You’ve spotted “1257L” or maybe something stranger like “K475” on your payslip, and you want to know two things: what does it actually mean, and is HMRC taking the right amount of money out of your pay. This guide answers both, with worked examples rather than vague definitions.

What is a UK Tax Code? (The Quick Answer)

A tax code is a short combination of numbers and letters — such as 1257L — that your employer or pension provider uses to work out how much Income Tax to deduct from your pay before you receive it. HMRC issues the code; your employer or pension provider simply applies it through the PAYE (Pay As You Earn) system. The number tells your employer how much of your income is tax-free. The letter tells them why.

Why Do You Have a Tax Code?

Every PAYE employee and most pension recipients need a tax code because the UK doesn’t tax you on everything you earn. You get a tax-free Personal Allowance first — £12,570 for the 2026/27 tax year, frozen at that level since 2021/22 and expected to stay frozen until at least April 2028. Your tax code tells your employer exactly how much of that allowance applies to this particular job or pension, and whether anything needs to be added or subtracted from it.

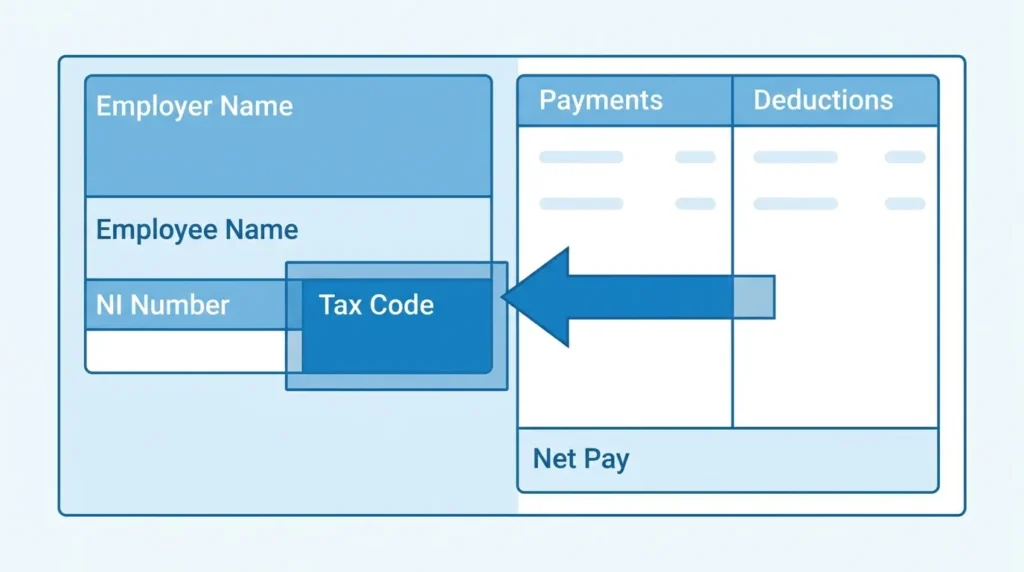

Where to Find Your Tax Code

Your tax code appears in four places:

- Your payslip — usually near your National Insurance number, labelled “Tax Code” or “T/C.”

- Your P45 — issued when you leave a job.

- Your P60 — issued by your employer at the end of each tax year (by 31 May).

- Your P2 coding notice — a letter HMRC sends whenever your code changes, with a breakdown of how they calculated it.

You can also view your current code any time by logging into your Personal Tax Account or the HMRC app.

How Does a Tax Code Work? Understanding the Math

Here’s the part most guides skip: the actual arithmetic. Your tax code number, multiplied by 10, gives you your annual tax-free allowance. So 1257 becomes £12,570. Your employer takes that figure and divides it across your pay periods — by 12 if you’re paid monthly, by 52 if weekly — giving you roughly £1,047.50 of tax-free pay each month before Income Tax kicks in on the rest.

The Standard Personal Allowance Explained

For the 2026/27 tax year, which runs from 6 April 2026 to 5 April 2027, the standard Personal Allowance is £12,570. Once that’s used up, the remaining bands for England, Wales and Northern Ireland are:

| Band | Taxable Income | Tax Rate |

|---|---|---|

| Personal Allowance | Up to £12,570 | 0% |

| Basic Rate | £12,571 to £50,270 | 20% |

| Higher Rate | £50,271 to £125,140 | 40% |

| Additional Rate | Over £125,140 | 45% |

Scotland uses its own bands under an S-prefixed code (e.g. S1257L), with more, narrower bands than the rest of the UK. Wales uses a C-prefixed code (e.g. C1257L), but currently mirrors the England and Northern Ireland rates.

How HMRC Calculates Your Code (With Examples)

HMRC starts with your standard Personal Allowance, then adjusts it up or down based on your circumstances:

- Add — Marriage Allowance received, approved job expenses (uniform, tools, professional subscriptions).

- Subtract — the taxable value of benefits in kind (company car, private medical insurance), untaxed income such as a small amount of rental income, or tax owed from a previous year.

Worked example: Say you have a company car with a taxable benefit value of £3,000. HMRC subtracts that from your £12,570 allowance, leaving £9,570. Drop the last digit, and your code becomes 957L. That’s why your code might be lower than your colleague’s even though you earn the same salary — the difference is entirely down to the benefit, not your pay.

Getting this right matters for anyone running payroll too. If you’re an employer working through this from the other side, our guide on how to run payroll for a small business in the UK covers the process end to end.

UK Tax Code Letters Explained: What Do They Mean?

The letter (or letters) attached to your tax code number tells your employer which set of rules applies. Here’s a direct breakdown.

L, M, N, and T: The Common Coding Letters

| Letter | Meaning |

|---|---|

| L | Standard Personal Allowance — the default for most single-job employees with no complications |

| M | You’ve received 10% of your partner’s Personal Allowance via Marriage Allowance (code rises, e.g. 1383M) |

| N | You’ve transferred 10% of your allowance to your partner via Marriage Allowance (code falls, e.g. 1131N) |

| T | HMRC needs to review your situation manually — often triggered by income near or above £100,000, or other complex circumstances |

BR, D0, D1, and NT: The Multiple-Income Codes

These letters are almost always applied to a second income source — a second job, or a pension running alongside employment — because HMRC assumes your main job already uses your Personal Allowance.

- BR — Basic Rate. Every pound from this income is taxed at 20%, with no tax-free allowance applied.

- D0 — Every pound taxed at the higher rate, 40%.

- D1 — Every pound taxed at the additional rate, 45%.

- NT — No Tax. Rare; used in specific situations such as certain non-UK residents or where HMRC has agreed no tax should be deducted at source.

If BR, D0 or D1 has landed on your main job by mistake rather than a second one, you’re likely being significantly overtaxed, and it’s worth contacting HMRC straight away.

K Codes: When Your Deductions Exceed Your Allowance

K codes are where most guides get vague. Here’s the plain version.

A K code appears when the things HMRC needs to deduct from your allowance — usually company benefits, state pension income, or tax owed from a previous year — are worth more than your Personal Allowance itself. Since your allowance can’t go below zero, HMRC flips the calculation: instead of giving you a tax-free amount, they add the excess on top of your taxable income.

Worked example: Suppose your company benefits are worth £15,000, but your Personal Allowance is only £12,570. That leaves an excess of £2,430 with nowhere to go except onto your taxable income. Your code becomes K243 (the £2,430 rounded and divided by 10). In practice, this means your employer adds £2,430 to your salary before working out your tax — so a £2,430 chunk of pay effectively gets taxed twice as hard, once as extra “notional” income and once through the normal bands.

HMRC does cap K code deductions so your take-home pay in any single period can’t fall by more than 50%, as protection against a code swallowing your entire wage.

What is an Emergency Tax Code? (W1, M1, and X)

An emergency tax code is a temporary code HMRC applies when it doesn’t have enough information to calculate your correct, cumulative code — most commonly when you start a new job without handing over a P45. You’ll recognise it by the suffix: W1 (Week 1), M1 (Month 1), or X.

Why Have You Been Put on an Emergency Tax Code?

Common triggers include:

- Starting a new job and not providing a P45 from your previous employer.

- Starting your first job with no prior UK employment record.

- Beginning to receive company benefits or the State Pension alongside a job, before HMRC has updated your details.

- Being self-employed and taking on PAYE work at the same time.

How to Get Off an Emergency Tax Code

An emergency code taxes each pay period in isolation — non-cumulatively — rather than looking at your earnings across the whole tax year. This is the key difference from a normal code, and it’s usually what causes overpayment, particularly for anyone who had lower earnings (or none at all) earlier in the tax year.

The fix is largely automatic once HMRC has full information:

- Give your new employer your P45 from your previous job as soon as possible.

- If you don’t have a P45, complete the “starter checklist” your new employer provides.

- HMRC will then issue a correct, cumulative tax code — usually reflected within one or two pay cycles once your employer receives it.

- Any tax you overpaid on the emergency code is typically refunded automatically through your payslip once the new code is applied. If it isn’t picked up by year-end, you can claim it back via your Personal Tax Account.

How to Check if Your Tax Code is Wrong

Direct answer: Compare the code on your latest payslip against your actual circumstances — one job, no benefits, no other income should mean 1257L. If your situation includes a company benefit, second income, or a recent job change and your code doesn’t reflect that, it’s worth checking.

Common Reasons for an Incorrect Tax Code

- A benefit in kind (company car, private medical cover, gym membership) started or stopped, but your code wasn’t updated.

- You changed jobs and an emergency code was never corrected.

- You have two jobs or pensions and both are mistakenly using a full Personal Allowance.

- Your estimated income for the year, used by HMRC to set your code, is now inaccurate.

- A Marriage Allowance claim was made, cancelled, or never processed correctly.

In our experience reviewing payslip queries, the single most common cause isn’t a missing P45 — it’s a taxable benefit that changes without HMRC being told. Because your code stays fixed until someone flags the change, you can be quietly over- or undertaxed for months without noticing.

What Happens if You Underpay or Overpay Tax?

If you’ve overpaid, HMRC will usually refund the difference automatically once your code is corrected, either through your payslip or as a lump-sum rebate. If you’ve underpaid, HMRC typically collects the shortfall by adjusting your tax code for the following year, spreading the repayment across your pay rather than demanding it in one go — though a large underpayment can still mean a direct bill.

It’s worth remembering: it is your responsibility, not your employer’s or HMRC’s, to make sure your tax code is correct. Employers apply whatever code HMRC gives them; they don’t check it for accuracy on your behalf.

How to Change or Update Your Tax Code with HMRC

Direct answer: Update or dispute your tax code through your Personal Tax Account online, via the HMRC app, or by phone. Most changes are simple and don’t require paperwork.

Step-by-Step Guide to Correcting Your Code Online

- Log in to your Personal Tax Account at gov.uk (or use the HMRC app).

- Go to the “Income Tax” section and check your current tax code and how it was calculated.

- Report the change that affects your allowance — for example, a benefit that’s started or stopped, a new job, or an income change.

- Submit the update. HMRC recalculates your code and sends the new figure directly to your employer or pension provider.

- Check your next payslip to confirm the new code has been applied.

Contacting HMRC by Phone

If your situation is more complex, or you’d rather speak to someone, call HMRC’s Income Tax helpline on 0300 200 3300. Have your National Insurance number and, if possible, your latest P60 or payslip to hand — it speeds up the call considerably.

Timeline to expect: once HMRC issues a corrected code, it typically reaches your employer in time for your next payroll run, though this depends on your employer’s payroll cut-off date. If your payroll processes a week or more before payday, a change made mid-cycle may not land until the following pay period. If you haven’t seen a change after two full pay cycles, it’s worth chasing.

If you’re a company director figuring out the most tax-efficient way to draw income in the first place, it’s worth reading alongside our guide on how to pay yourself as a limited company director in the UK.

Frequently Asked Questions About UK Tax Codes

Why is my tax code 1257L? 1257L is the standard code for anyone with one job or pension, no taxable company benefits, and no other income affecting their allowance. It gives you the full £12,570 tax-free Personal Allowance for 2026/27.

What does K mean in a tax code? A K code means the deductions from your allowance — usually company benefits or unpaid tax — are worth more than your Personal Allowance itself. Instead of a tax-free amount, the excess is added to your taxable income.

Am I paying too much tax? You may be overpaying if you’re on an emergency code (W1, M1, or X), if a company benefit has stopped but your code hasn’t been updated, or if two jobs are both applying a full Personal Allowance. Check your code against your actual circumstances using your Personal Tax Account.

How do I claim a tax refund? If you’ve overpaid, HMRC usually refunds you automatically once your code is corrected, either through payroll or as a lump sum. You can also check and claim through your Personal Tax Account if a refund hasn’t appeared after your code changes.

What is a BR tax code? BR stands for Basic Rate. It taxes all income from that source at 20%, with no tax-free allowance applied. It’s typically used for a second job or pension, since your main income is assumed to already be using your Personal Allowance.

How long does it take for a tax code change to show on my payslip? Usually one to two pay cycles after HMRC updates your record, depending on your employer’s payroll cut-off dates.

Do self-employed people have a tax code? Only if they also have PAYE income — for example, a part-time job alongside self-employment. Pure self-employment income is taxed through Self Assessment, not a tax code. If that’s your situation, our guide to sole trader tax in the UK explains how that side of things works.

Getting your tax code right is one small check that can save you real money, in either direction. If anything on your payslip doesn’t match your circumstances — a benefit that’s changed, a new job, or a code that looks off — it’s worth five minutes in your Personal Tax Account rather than waiting for a surprise at year-end.

")

{kind=link}