IR35 decides whether you pay tax as an employee or as a genuine business. Get it wrong and HMRC can come after backdated tax, interest, and penalties. Get it right and you keep the tax efficiency that comes with running your own limited company.

This guide breaks down what IR35 actually means, how status gets decided, and what changed in April 2026 — because two separate updates landed this year, and most guides only cover one of them.

What Is IR35?

IR35 is UK tax legislation that stops contractors from working like employees while paying tax like a business. HMRC calls it the off-payroll working rules.

The name comes from Inland Revenue press release number 35, issued in 1999, when the rules were first announced. They took effect in April 2000.

The legislation targets what HMRC calls disguised employment. Picture someone who leaves a permanent job on a Friday, sets up a limited company over the weekend, and returns to the same desk on Monday doing the same work for the same manager. Without IR35, that person could pay themselves through dividends and save thousands a year in tax and National Insurance, despite nothing about the actual job changing.

IR35 closes that gap. If your working arrangement looks like employment, you pay tax like an employee — regardless of what your contract says.

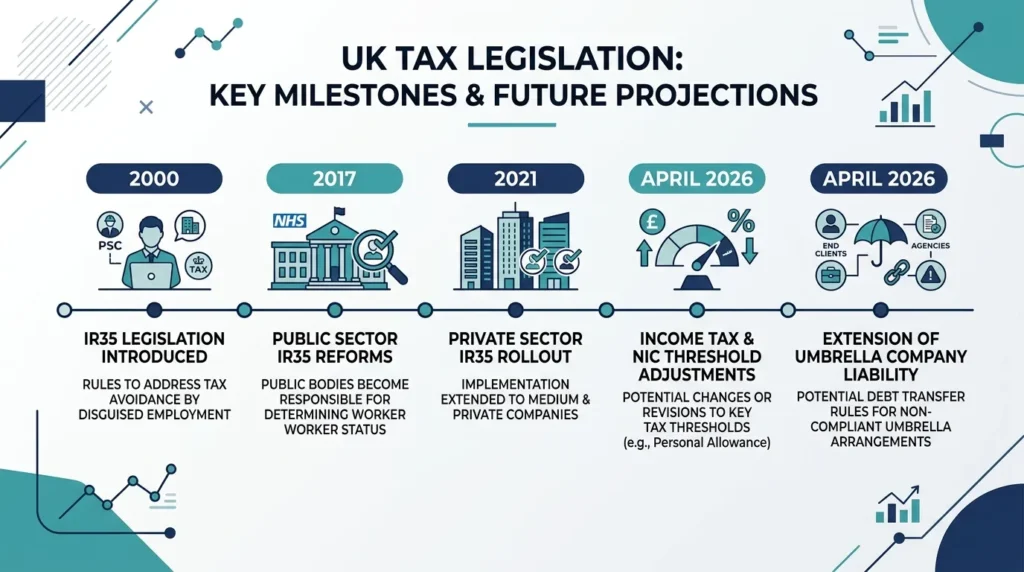

A Short History of the Off-Payroll Rules

IR35 isn’t one fixed law. It has been reformed three times since 2000, and two more changes landed in 2026.

2000 — Original IR35. Sits in Chapter 8 of the Income Tax (Earnings and Pensions) Act 2003 (ITEPA 2003). The contractor’s own limited company was responsible for deciding its own status. Self-policing didn’t work well — compliance was patchy and enforcement was slow.

2017 — Public sector reform. Responsibility for the status decision moved from the contractor’s company to the public sector body engaging them.

2021 — Private sector reform. The same shift extended to medium and large private sector businesses. If you contract for a company that isn’t classed as small, your client — not you — decides your IR35 status.

April 2026 — Small company threshold change. The financial thresholds that define a “small” company rose, shifting the status decision back to the contractor for some engagements. Detailed below.

April 2026 — Joint and several liability for umbrella companies. Separate legislation makes agencies and end clients liable for unpaid PAYE if an umbrella company in the supply chain fails to pay correctly.

Who Does IR35 Apply To?

IR35 applies to anyone who provides personal services to a client through an intermediary — almost always a personal service company (PSC), a limited company with the contractor as its main or only worker.

If you invoice a client through your own limited company rather than working as a permanent employee, IR35 is relevant to you. It doesn’t apply to genuine sole traders, since there’s no intermediary company in the chain. If you’re still deciding between structures, it’s worth understanding what a limited company actually is before contracting through one.

Who decides depends on your client’s size:

- Small clients — the contractor’s own PSC decides status, under Chapter 8

- Medium and large clients — the client decides, and must issue a Status Determination Statement

A company counts as small if it meets two of three criteria: turnover under £15 million, balance sheet total under £7.5 million, or fewer than 50 employees. These thresholds rose in April 2025, with the practical IR35 effect landing from 2026 for some businesses and 2027 for most — more on the timing below.

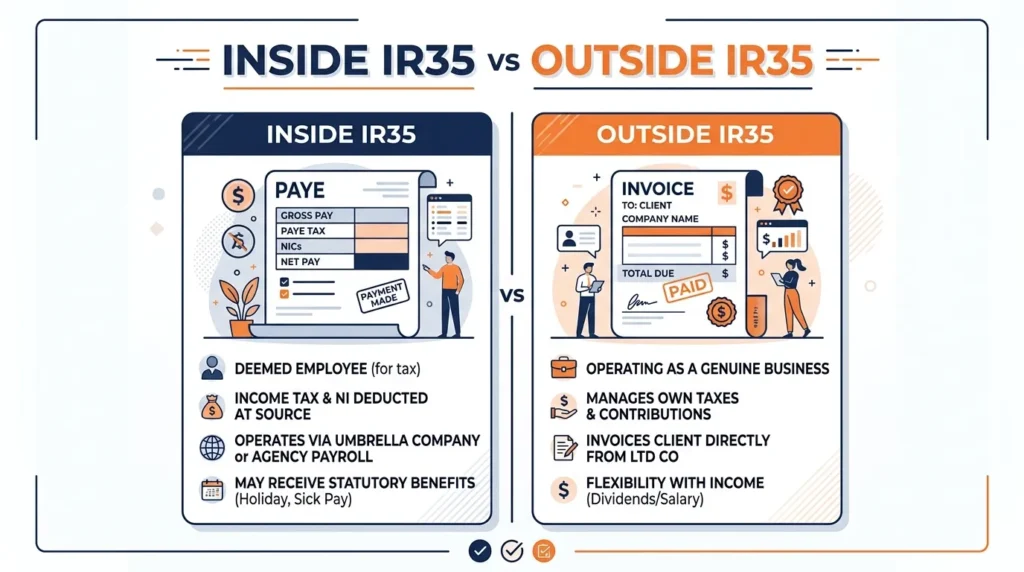

Inside IR35 vs Outside IR35

This is the single most important distinction in the whole system.

Inside IR35 means HMRC treats you as an employee for tax purposes on that engagement. Your client or the fee-payer deducts Income Tax and Class 1 National Insurance through PAYE before you’re paid, just like permanent staff.

Outside IR35 means you’re a genuine business. You’re paid gross through your limited company, pay Corporation Tax on profits, and draw income as a mix of salary and dividends — significantly more tax-efficient. If you’re outside IR35, how you structure paying yourself as a director has a real effect on what you keep.

| Inside IR35 | Outside IR35 | |

|---|---|---|

| Tax treatment | Taxed as an employee | Taxed as a business |

| Who deducts tax | Client or fee-payer, via PAYE | You, via your limited company |

| National Insurance | Employee and employer NIC apply | Standard business NIC rules |

| Income extraction | Salary only (PAYE) | Salary plus dividends |

| Expenses | Limited | Broader range of allowable expenses |

To put a number on it: a contractor billing £500 a day inside IR35 typically takes home noticeably less than the same contractor outside IR35, because dividend income is taxed differently from PAYE salary, and outside-IR35 contractors can claim more expenses against Corporation Tax. The exact gap depends on your overall income, which is why checking your dividend tax position matters before accepting an inside-IR35 rate.

How Is IR35 Status Decided? The Three Key Tests

HMRC and the courts don’t rely on the contract wording alone. What matters most is how the work actually happens day to day. Three tests carry the most weight, and none of them is decisive on its own — they’re weighed together.

1. Control. How much say does the client have over what you do, how you do it, when you do it, and where you do it? Genuine contractors control their own methods. Employees take direction.

2. Right of substitution. Can you send someone else to do the work in your place, and would the client accept that? A genuine, unfettered right of substitution is one of the strongest indicators of being outside IR35.

3. Mutuality of obligation (MOO). Is the client obliged to offer you work, and are you obliged to accept it? Genuine contracting is project-based — when the work is done, the obligation ends.

Beyond these three, HMRC also weighs financial risk, integration into the client’s organisation, and whether you can work for other clients at the same time.

The Status Determination Statement (SDS)

A Status Determination Statement is the formal document a medium or large client must produce, explaining whether an engagement falls inside or outside IR35 and the reasoning behind it.

Clients issuing an SDS must: take reasonable care reaching the decision, pass it to the worker and the next party in the supply chain, and keep records showing how the conclusion was reached. If a client fails to take reasonable care, responsibility for unpaid tax can fall back on the client itself.

Appealing a determination. If you disagree, the client must have a process for hearing it and respond within 45 days. The strongest appeals come with evidence — your actual contract and documentation of how the engagement runs in practice.

HMRC’s CEST Tool

CEST stands for Check Employment Status for Tax — HMRC’s free online tool, used by many clients to help reach an IR35 decision. It asks a series of questions about control, substitution, and the working relationship, then returns an inside, outside, or “unable to determine” result.

CEST has real limits. It doesn’t directly ask about mutuality of obligation in a way that fully reflects case law, and “unable to determine” results happen more often than clients expect. Treat CEST as a starting point, not the final word.

What Happens If You Get IR35 Wrong

If HMRC opens an enquiry and decides an engagement should have been inside IR35, the consequences land on whoever was responsible for the determination — the contractor’s PSC for small-client engagements, or the client/fee-payer for medium and large ones.

What’s typically due:

- Backdated Income Tax and National Insurance on the disputed payments

- Interest on the unpaid amount

- A behaviour-based penalty: lower for genuine mistakes made with reasonable care, up to 100% of the tax owed for deliberate, concealed non-compliance

HMRC can investigate going back several years, so the exposure from a wrong determination can be substantial. This is why accurate self-assessment record-keeping matters even when you’re confident you’re outside IR35.

What’s Changing in 2026

Two genuinely separate changes landed in 2026, and they’re easy to confuse with each other.

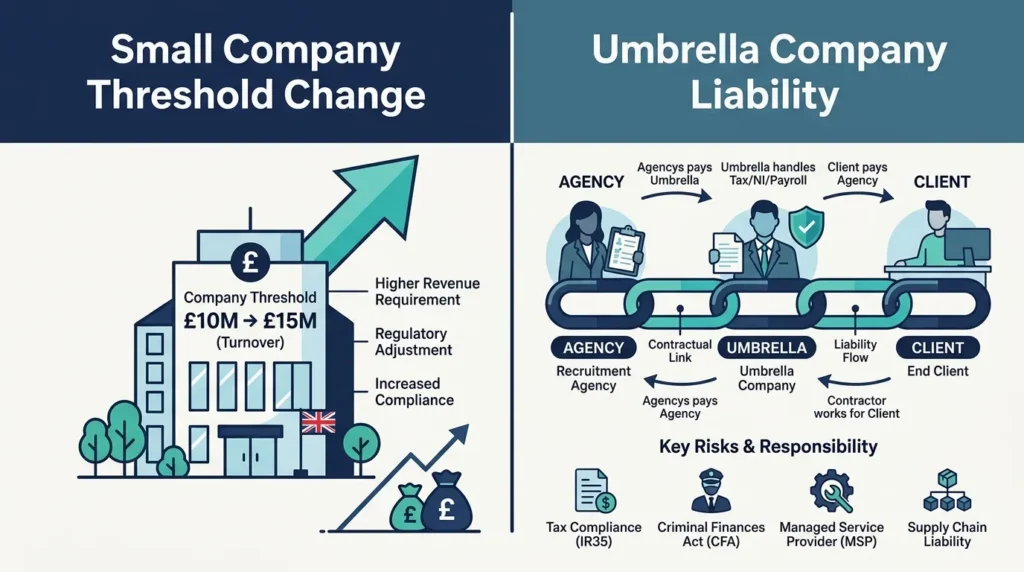

The Small Company Threshold Increase

From 6 April 2025, the Companies Act thresholds that define a “small” company rose: turnover from £10.2 million to £15 million, and balance sheet total from £5.1 million to £7.5 million. The employee threshold stayed at 50.

Here’s the part that trips people up: company size for IR35 purposes is judged against the previous financial year’s accounts. So most businesses won’t see the practical effect until the 2027/28 tax year.

HMRC estimates around 14,000 businesses will move from medium to small as a result, shifting status determination back to the contractor’s own PSC. If your end client currently issues your SDS, ask now whether they expect to reclassify.

Joint and Several Liability for Umbrella Companies

From 6 April 2026, a new rule under Chapter 11 of ITEPA 2003 makes recruitment agencies — and end clients, where there’s no agency involved — jointly and severally liable for PAYE and National Insurance if the umbrella company paying a worker fails to account for it correctly.

This doesn’t change how IR35 status itself is assessed. It’s separate legislation aimed at tax loss in the umbrella market. But because so many inside-IR35 contractors get paid through umbrella companies, the practical overlap is significant. If you’re paid via PAYE through any structure, it helps to understand how employer National Insurance factors into what gets deducted from your pay.

FAQs

Does Brexit affect IR35?

No. IR35 is domestic UK tax law, unconnected to EU membership.

Who decides if I’m inside or outside IR35?

Your own limited company decides if your client is small. Your client decides, via a Status Determination Statement, if they’re medium or large.

Can I challenge an inside IR35 determination?

Yes. Clients must provide an appeals process and respond within 45 days.

Does IR35 apply to sole traders?

No. IR35 only applies where an intermediary — typically a personal service company — sits between you and the client.

What happens if HMRC investigates my IR35 status?

HMRC reviews your contract and your actual working practices, focusing on control, substitution, and mutuality of obligation. If they conclude the engagement was inside IR35, backdated tax, interest, and a behaviour-based penalty can follow.

Key Takeaways

IR35 decides whether contractors pay tax as employees or as businesses, based on how an engagement actually works rather than what the contract claims. Status hinges on three tests — control, substitution, and mutuality of obligation — and who makes the determination depends entirely on your client’s size. Two 2026 changes are reshaping this landscape: rising company size thresholds will eventually shift responsibility back to more contractors’ own companies, and new liability rules are pushing agencies and clients to scrutinise umbrella companies more closely. Whichever side of the line you sit on, the safest position is the same one it’s always been — make sure your contract and your day-to-day working practices actually match.

{kind=link}