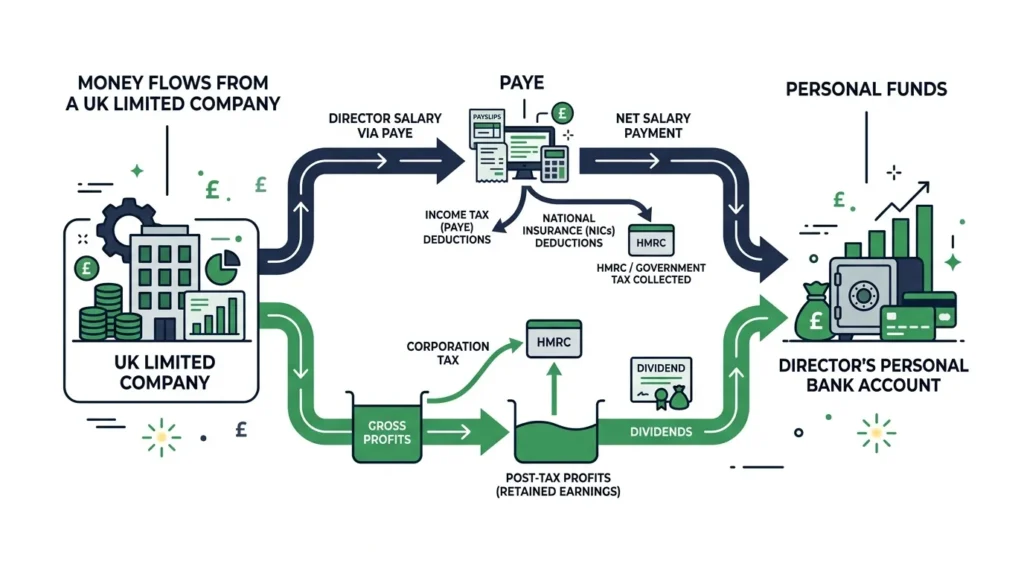

As a limited company director in the UK, you can pay yourself in four ways: a director’s salary through PAYE, dividends from profits, a director’s loan, or reimbursement of business expenses. Most directors use a mix of salary and dividends. Done correctly, this approach is the most tax-efficient option available — and for many directors it saves several thousand pounds per year compared to taking a straight salary. This guide covers how each method works, the 2026/27 thresholds you need, and the steps you must follow to stay on the right side of HMRC.

The Four Ways Directors Can Pay Themselves

Understanding what a limited company is and how it operates as a separate legal entity is the starting point. Because the company is distinct from you personally, there are specific rules around how you extract money from it.

Director’s salary is processed through PAYE, the same system used for all UK employees. Income Tax and National Insurance are deducted at source and sent directly to HMRC. It’s the most familiar method, but taking a large salary can be expensive in tax and National Insurance.

Dividends are payments from the company’s post-tax profits. They’re taxed at lower rates than salary and carry no National Insurance. There’s one hard rule: you can only pay dividends when the company has distributable profits. Paying them without sufficient retained profit is an illegal dividend — one that must be repaid.

A director’s loan allows you to borrow company money for personal use. It’s not income, so there’s no immediate tax charge. But strict repayment rules apply, and missing a deadline triggers a significant tax penalty.

Expenses and benefits cover legitimate business costs. Claiming these through the company avoids you funding business spending from already-taxed personal income and reduces the company’s taxable profit.

Tax on a Director’s Salary

Salary is taxed through PAYE in the same way as any employee’s wages. For 2026/27, the Personal Allowance is £12,570 — the first £12,570 of salary is tax-free.

Above that, Income Tax applies at:

- 20% on earnings from £12,571 to £50,270

- 40% on earnings from £50,271 to £125,140

- 45% on anything above £125,140

National Insurance adds another layer. Employee Class 1 NI applies once your salary exceeds £12,570. Your company pays employer Class 1 NI at 15% on any salary above the Secondary Threshold — which dropped to £5,000 per year from April 2025.

How employer National Insurance is calculated matters here more than ever. The reduction in the Secondary Threshold from £9,100 to £5,000 significantly increased the employer NI cost of paying a director. On a salary of £12,570, the company now pays approximately £1,135 in employer NI on the £7,570 above the threshold.

Tax on Dividends

Dividends come from profits that have already been subject to Corporation Tax — either at 19% (for profits under £50,000) or 25% (for profits over £250,000). What’s left after Corporation Tax can be distributed to shareholders.

For 2026/27, the Dividend Allowance is £500. The first £500 of dividend income is tax-free. Above that, dividend tax rates are:

- 8.75% for basic rate taxpayers

- 33.75% for higher rate taxpayers

- 39.35% for additional rate taxpayers

These rates are notably lower than the equivalent income tax rates on salary. No National Insurance applies to dividends either, which makes them far more efficient as a top-up to a low salary.

The Most Tax-Efficient Strategy: Salary + Dividends Combined

Most limited company directors pay themselves a low salary and draw the rest as dividends. The salary keeps your National Insurance record intact and reduces the company’s Corporation Tax bill. The dividends top up your income at a lower tax rate, with no NI.

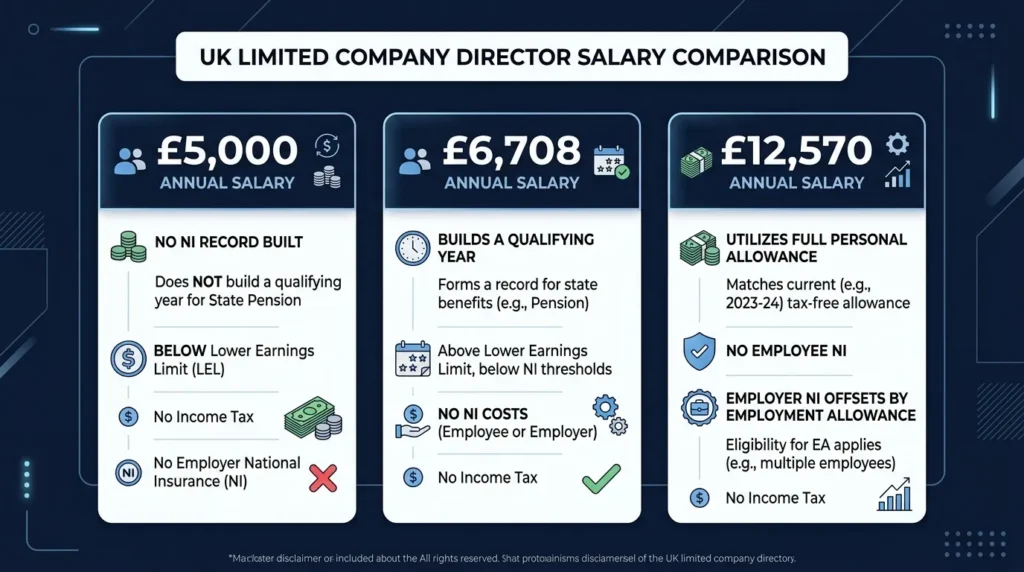

For 2026/27, three salary levels are most commonly used. Each one aligns with a specific NI threshold.

£5,000 keeps you below the employer Secondary Threshold. No employer NI, no employee NI, no Income Tax. The downside: this salary is below the Lower Earnings Limit, so it doesn’t build an NI qualifying year and doesn’t count towards your State Pension.

£6,708 (the Lower Earnings Limit for 2026/27) earns you a qualifying year on your NI record without you or the company actually paying any NI contributions. You’re above the LEL so the year counts, but below the Secondary Threshold so the company owes nothing. This is the cleanest option for sole directors where Employment Allowance isn’t available.

£12,570 uses your full Personal Allowance. No Income Tax, no employee NI — your salary sits exactly at the Primary Threshold. The company does pay employer NI of approximately £1,135 (15% of the £7,570 between the £5,000 Secondary Threshold and £12,570). If your company qualifies for Employment Allowance — available when you have at least two directors, or one director and at least one other employee — that £1,135 is fully offset. At that point, £12,570 becomes the most efficient choice by some margin.

Worked Example: £50,000 Total Income (2026/27)

You take a salary of £12,570. Your company qualifies for Employment Allowance, so the £1,135 employer NI is covered. No Income Tax and no employee NI on the salary. Your company then pays you £37,430 as dividends. The first £500 is tax-free. The remaining £36,930 is taxed at 8.75% (basic rate) — a dividend tax bill of approximately £3,231. Your total take-home is roughly £46,769 out of £50,000. A straightforward salary of £50,000 would cost considerably more in combined Income Tax and NI contributions.

Company Pension Contributions — The Strategy Most Directors Miss

If your salary is low and most of your income is in dividends, your personal pension tax relief is restricted. Dividends don’t count as relevant UK earnings, so the amount you can contribute personally and claim tax relief on is capped at your salary level.

The more effective route is contributing directly from the company. Company pension contributions are a legitimate business expense. They reduce your Corporation Tax bill, carry no National Insurance charge, and aren’t subject to the relevant UK earnings restriction. For 2026/27, the annual pension allowance is £60,000 — a company contribution can use this in full regardless of your salary level.

For a profitable limited company, this is one of the most powerful tax-planning tools available. The money leaves a taxed environment and enters a tax-free one, compounding over time. Talk to a financial adviser before setting contribution levels for your situation.

Director’s Loan Rules You Must Know

You can borrow money from your company through a director’s loan account (DLA). If the loan is repaid within 9 months and 1 day of the company’s accounting year end, no tax applies.

Miss that window and the company faces the Section 455 charge — currently 33.75% of the outstanding loan balance. HMRC applies this charge to the amount that hasn’t been repaid. The money is recoverable once the loan is repaid, but it creates a cash flow problem in the meantime and adds complexity to your accounts.

Keep loans below £10,000 to avoid a benefit-in-kind charge. Above that threshold, HMRC treats the loan as a taxable benefit unless you’re paying interest to the company at HMRC’s official rate.

One more thing: don’t cycle the same loan repeatedly — repaying it just before the deadline and immediately re-drawing the same amount. HMRC treats this as disguised salary and will tax it accordingly.

How to Legally Pay Yourself Dividends

Paying dividends isn’t just a bank transfer. There is a legal procedure you must follow each time.

The directors must hold a board meeting — even if you are the sole director — and formally declare the dividend. You record the decision in board minutes. You then issue a dividend voucher to each shareholder receiving payment. The voucher must state the date, amount per share, and company details.

Only pay dividends from distributable profits — the retained profit remaining after Corporation Tax. Paying more than the available profit creates an illegal dividend, which must be repaid to the company.

All dividend income above the £500 allowance must be declared on a Self Assessment tax return. If you haven’t registered for Self Assessment yet, you must do so by 5 October following the end of the tax year in which you first received dividends. HMRC will then issue you a Unique Taxpayer Reference (UTR) and set up your filing obligations.

Common Mistakes Limited Company Directors Make

Paying dividends from a loss-making company. No distributable profits means no legal dividends. If you make the payment anyway, it becomes an illegal dividend and must be repaid to the company.

Not registering for Self Assessment. PAYE doesn’t cover dividends. Many new directors assume it does. It doesn’t. Dividend income and any other untaxed income must be reported. Late Self Assessment filing carries penalties that start at £100 and escalate sharply the longer the return is outstanding.

Letting a director’s loan run overdrawn past the deadline. The S455 charge is 33.75%. Directors sometimes lose track of the 9-month repayment window when a year end passes.

Ignoring the State Pension. Dividends build no NI record. Over a full working career, taking zero salary means significant gaps in State Pension entitlement. A salary of at least £6,708 builds a qualifying year at no NI cost to you or the company.

Not keeping dividend paperwork. Board minutes and dividend vouchers are legal requirements under company law. If HMRC investigates, these documents are what you produce to prove the payments were legitimate.

Frequently Asked Questions

Do dividends count towards my State Pension? No. Only PAYE salary contributes to your NI record. Dividend income does not build any NI qualifying years and has no impact on your State Pension entitlement.

Can I pay myself a dividend every month? Yes, as long as the company has sufficient distributable profits each time. You must go through the formal process — board resolution, minutes, and a dividend voucher — every single time you declare one.

Do I need to register for PAYE as a director? Yes, if you’re paying yourself a salary. You must register with HMRC as an employer before making your first payment. If you’re taking only dividends and no salary, you don’t need to run payroll — but remember, this means no NI qualifying years and no State Pension contributions.

Should I operate as a limited company or sole trader? It depends on your profit level and circumstances. The sole trader vs limited company comparison for 2026 covers this in detail — but broadly, a limited company becomes more tax-efficient once your profits consistently exceed £30,000–£35,000 per year.

What happens if my company makes a loss? You can still pay yourself a salary if the company has the cash — but not dividends. Your salary is a business expense, so it will deepen the loss. That loss can be carried forward and offset against future profits.

Should I use an accountant? For most directors, yes. Getting the salary and dividend split right, staying on top of PAYE submissions, completing Self Assessment correctly, and maximising pension contributions all benefit from professional advice. The cost is typically a fraction of what you’d overpay in tax without it.

Tax rules change each April. Always verify the current rates and thresholds with HMRC or a qualified accountant. The information in this article is correct as of the 2026/27 tax year but does not constitute personalised financial or tax advice.

{kind=link}