If you’re self-employed in the UK, National Insurance in 2026 works differently to how it works for employees — and the rules have changed enough in the last two years that a lot of people are still working from outdated information.

The short version: mandatory Class 2 NI was abolished in April 2024. You now pay Class 4 NI on your profits — at 6% between £12,570 and £50,270, and 2% above that. But there’s more to it. Whether voluntary Class 2 is worth paying, how your NI record protects your State Pension, and what Making Tax Digital changes from April 2026 — all of that affects your real position.

This guide covers the 2026/27 tax year: 6 April 2026 to 5 April 2027.

How National Insurance Works Differently for Self-Employed People

Employees have NI deducted automatically through PAYE every pay period. You don’t. As a sole trader or freelancer, you calculate and pay your National Insurance through your annual Self Assessment tax return.

There’s another key difference. Employees pay NI on gross earnings. You pay NI on your profits — income minus allowable business expenses. If you earned £40,000 but spent £8,000 on legitimate costs, your NI is calculated on £32,000, not £40,000. That distinction matters a lot, especially if you’re just starting out as self-employed in the UK and still building your expense base.

Class 2 National Insurance in 2026: What the Abolition Actually Means

From 6 April 2024, mandatory Class 2 National Insurance was abolished. You no longer pay a flat weekly amount regardless of your profits.

But abolished doesn’t mean gone. HMRC replaced mandatory payments with an automatic credit system.

Here’s exactly how it works for 2026/27:

- Profits above £7,105 (the Small Profits Threshold): You receive an automatic NI credit. No payment needed. You still build a qualifying year toward your State Pension.

- Profits below £7,105: No automatic credit. You don’t pay Class 2 and you don’t get a qualifying year — unless you choose to pay voluntarily.

The £7,105 threshold matters most if your profits are low or variable. A gap in your NI record reduces your eventual State Pension, sometimes permanently if left too long.

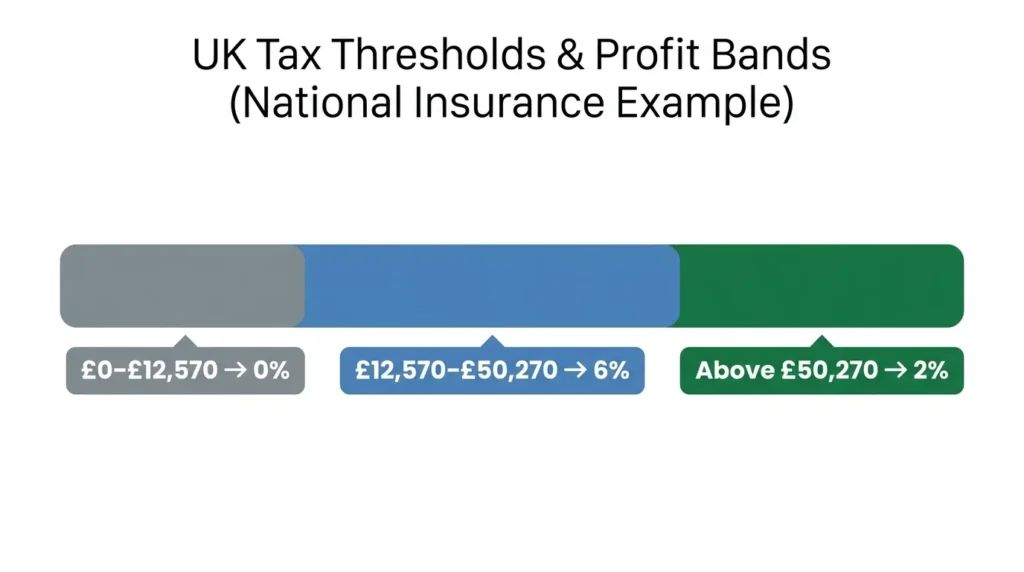

Class 4 National Insurance Rates for 2026/27

Class 4 is your main NI charge as a self-employed person. It’s a percentage of your annual trading profits.

2026/27 Class 4 rates and thresholds:

| Profit Level | Rate |

|---|---|

| Up to £12,570 (Lower Profits Limit) | 0% |

| £12,570 to £50,270 (Upper Profits Limit) | 6% |

| Above £50,270 | 2% |

Both thresholds are frozen until April 2028. The Lower Profits Limit of £12,570 matches the income tax Personal Allowance — so if your profits sit below that figure, you owe nothing in either Class 4 NI or income tax.

Class 4 is paid through Self Assessment alongside your income tax. There’s no separate payment route.

Worked Example: Calculating Your Class 4 Bill

Say you’re a freelance photographer with profits of £32,000 in 2026/27.

- Profits up to £12,570 → £0 NI

- Profits from £12,570 to £32,000 = £19,430 taxable band

- £19,430 × 6% = £1,165.80 in Class 4 NI

That’s your entire Class 4 liability for the year. Paid as part of your January 2027 Self Assessment bill.

For higher earners — say profits of £60,000:

- £12,570 to £50,270 = £37,700 × 6% = £2,262.00

- £50,270 to £60,000 = £9,730 × 2% = £194.60

- Total Class 4 NI: £2,456.60

Voluntary Class 2 Contributions: Is It Worth Paying?

If your profits fall below £7,105, you won’t automatically earn a State Pension qualifying year. Voluntary Class 2 lets you buy that year for £3.65 per week — £189.80 for a full year in 2026/27.

Compare that to Class 3 voluntary contributions, which are available to people who are neither employed nor self-employed. Class 3 costs £18.40 per week — £956.80 per year.

Same result. A £767 difference.

Is it worth it? The full new State Pension for 2026/27 is £241.30 per week. Each qualifying year adds roughly £358 annually to your eventual pension. You’d recover the £189.80 cost of a voluntary Class 2 payment in well under a year of retirement. For most people with low-profit years, it’s worth paying.

There’s a second reason if you’re planning a family. Voluntary Class 2 protects eligibility for Maternity Allowance, the primary maternity benefit for self-employed women. Entitlement depends on your NI record across the 66-week test period before your due date.

One change from April 2026: You can no longer pay voluntary Class 2 for periods spent working abroad. Only Class 3 voluntary contributions are available for overseas time from this tax year onward.

National Insurance and Your State Pension: What Counts and What Doesn’t

This catches a lot of self-employed people off guard.

Class 4 NI does not build State Pension entitlement. It funds public services as a profit-based tax. It does not add qualifying years to your NI record.

Qualifying years come only from Class 2 — automatically if your profits exceed £7,105, or through voluntary payments if they don’t.

You need 35 qualifying years for the full State Pension (£241.30/week in 2026/27). A minimum of 10 qualifying years earns you any State Pension at all. Below 10 years, you get nothing.

Check your NI record through your Government Gateway account on GOV.UK. It shows your total qualifying years, any gaps, and how many more you need.

You can normally fill gaps by paying voluntary contributions going back up to six tax years. Note: the one-off extension that allowed payments back to 2006 ended on 5 April 2025. That window is closed.

Accurate profit tracking is the foundation of all of this. Solid small business accounting practices directly affect both your Class 4 NI bill and whether you automatically earn State Pension credits each year.

How and When to Pay NI as a Sole Trader

Class 4 NI is collected through your Self Assessment return. The key 2026/27 deadlines:

- 31 January 2027 — balancing payment for 2026/27, plus first Payment on Account for 2027/28

- 31 July 2027 — second Payment on Account for 2027/28

Payments on Account explained

If your combined tax and NI bill exceeds £1,000, HMRC requires advance payments toward next year’s bill. Each payment is 50% of your previous year’s total. It surprises a lot of first-year sole traders.

Example: your 2026/27 tax and Class 4 bill comes to £3,000. In January 2027, you owe £3,000 (the balancing payment) plus £1,500 (first payment on account) — £4,500 in a single month. Knowing this in advance is the only protection against it. Budgeting for your annual tax bill across the year, rather than saving in a panic, makes a real difference.

If you can’t pay on time, HMRC’s Time to Pay arrangement lets you set up an instalment plan. Contact them before the deadline — not after it passes.

Making Tax Digital from April 2026: What Self-Employed People Need to Know

Making Tax Digital (MTD) for Income Tax is the biggest administrative shift for sole traders in years. From 6 April 2026, it becomes mandatory for the first group of affected taxpayers.

Who is affected from April 2026? Sole traders and landlords with combined gross income (turnover, not profit) above £50,000. Even if your taxable profit is much lower, MTD uses gross income before expenses to determine who qualifies.

Under MTD, you replace the single annual Self Assessment return with:

- Digital bookkeeping throughout the year using HMRC-compatible software

- Quarterly digital updates to HMRC (four times per year)

- A final year-end declaration — a fifth submission that closes the year

This doesn’t change your NI rates or thresholds. Class 4 is calculated exactly the same way. What changes is the timing and format of how you report. Using finance apps built for UK sole traders that are MTD-compatible from day one cuts the quarterly burden significantly.

April 2027 expansion: The threshold drops to £30,000 gross income, pulling in a much larger pool of sole traders and landlords.

If you’re not already using cloud accounting software, start now. Leaving it until your first quarterly deadline arrives is not a workable plan.

Self-Employed NI vs Employee NI: Key Differences

| Employee | Self-Employed | |

|---|---|---|

| NI class paid | Class 1 | Class 4 (+ Class 2 credits) |

| Main band rate | 8% | 6% |

| Upper rate (above £50,270) | 2% | 2% |

| Employer also contributes | Yes (15% above £5,000) | No |

| Payment method | Automatic via PAYE | Self Assessment |

| Builds State Pension | Yes (Class 1) | Class 2 credits only |

The 2% lower rate in the main band is a genuine saving. But employees also benefit from employer pension contributions, statutory sick pay, and employer-funded NI credits. As a sole trader, none of that exists.

If you’re weighing up whether to remain a sole trader or move to a limited company structure, the NI treatment of salary vs dividends changes the calculation significantly. A full comparison of sole trader vs limited company covers the tax and NI implications of each structure in detail.

Frequently Asked Questions

Do self-employed people still pay Class 2 NI in 2026? Mandatory Class 2 was abolished in April 2024. If your profits exceed £7,105, you automatically receive NI credits at no cost. Below that, you can pay £3.65 per week voluntarily to protect your State Pension record.

Does Class 4 NI count toward my State Pension? No. Class 4 is a profit-based tax that funds public services. It does not build qualifying years. Only Class 2 contributions — automatic credits above £7,105, or voluntary payments below — count toward your State Pension.

What is the self-employed NI rate for 2026/27? 6% on profits between £12,570 and £50,270. 2% on profits above £50,270. No NI is charged on profits below £12,570.

When do I pay my NI bill? Through Self Assessment. The main deadline is 31 January 2027 for the 2026/27 tax year. Payments on Account may also be due on 31 July 2027. Proper self-employed tax planning throughout the year prevents the January bill from being a shock.

What if I’m both employed and self-employed? You pay Class 1 NI through PAYE on your employment income and Class 4 NI on your self-employed profits. If you’ve already paid the maximum Class 1 in the year (earnings above the Upper Earnings Limit), Class 4 NI on your profits above £50,270 is limited to 2%. The two are calculated separately in your Self Assessment return.

Does MTD change how I pay NI? No. Making Tax Digital changes how and when you report income — not the NI rates or payment amounts. Class 4 NI is still calculated on your annual profits and collected through Self Assessment.

What to Take Away

For the 2026/27 tax year, self-employed National Insurance is simpler than it was before 2024 — but it still has real gaps that catch people out.

Class 4 is your main charge: 6% on profits between £12,570 and £50,270, and 2% above that. Class 2 is no longer mandatory, but if your profits fall below £7,105, you need to pay voluntarily at £3.65 a week to protect your State Pension record. It costs £189.80 a year. It’s worth it.

If your gross income exceeds £50,000, Making Tax Digital is live from April 2026. Get compliant software in place before the first quarterly deadline — not after.

And if you’re still getting to grips with what’s required of you as a self-employed person more broadly, understanding your legal and tax obligations as a UK small business owner gives you a solid foundation to build on.

Rates and thresholds in this article are based on confirmed HMRC figures for the 2026/27 tax year. This is general information, not personal tax advice. For advice specific to your situation, speak with a qualified accountant.

: HMRC Steps, NI Rates & Deadlines")

: Step-by-Step Guide")

{kind=link}