The UK dividend tax rates for 2026/27 are 10.75% (basic rate), 35.75% (higher rate), and 39.35% (additional rate). The dividend allowance stays at £500. Both the basic and higher rates increased by 2 percentage points on 6 April 2026.

If you run a limited company and draw dividends, or hold dividend-paying investments outside an ISA, your tax bill is higher this year than last. Many directors haven’t updated their income strategy to account for it.

This guide covers the confirmed rates, how HMRC calculates what you owe, worked examples at two income levels, and the most effective moves to reduce your liability before April 2027.

UK Dividend Tax Rates 2026/27 — The Confirmed Figures

| Tax Band | Rate | Applies to Dividends Within |

|---|---|---|

| Dividend allowance | 0% | First £500 of dividend income |

| Basic rate band | 10.75% | Total income up to £50,270 |

| Higher rate band | 35.75% | Total income £50,271 to £125,140 |

| Additional rate | 39.35% | Total income above £125,140 |

The personal allowance for 2026/27 is £12,570 — unchanged. All dividend income sits on top of your other income when HMRC applies the bands. Your salary gets there first.

The additional rate is unchanged at 39.35%. Only the basic and higher rates rose this year.

The £500 Dividend Allowance for 2026/27

Every UK taxpayer receives a £500 dividend allowance. The first £500 of dividend income you earn in 2026/27 is tax-free. It applies to dividends from every source — a limited company, a share portfolio, a unit trust, or an ETF.

One thing the allowance does not do: it doesn’t free up that £500 from the tax bands. It still occupies space in your basic rate band. So your taxable dividend income starts at £500, not £0.

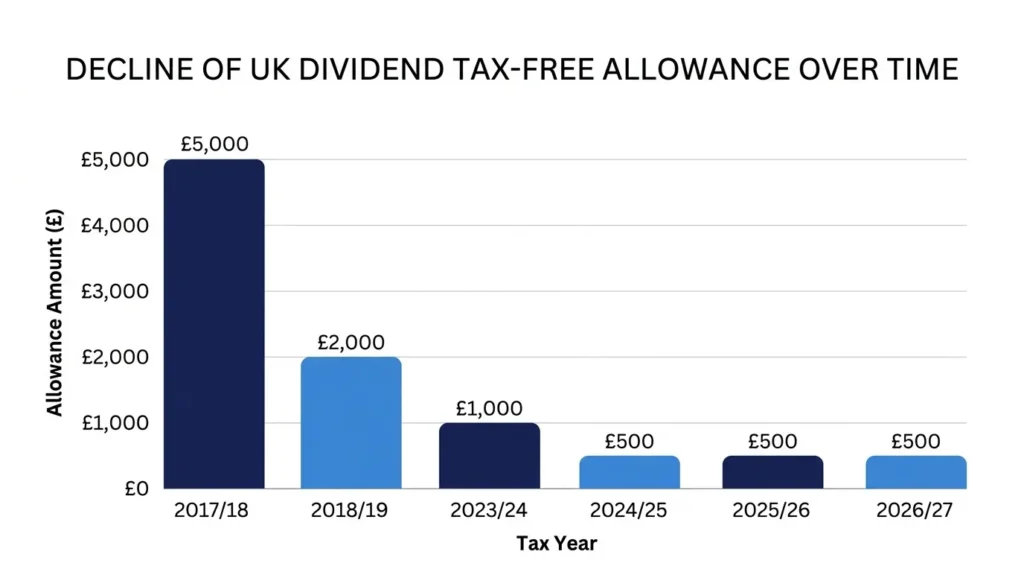

How the Allowance Has Fallen Over Time

The allowance stood at £5,000 in 2017/18. It fell to £2,000 in 2018/19, dropped to £1,000 in April 2023, and was halved to £500 in April 2024. It stays at £500 for 2026/27 with no sign of recovery. Anyone still mentally using the old £2,000 figure will underestimate their tax liability.

How Dividend Tax Is Calculated

HMRC stacks income in a fixed order. Get the sequence wrong and your tax estimate will be off.

- Total all income: salary, rental income, bank interest, and dividends.

- Subtract the personal allowance (£12,570) to get taxable income.

- Non-dividend income — salary, rental, interest — fills the tax bands first.

- Dividend income sits on top of all of that.

- Apply the £500 allowance to the first £500 of dividends. Tax the rest at the rate of the band it falls into.

The Split-Band Problem Most Directors Miss

Here’s where many directors go wrong. A £40,000 salary and £15,000 in dividends gives a total income of £55,000. Salary fills the basic rate band from £12,570 to £40,000. That leaves only £10,270 of basic rate band remaining. The other £4,730 of dividends tips into the higher rate band at 35.75%.

Directors who assume their dividends sit in the basic rate band because their total income is “around £50,000” often get a bigger tax bill than they planned for. Salary pushes dividends upward. Always calculate from your total income, not just from what you draw in dividends.

Worked Examples

Example 1: Director With Salary Covered by the Personal Allowance

- Salary: £12,570 (equals the personal allowance — zero income tax on salary)

- Dividends: £35,000

- Total income: £47,570 — entirely within the basic rate band

| Step | Amount | Rate | Tax |

|---|---|---|---|

| Dividend allowance | £500 | 0% | £0 |

| Remaining dividends | £34,500 | 10.75% | £3,708.75 |

| Total dividend tax | £3,708.75 |

At the 2025/26 rate of 8.75%, the same director paid £3,018.75. The rate rise costs this director £690 more per year — before any planning actions.

Example 2: Director With Salary Pushing Dividends Into Two Bands

- Salary: £40,000

- Dividends: £20,000

- Total income: £60,000

The salary fills the basic rate band up to £40,000. Remaining basic rate band for dividends: £50,270 − £40,000 = £10,270.

| Step | Amount | Rate | Tax |

|---|---|---|---|

| Dividend allowance | £500 | 0% | £0 |

| Basic rate portion | £9,770 | 10.75% | £1,050.33 |

| Higher rate portion | £9,730 | 35.75% | £3,478.48 |

| Total dividend tax | £4,528.81 |

Income tax on the salary (after personal allowance): £27,430 × 20% = £5,486. Total income tax bill for this director: £10,014.81.

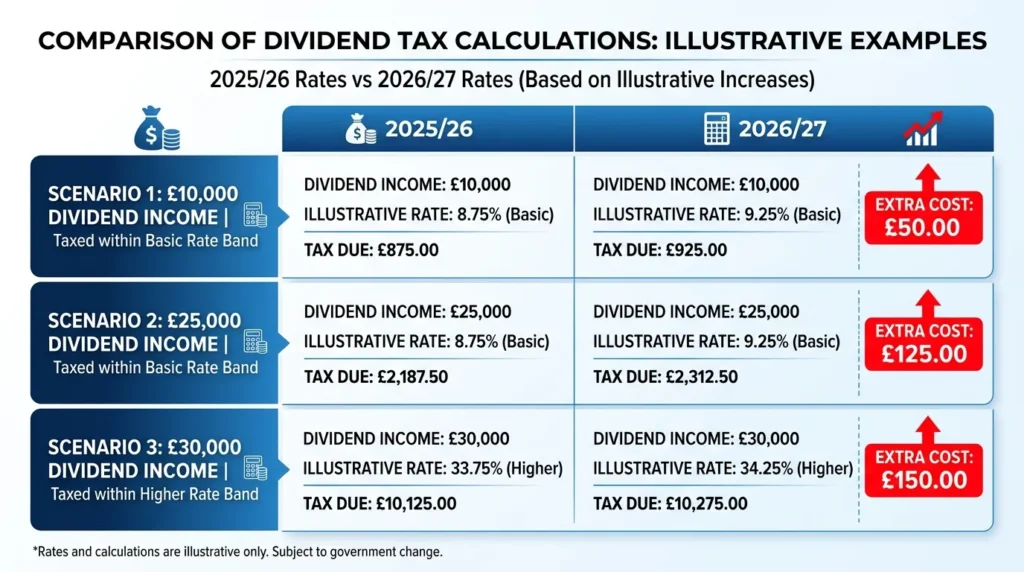

What the April 2026 Rate Rise Actually Costs You

The 2% rate increase sounds modest. In cash terms:

| Dividend income in band | Extra tax in 2026/27 vs 2025/26 |

|---|---|

| £10,000 (basic rate) | £190 more |

| £25,000 (basic rate) | £490 more |

| £37,700 (full basic rate band) | £754 more |

| £10,000 (higher rate) | £190 more |

| £30,000 (higher rate) | £570 more |

Anyone drawing dividends across both bands could pay up to £2,492 more this year than in 2025/26. If your remuneration plan was built on last year’s rates and hasn’t been reviewed, that gap won’t sort itself out.

How and When to Report Dividend Income to HMRC

Dividend income above the £500 allowance is taxable. You report it via a Self Assessment tax return.

You need to register for Self Assessment if any of these apply:

- Your total dividend income exceeds £10,000 in the tax year

- You already file a Self Assessment return and have any taxable dividend income

Key deadlines for the 2026/27 tax year:

- 31 October 2026 — paper return deadline

- 31 January 2027 — online return deadline and payment deadline

Miss these dates and HMRC issues automatic penalties starting at £100, which escalate quickly. For a full breakdown of what happens if you file late, see the guide to late Self Assessment penalties.

If you hold dividend-paying shares inside a pension or ISA, those dividends do not go on your tax return. The wrapper handles the tax treatment separately.

5 Ways to Reduce Your Dividend Tax Bill in 2026/27

1. Use Your ISA Allowance First

Dividends earned inside a Stocks and Shares ISA are completely exempt from dividend tax — at any rate band, for any amount. You can invest up to £20,000 per year across your ISAs. Any dividend income from shares or funds held inside the wrapper is tax-free permanently. For investors with growing portfolios, this is the most straightforward way to eliminate dividend tax entirely over time.

2. Make Pension Contributions

Pension contributions increase your basic rate band. A £10,000 pension contribution shifts the basic rate threshold from £50,270 to £60,270. If your dividends were spilling into the higher rate band, some of them fall back into the basic rate band — reducing the rate on that portion from 35.75% to 10.75%. The saving on £10,000 moving between bands in 2026/27 is £2,500.

3. Transfer Shares to Your Spouse or Civil Partner

Each UK taxpayer has their own personal allowance (£12,570) and dividend allowance (£500). If your spouse or civil partner has unused allowances or pays a lower rate of tax, transferring shares to them can substantially reduce the household tax bill on those dividends. The transfer must be genuine — HMRC looks at whether the shares represent a real economic interest — but the strategy is legal and widely used.

4. Optimise Your Salary and Dividend Split

The right salary level for most directors depends on two things: preserving state pension entitlement and avoiding unnecessary employer National Insurance contributions. Setting salary at the secondary NI threshold (£9,100) avoids employer NICs while keeping entitlement intact. Salary above that triggers employer NICs at 15%, which erodes the tax advantage of incorporation fast.

With dividend rates now 2 points higher, the optimal split has shifted for many directors. If you haven’t recalculated your numbers since April 2026, it’s worth doing so. For a broader breakdown of tax efficiency across business structures, the sole trader vs limited company comparison for 2026/27 shows which structure costs less at different income levels.

5. Time Your Dividends Carefully

A dividend declared on 5 April 2026 falls into the 2025/26 tax year and attracts the old rates. One declared on 6 April 2026 attracts 2026/27 rates. Going forward, that same logic applies: if you expect lower income next year — through reduced profits, a career change, or retirement — delaying dividends until after April 2027 could save a material amount.

Directors can also spread dividends across two tax years to stay within the basic rate band in both, rather than crossing into the higher rate band in one. This requires forward planning, not last-minute declarations.

Frequently Asked Questions

Are dividends taxed twice in the UK? In effect, yes. A limited company pays Corporation Tax on profits before any dividends are issued — currently 19% on profits up to £50,000, or 25% above £250,000. Dividends distributed to shareholders are then taxed again at personal dividend rates. The rates are set lower than standard income tax specifically to partially account for this double charge.

Do I pay National Insurance on dividends? No. Dividends are not subject to National Insurance Contributions, either for the company or the individual shareholder. That remains one of the core advantages of drawing income as dividends rather than salary, even after the 2026 rate increases.

What if I receive no salary — only dividends? You can still use the full personal allowance of £12,570 against dividend income. That gives you an effective tax-free threshold of £13,070 (£12,570 personal allowance plus £500 dividend allowance). Dividends above that are taxed at 10.75% if total income stays below £50,270.

Do Scottish income tax rates affect dividend tax? No. Dividend tax is set by Westminster and applies at the same rates across the whole of the UK. Scottish income tax only covers earned income, rental income, and most savings income — not dividends. A director based in Edinburgh pays the same 10.75%, 35.75%, and 39.35% dividend rates as one based in London.

The Bottom Line

The UK dividend tax rates for 2026/27 are confirmed at 10.75%, 35.75%, and 39.35%. The £500 allowance is unchanged. Both the basic and higher rates rose by 2 percentage points on 6 April 2026.

The rise is not ruinous, but it’s not trivial either. A director drawing £35,000 in dividends pays around £690 more this year than in 2025/26. Anyone near the higher rate threshold is more exposed, and anyone who hasn’t reviewed their salary and dividend structure is likely paying more than they need to.

ISAs, pension contributions, and a proper salary split are the three levers that make the most difference. Use them before 5 April 2027.

{kind=link}