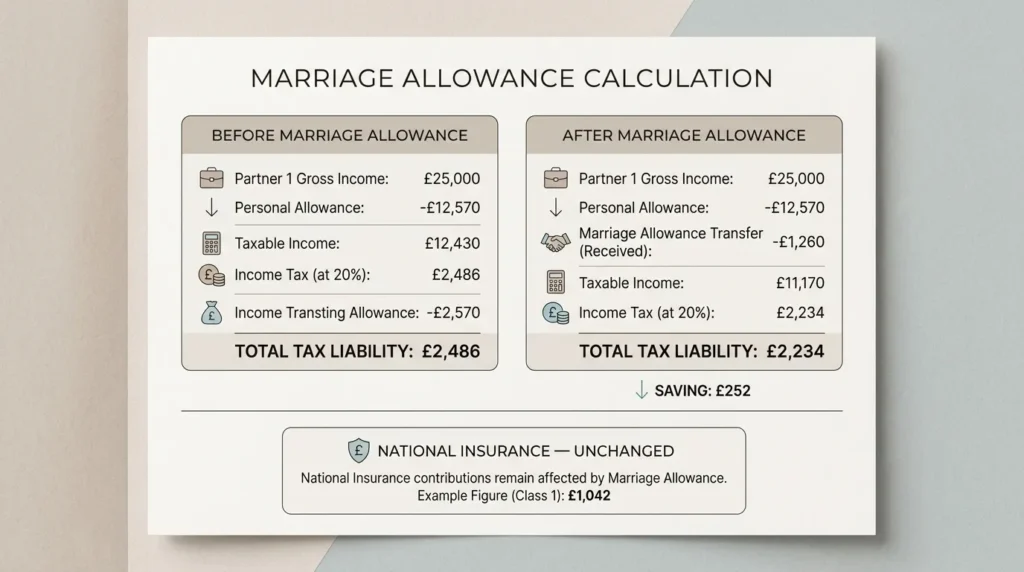

A Worked Example: How Marriage Allowance Actually Affects a Sole Trader’s Bill

Most guidance stops at “your tax bill is reduced” without showing the maths — and self-employed taxpayers need to see what it doesn’t reduce.

Rania is a self-employed graphic designer with a taxable profit of £30,000 for 2026/27. Her husband, Tom, earns £9,500 part-time — well under the Personal Allowance — so he transfers £1,260 to her.

Income Tax, before Marriage Allowance: (£30,000 − £12,570) × 20% = £3,486.00

Income Tax, after Marriage Allowance: Rania’s Personal Allowance rises to £13,830. (£30,000 − £13,830) × 20% = £3,234.00

Saving: £252.00 — exactly as expected.

Class 4 National Insurance is unaffected either way: (£30,000 − £12,570) × 6% = £1,045.80

Marriage Allowance only reduces Income Tax liability. It has no effect on Class 2 or Class 4 National Insurance contributions, which are calculated on the same profit figure regardless of any allowance transfer.

There’s a second, quieter benefit too. Because Rania’s total Self Assessment liability for the year is now £252 lower, her payments on account for the following year — each set at 50% of the prior year’s tax liability — drop as well. That means the cash-flow benefit of claiming Marriage Allowance is often slightly larger than the headline £252 figure once you account for reduced payments on account the following January and July.

What Happens if Your Circumstances Change?

Marriage Allowance isn’t a one-off decision — it needs revisiting whenever your income or your relationship status changes.

If Your Income Rises Above the Threshold

If the transferring partner’s profit rises above £12,570, or the recipient’s income moves into the higher-rate band, the claim needs to be cancelled. HMRC sometimes catches this using information from your Self Assessment return, but self-employed income is unpredictable enough that it’s worth cancelling through your personal tax account as soon as you know your profits will exceed the threshold, rather than waiting for HMRC to notice. Leave it too late and you may owe back some or all of the saving.

Divorce, Separation, or the Death of a Partner

Marriage Allowance ends automatically on divorce or dissolution of a civil partnership, from the date the decree absolute or final order is granted. If a partner dies, the claim can continue for that tax year, and any previously unclaimed backdated years remain claimable by the surviving partner or their estate.

Frequently Asked Questions (FAQs)

Do I put Marriage Allowance on my Self Assessment? Only if you haven’t already registered online. If you applied through Government Gateway, HMRC applies the reduction automatically — entering it again on your return can trigger a duplicate-claim error.

How does Marriage Allowance affect my self-employed tax bill? It increases your Personal Allowance (recipient) or reduces it (transferor), changing how much taxable profit is subject to Income Tax. It has no effect on Class 2 or Class 4 National Insurance.

Can two self-employed partners both claim Marriage Allowance? Yes, as long as one partner’s taxable profit is below £12,570 and the other’s falls within the basic-rate band — up to £50,270 in England, Wales and Northern Ireland, or roughly £43,662 in Scotland.

Does Marriage Allowance reduce my National Insurance? No. It only reduces Income Tax. Class 2 and Class 4 NI are calculated on your full taxable profit regardless of any transfer.

How far back can I backdate a claim? Up to four previous tax years plus the current one, provided you were eligible in each. In 2026/27, that covers 2022/23 through to the present.

What if my partner has died? You can still claim, including backdated years, as long as you were eligible during the years in question.

Is Marriage Allowance the same as Married Couple’s Allowance? No. Married Couple’s Allowance is separate and generally more valuable, for couples where at least one partner was born before 6 April 1935. You cannot claim both.

{kind=link}