The HMRC approved mileage allowance for 2025/26 is 45p per mile for the first 10,000 business miles in your own car or van, then 25p per mile after that. These rates apply from 6 April 2025 to 5 April 2026.

Motorcycles get 24p per mile. Bicycles get 20p. And if you carry a fellow employee on a business journey, there is an extra 5p per mile per passenger on top.

If you use your own vehicle for work travel, these rates matter. Employers can pay them tax-free. Employees whose employer pays below the rate can claim the shortfall back. Self-employed workers deduct the total directly from their taxable profit. Get it right and it is worth hundreds — sometimes over a thousand pounds — per year.

HMRC Approved Mileage Rates 2025/26

HMRC calls these Approved Mileage Allowance Payments (AMAPs). They set the maximum amount that can be paid or claimed tax-free when you use a personally owned vehicle for business travel.

| Vehicle | First 10,000 miles | Above 10,000 miles |

|---|---|---|

| Cars and vans | 45p | 25p |

| Motorcycles | 24p | 24p |

| Bicycles | 20p | 20p |

| Passenger supplement* | +5p | +5p |

*Per fellow employee carried on a business journey. Cars only. Each additional passenger adds 5p per mile on top of the standard rate.

The 10,000-mile threshold resets on 6 April every year. Even if you hit 10,000 miles in January or February, you start again at the full 45p rate at the start of the next tax year.

One important note: these rates have not changed since April 2011. That is fourteen consecutive years frozen. Fuel, insurance, servicing costs and tyres have all risen sharply in that time. The gap between what 45p actually covers and what running a modern car genuinely costs has widened considerably.

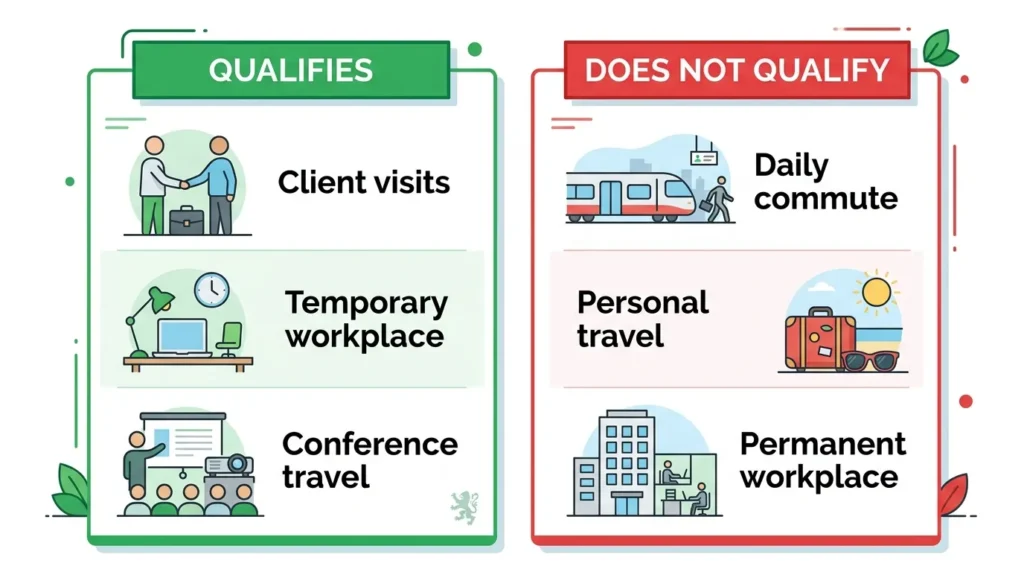

What Counts as Business Mileage?

Not every work-related drive qualifies. HMRC is specific.

Journeys that qualify:

- Travelling to a client’s premises

- Driving between two different work locations in the same day

- Attending a temporary workplace (one expected to last under 24 months)

- Going to a supplier, conference or off-site training event

- Healthcare workers travelling between patient locations

Journeys that do not qualify:

- Your regular commute from home to your permanent workplace

- Any personal errands, even if made on a working day

- Travel to a workplace you attend regularly and for an indefinite period

The 24-month rule catches people out. If you’re sent to a site that is genuinely temporary — expected to last under two years — those journeys qualify. Once it becomes clear the posting will exceed 24 months, or you know from the start it will run indefinitely, HMRC treats it as a permanent workplace and the mileage relief stops from that point.

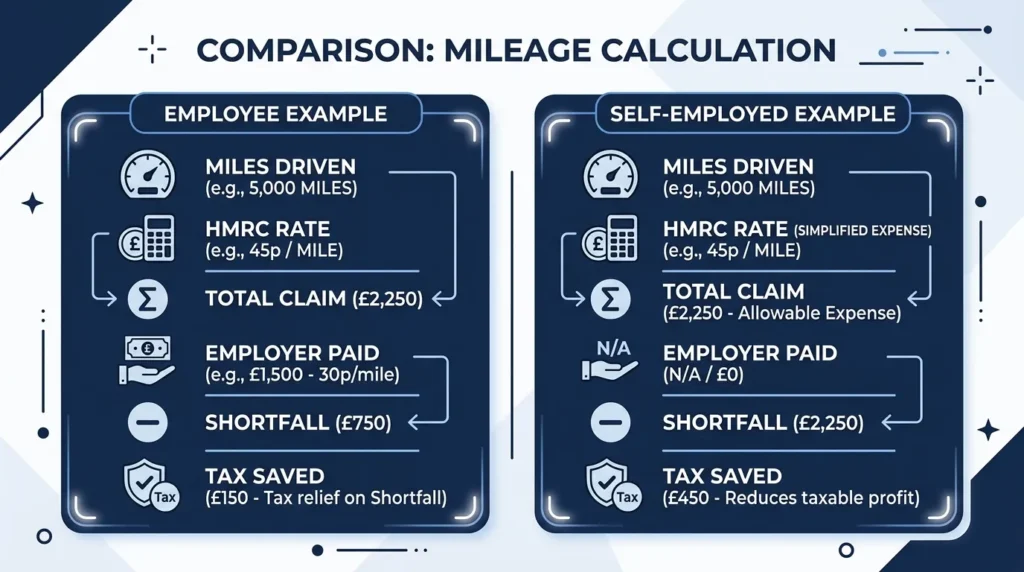

How to Claim as an Employee

If your employer already pays the full HMRC rate, there is nothing to do. The payment is tax-free up to the approved amount.

The situation is different when your employer pays below the approved rate — or nothing at all. You can claim the difference from HMRC. This is called Mileage Allowance Relief (MAR).

Here is a simple example. Say your employer pays you 25p per mile and you drove 8,000 business miles in 2025/26. HMRC’s approved rate is 45p. The shortfall is 20p per mile across 8,000 miles — that’s £1,600 of qualifying expenses. At the basic 20% tax rate, you would receive £320 back.

Using Form P87

If your total employment expenses, including mileage, are under £2,500 in the tax year and you do not already file a Self Assessment return, use Form P87. You can submit it online through your HMRC Personal Tax Account or send it by post. You’ll need your National Insurance number and your employer’s PAYE reference. HMRC will adjust your tax code or send a refund.

Using Self Assessment

If you already submit an annual return — because you’re self-employed, earn over £100,000, or have other untaxed income — include your mileage claim in the Employment pages under business travel expenses. Our full guide on how to complete your Self Assessment tax return walks through every section, including how to enter employment expenses correctly.

Backdating Your Claim

This is one of the most overlooked rules. You can claim Mileage Allowance Relief for up to four previous tax years. If you have been driving for work and never claimed — or claimed less than you were entitled to — you can still recover that tax relief now. Submit a P87 or contact HMRC directly for each year involved.

Do not let deadlines slip. Filing late on any year you’re claiming through Self Assessment opens the door to penalties. Our breakdown of HMRC Self Assessment late filing penalties covers exactly what HMRC charges and when.

How to Claim as Self-Employed

As a sole trader, business mileage is a deductible expense. It reduces your taxable profit — which means less income tax and less Class 4 National Insurance. You have two methods to choose from.

The Simplified Mileage Method

Use the same flat AMAP rates — 45p for the first 10,000 miles, 25p after that. Multiply your total business miles by the relevant rate and enter the figure as a motor expense on your Self Assessment return. No fuel receipts required. No insurance calculations. Just your mileage log.

This is the method most sole traders use. For most modern cars it works out more generously than tracking every individual cost.

The Actual Costs Method

Here you add up the genuine running cost of the vehicle — fuel, insurance, MOT, servicing, road tax, depreciation — then apply the percentage of business use. If 60% of your annual driving is for work, you deduct 60% of total running costs.

This approach suits very high-mileage drivers with expensive-to-run vehicles. It takes more record-keeping and requires receipts for everything.

The method-switching lock-in matters. Once you choose a method for a specific vehicle, you must stick with it for the entire time you own that vehicle. You cannot switch mid-ownership. If you claimed capital allowances when you purchased the vehicle, the actual costs method applies automatically — the flat rate is no longer an option for that vehicle.

If you haven’t yet registered with HMRC, our step-by-step guide on registering as a sole trader in the UK covers everything from your UTR number to your first tax return.

And if you are weighing up whether to remain a sole trader or move to a limited company, the mileage and expenses rules differ significantly between the two structures. Our sole trader vs limited company comparison for 2026 breaks down the tax treatment of vehicle expenses under each setup.

Electric Vehicles

Electric cars and vans use exactly the same AMAP rates as petrol and diesel vehicles. You can still claim 45p per mile for the first 10,000 business miles, 25p after that.

In practice, this is more favourable for EV drivers. The cost per mile to run an electric car is lower than petrol, so the 45p allowance produces a larger surplus. HMRC has made no move to create separate rates for electric personal vehicles.

This also means EV drivers have even more reason to use the simplified mileage method rather than actual costs.

What Records Does HMRC Require?

You do not need fuel receipts to claim AMAP rates. What you must have is a mileage log.

For every business journey, record:

- The date

- Start and end addresses, including postcodes

- The purpose of the journey

- The distance covered

Keep records for at least five years after the relevant Self Assessment filing deadline. HMRC can raise an enquiry well after a return is submitted, and without a log you have no defence.

Many drivers now use GPS-based mileage tracking apps. They log journeys automatically and produce HMRC-compliant reports. As Making Tax Digital expands — requiring sole traders earning over £50,000 to file quarterly from April 2026 — keeping digital expense records from now puts you ahead of the requirement. Our guide to Making Tax Digital for sole traders explains what’s changing and what software you need.

Worked Examples

Example 1 — Employee, basic rate taxpayer

James is a sales rep. He drove 11,000 business miles in 2025/26. His employer pays 30p per mile.

- HMRC-approved amount: (10,000 × 45p) + (1,000 × 25p) = £4,750

- Employer paid: 11,000 × 30p = £3,300

- Shortfall: £1,450

At 20% basic rate tax, James claims £290 as a refund via Form P87.

Example 2 — Sole trader, higher rate taxpayer

Aisha is a freelance marketing consultant. She drove 12,000 business miles in 2025/26 using the simplified mileage method.

- Claim: (10,000 × 45p) + (2,000 × 25p) = £5,000

At 40% income tax with Class 4 NIC savings on the reduced profit, her total tax saving is approximately £2,300.

What’s Changing for 2026/27?

In May 2026, HMRC confirmed the approved mileage rate for cars and vans will rise to 55p per mile for the first 10,000 business miles from 6 April 2026. It is the first increase to the AMAP rate in over 13 years, and it is linked to the September 2025 Consumer Price Index.

If any of your business journeys happened on or after 6 April 2026, use 55p — not the 45p rate this article covers.

The rates for motorcycles, bicycles and the passenger supplement are also expected to be updated for 2026/27. Always verify the current figures on GOV.UK before submitting any claim.

Key Takeaways

- 2025/26 AMAP rates: 45p per mile (first 10,000), 25p above that for cars and vans. Motorcycles: 24p. Bicycles: 20p. Passenger supplement: 5p per passenger per mile.

- Unchanged since 2011. Fourteen years without a rate increase.

- Employees can claim Mileage Allowance Relief via Form P87 (expenses under £2,500) or through Self Assessment.

- You can backdate claims for up to four previous tax years. Don’t leave money behind.

- Self-employed sole traders use the simplified 45p/25p method or actual vehicle costs — and cannot switch once a vehicle has been assigned a method.

- Electric vehicles qualify at the same AMAP rates as petrol and diesel cars.

- Keep a mileage log with date, start/end addresses, journey purpose and distance for every business trip.

- From 6 April 2026: The rate rises to 55p per mile for cars and vans under the 2026/27 rules.

{kind=link}