Most company directors assume they know their corporation tax rate. A surprising number are wrong.

The UK introduced a two-tier system in April 2023. It’s still in place for 2025/26 — confirmed unchanged by the Autumn Budget 2024 and the Spring Statement 2025. Two headline rates apply: 19% for smaller profits and 25% for larger ones. Between them, there’s a band where the effective rate on each additional pound of profit quietly hits 26.5%.

This guide covers every rate and threshold that applies for financial year 2025 (1 April 2025 to 31 March 2026). By the end, you’ll know your exact rate, how marginal relief works, and what reduces your bill.

What Is the UK Corporation Tax Rate for 2025/26?

The UK corporation tax rate for 2025/26 is 19% on taxable profits up to £50,000 and 25% on profits above £250,000. Profits between those two figures attract marginal relief, producing a gradually increasing effective rate.

| Taxable Profits | Rate Applied | Effective Rate |

|---|---|---|

| Up to £50,000 | Small profits rate | 19% |

| £50,001 – £250,000 | Main rate with marginal relief | 19% – 26.5% |

| Over £250,000 | Main rate | 25% |

These rates apply to all UK-resident limited companies and to overseas companies trading in the UK through a permanent establishment.

What Changed — and What Didn’t — for 2025/26

Nothing changed. Rates for 2025/26 are identical to those in 2023/24 and 2024/25.

The Autumn Budget 2024 formally confirmed the freeze. The Spring Statement 2025 made no further adjustments. The two-rate structure remains in place, and there is no published government plan to alter it before the next fiscal review.

Before April 2023, every UK company paid a flat 19% on all profits regardless of size. That changed when the Finance Act 2021 reintroduced a tiered system. A company with £500,000 in taxable profit that paid £95,000 in corporation tax under the old regime now pays £125,000 — an extra £30,000 every year.

The Small Profits Rate: 19%

Companies with augmented profits of £50,000 or less pay an effective corporation tax rate of 19%. According to HMRC data, approximately 70% of active UK limited companies fall into this category.

Technically, every company is initially charged at 25%. Those with profits at or below the lower limit then claim marginal relief to reduce their bill to the 19% effective rate. Your accounting software handles this automatically.

Augmented profits explained. HMRC uses augmented profits — not just taxable profits — to determine which band applies. Augmented profits equal taxable profits plus exempt distributions received from non-group companies. For most small companies with no dividend income from external investments, augmented profits and taxable profits are the same number.

If you’re still deciding whether to trade as a limited company at all, our comparison of sole trader and limited company tax treatment in the UK sets out how corporation tax fits into the broader picture.

The Main Rate: 25%

Any company with augmented profits above £250,000 pays 25% on all taxable profits. There’s no taper above this threshold — it’s a flat rate on the full amount.

| Taxable Profit | CT at 25% | Old Rate (19%) | Extra Tax |

|---|---|---|---|

| £300,000 | £75,000 | £57,000 | £18,000 |

| £500,000 | £125,000 | £95,000 | £30,000 |

| £1,000,000 | £250,000 | £190,000 | £60,000 |

Companies close to the £250,000 threshold may want to model the impact of accelerating allowable expenditure before year-end to keep profits below the upper limit.

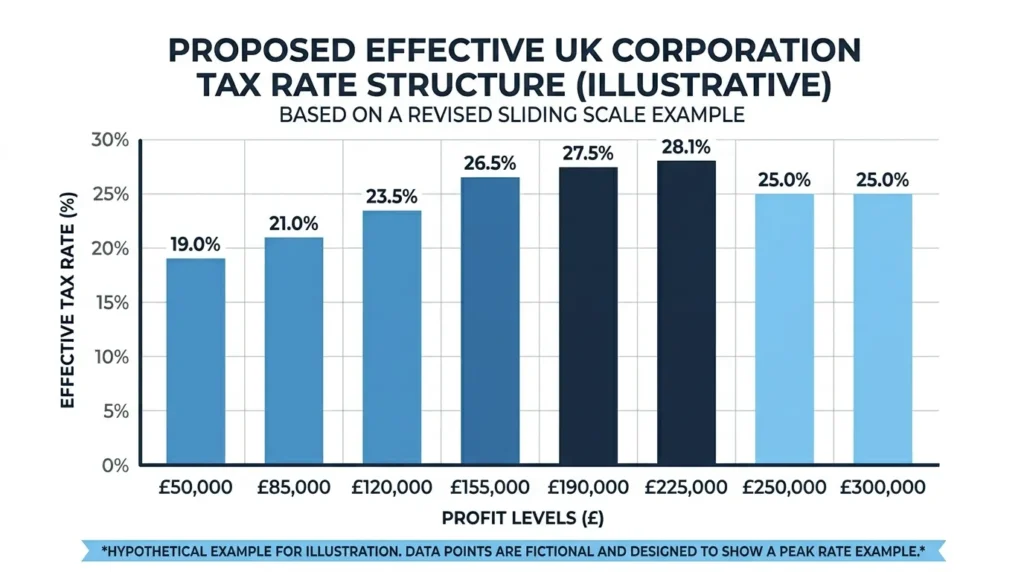

Marginal Relief: The Band Between £50,000 and £250,000

This is the part most guides underexplain.

Companies with profits between £50,000 and £250,000 pay the 25% main rate, then deduct marginal relief. The relief is withdrawn as profits increase, which creates an effective rate that climbs from 19% toward 25%.

Here’s the catch: the effective tax rate on each additional pound of profit inside this band is 26.5% — higher than the main rate itself. As marginal relief is withdrawn, every extra £1 of profit in this range costs 26.5p in corporation tax. Earning more money inside this band costs more per pound than earning it above £250,000.

The Marginal Relief Formula

Marginal Relief = 3/200 × (£250,000 − Augmented Profits) × (Taxable Profits ÷ Augmented Profits)

For most standalone companies with no exempt distributions, this simplifies to:

Marginal Relief = 0.015 × (£250,000 − Taxable Profits)

Effective Rates at Key Profit Levels

| Taxable Profit | CT at 25% | Marginal Relief | CT Payable | Effective Rate |

|---|---|---|---|---|

| £50,000 | £12,500 | £3,000 | £9,500 | 19.00% |

| £75,000 | £18,750 | £2,625 | £16,125 | 21.50% |

| £100,000 | £25,000 | £2,250 | £22,750 | 22.75% |

| £150,000 | £37,500 | £1,500 | £36,000 | 24.00% |

| £200,000 | £50,000 | £750 | £49,250 | 24.63% |

| £250,000 | £62,500 | £0 | £62,500 | 25.00% |

| £500,000 | £125,000 | £0 | £125,000 | 25.00% |

Associated Companies: How They Affect Your Thresholds

If you control more than one UK company — or two companies share the same controlling ownership — they are associated for corporation tax purposes. The £50,000 and £250,000 thresholds are divided equally between all associated companies.

| Number of Associated Companies | Lower Limit per Company | Upper Limit per Company |

|---|---|---|

| 1 (standalone) | £50,000 | £250,000 |

| 2 | £25,000 | £125,000 |

| 3 | £16,667 | £83,333 |

| 4 | £12,500 | £62,500 |

A company with £80,000 in taxable profits and no associated companies pays 19% — its profits fall below the lower limit. Add one associated company, and the lower threshold halves to £25,000. That £80,000 now sits deep inside the marginal relief band, and the effective rate rises to around 23%.

What Counts as an Associated Company?

Two companies are associated if one controls the other, or if the same person (or group of connected persons) controls both. Connected persons include spouses and civil partners. Dormant companies with no income and no significant assets or transactions are excluded from the count.

If you’re setting up a second company, or haven’t yet launched your first, our step-by-step guide to starting a limited company in the UK covers how company structure affects your tax position from day one.

Short Accounting Periods

If your company’s accounting period is shorter than 12 months, both thresholds are reduced proportionally.

A company with a six-month accounting period has a lower limit of £25,000 and an upper limit of £125,000. A three-month accounting period cuts both thresholds to one quarter of their standard values. This most commonly affects newly incorporated companies or those that have changed their year-end date.

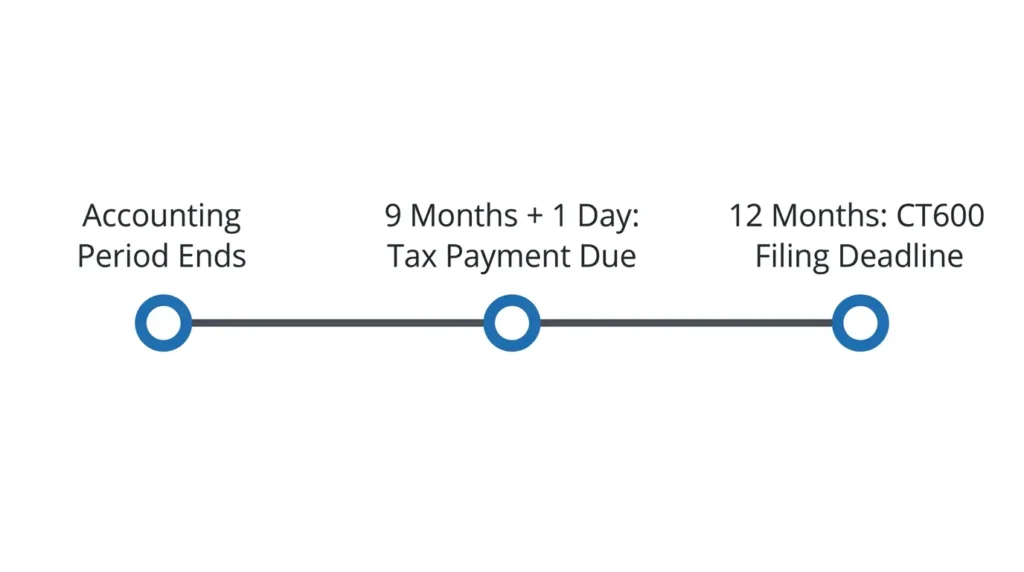

When to Pay Corporation Tax

Small companies (profits under £1.5 million): Payment is due 9 months and 1 day after the accounting period ends. A company with a 31 March 2026 year-end must pay by 1 January 2027.

Large companies (profits over £1.5 million): Pay via quarterly instalment payments (QIPs), starting 6 months and 13 days into the accounting period. This applies to companies that were large in the prior year.

HMRC charges interest on late payments at the Bank of England base rate plus 2.5%. This accrues from the day the payment was due.

Filing the CT600 Return

The CT600 corporation tax return must be filed with HMRC within 12 months of the accounting period end. Payment and filing are on separate schedules — for most small companies, you pay three months before you file.

Penalties for late CT600 filing:

- 1 day late: £100 automatic penalty

- 3 months late: A further £100

- 6 months late: HMRC estimates your liability and adds 10% of the unpaid tax

- 12 months late: A further 10% of unpaid tax

Interest on unpaid tax runs alongside penalties from the payment due date. For a broader look at how HMRC applies penalty escalation across taxes, our article on HMRC late filing and payment penalties explains the process in detail.

How to Reduce Your Corporation Tax Bill

Capital Allowances and the Annual Investment Allowance

You can deduct the full cost of qualifying plant and machinery in the year you buy it via the Annual Investment Allowance (AIA). The AIA limit is £1 million per year. This covers equipment, tools, commercial vehicles, and most fixtures.

R&D Tax Credits

SMEs can claim an enhanced deduction of 86% on qualifying research and development expenditure, reducing taxable profit. Loss-making SMEs can claim a cash credit of 10% of qualifying R&D spend from HMRC. The R&D Expenditure Credit (RDEC) for large companies is 20%.

Trading Loss Relief

Trading losses can be carried back one year to offset prior profits, generating a repayment. They can also be carried forward indefinitely against future profits from the same trade.

Salary and Dividend Planning

For companies in the marginal relief band, year-end profit planning matters. The optimal director salary for 2025/26 is typically £12,570 — it uses the personal allowance fully while triggering minimal National Insurance.

Salary is a tax-deductible business expense, which reduces taxable profit. But paying more salary brings employer National Insurance contributions at 13.8% on earnings above £5,000. Whether increasing salary to reduce profits is worthwhile depends on your specific position in the marginal band — it needs modelling, not guessing.

Corporation Tax Rate History

| Financial Year | Corporation Tax Rate |

|---|---|

| 2017/18 – 2022/23 | 19% (flat rate, all profits) |

| 2023/24 – 2025/26 | 19% (profits ≤ £50,000) / 25% (profits > £250,000) |

The current regime traces back to the Finance Act 2021, which legislated the rate increase and reintroduced the tiered structure from April 2023. Between 2010 and 2017, the main rate was progressively reduced from 28% to 19%. The 2023 change was the first upward rate movement in over a decade.

Frequently Asked Questions

Does corporation tax apply to sole traders? No. Sole traders pay Income Tax and National Insurance on their profits. Corporation tax applies only to UK limited companies and some other corporate entities such as overseas companies with a UK permanent establishment.

What is the UK corporation tax rate for 2025/26? 19% on taxable profits up to £50,000. 25% on profits above £250,000. Marginal relief applies between those figures, with an effective marginal rate of 26.5% on each extra pound earned inside the band.

Did the corporation tax rate change for 2025/26? No. Rates are unchanged from 2023/24 and 2024/25. The Autumn Budget 2024 confirmed no changes for the current year.

What is the 26.5% effective rate? It’s the tax cost per additional pound of profit inside the £50,000–£250,000 marginal relief band. As profits rise, marginal relief is withdrawn at a rate equivalent to 26.5p per pound. This means profits in this range cost more per pound than profits above £250,000.

When does corporation tax have to be paid? For most companies, 9 months and 1 day after the accounting period ends. Large companies with profits above £1.5 million pay via quarterly instalments during the accounting period.

What happens if I miss the payment deadline? HMRC charges interest from the due date. The late filing penalty for the CT600 is separate — starting at £100 for one day late and escalating from there.

{kind=link}