If your business spent money this year trying to solve a technical problem, you may be sitting on a tax refund you don’t know about.

R&D tax credits let UK companies claim back part of what they spent on research and development. The relief comes as a reduction in your corporation tax bill, or as a cash payment from HMRC if you made a loss. Either way, it’s real money — not a deduction buried somewhere that barely moves the needle.

Here’s the catch. The rules changed in April 2024. Two old schemes were scrapped and replaced with one merged scheme, plus a separate top-up for loss-making companies doing heavy R&D. A lot of guidance online still quotes the old rates. If you’re working off outdated numbers, your claim will be wrong.

This guide covers what qualifies, which scheme applies to you, how much you can actually expect back, and the exact steps to file. If you’re still getting your business expenses organised before tax season, that’s worth sorting first — clean records make an R&D claim far easier to build.

What Are R&D Tax Credits

R&D tax credits are a UK government incentive. They reward companies for spending money trying to advance science or technology — even when the project doesn’t work out.

The relief isn’t a grant. You don’t apply for funding upfront. Instead, you claim it after the fact, through your Corporation Tax return, based on what you already spent.

Two things happen with the relief, depending on your scheme and your profit position:

- It reduces your Corporation Tax bill

- Or it pays out as cash, if you’re loss-making

The scheme was introduced in 2000. It’s been through several rounds of changes since, with the biggest overhaul landing on 1 April 2024.

Do You Qualify

Qualifying for R&D tax credits comes down to one test: did you try to resolve a scientific or technological uncertainty that a competent professional in your field couldn’t easily work out?

That’s it. No lab coat required.

What Counts as R&D

HMRC’s definition is broader than most business owners assume. You don’t need to be inventing something from scratch. Improving an existing product, process, or piece of software counts, as long as the work involved genuine technical uncertainty.

Real examples that typically qualify:

- A software company building a new way to process data at scale, where the approach wasn’t obvious from existing tools

- A manufacturer redesigning a production process to cut waste, where the outcome wasn’t guaranteed

- A food business reformulating a product to remove an allergen while keeping shelf life and texture stable

- A construction firm developing a new method to meet a structural requirement on a difficult site

What Doesn’t Count

Some areas are excluded outright. Work in arts, humanities, and social sciences — including economics — doesn’t qualify, regardless of how innovative it feels. Routine testing, cosmetic changes, and applying existing knowledge in the obvious way also won’t pass HMRC’s test.

One detail that surprises people: a failed project still qualifies. If you tried to solve the uncertainty and it didn’t work, the attempt is what matters, not the result.

Which Scheme Applies to You in 2026

For accounting periods starting on or after 1 April 2024, the old SME scheme and the old RDEC scheme were replaced. Most companies now claim under one of two routes.

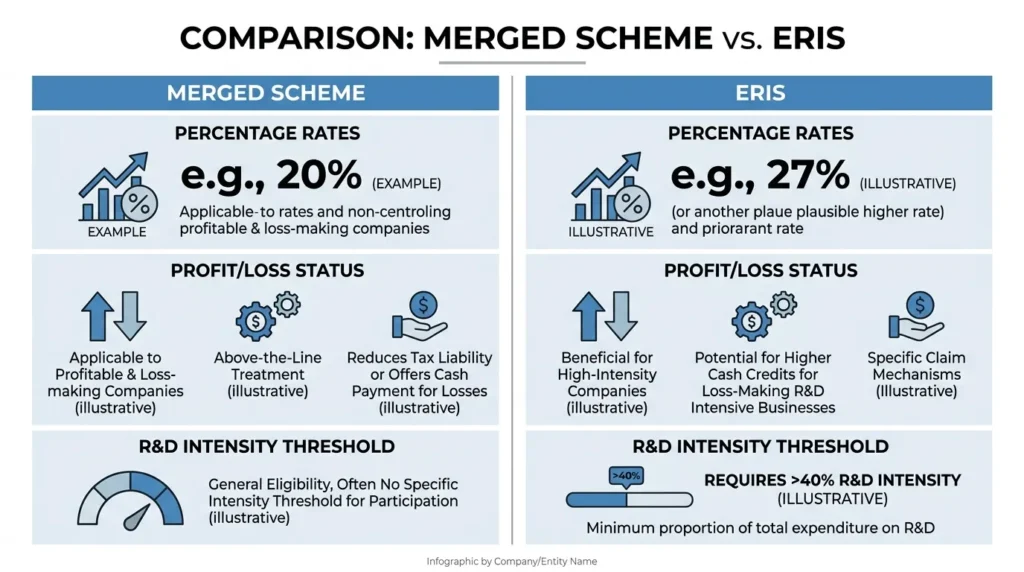

The Merged Scheme

This is the default for most SMEs and all large companies now. It works as an above-the-line credit, currently set at a 20% gross rate on qualifying R&D spend.

The credit is taxable. Once tax is applied, the typical net benefit lands between 15% and 16.2% of your qualifying expenditure, depending on your Corporation Tax position.

ERIS — Enhanced R&D Intensive Support

ERIS exists for a narrower group: loss-making SMEs where R&D spend makes up a large share of total costs.

To qualify, your qualifying R&D expenditure needs to represent 30% or more of your total expenditure. This threshold was lowered from 40% specifically to bring more small, R&D-heavy businesses into scope.

Under ERIS, the benefit is significantly better. You get an extra 86% deduction on qualifying costs, plus a payable credit worth 14.5% of your surrenderable loss. Combined, that works out to an effective benefit of up to 27% of qualifying spend.

You cannot claim both schemes on the same expenditure. It’s one or the other, based on your profit position and R&D intensity.

The SME Size Test

To be treated as an SME for R&D purposes, you and any connected companies need to fall under these limits:

- Fewer than 500 employees

- Either an annual turnover under €100 million, or a balance sheet under €86 million

If you’re unsure whether you count as a limited company or a different structure for tax purposes, that distinction matters here — only companies subject to UK Corporation Tax can claim either scheme. A company doesn’t need to be turning a profit to claim. Being in a loss position doesn’t block eligibility.

How Much Is It Actually Worth

Numbers help more than percentages here. Take a company spending £100,000 on qualifying R&D in one year.

Under the merged scheme, the gross credit is £20,000. After tax is applied at the standard rate, the net benefit typically comes out around £15,000 to £16,200.

Under ERIS, the same £100,000 spend could return up to £27,000 — nearly double, but only available to loss-making, R&D-intensive companies that meet the 30% threshold.

The Payable Credit Cap

If you’re claiming a payable cash credit, HMRC caps how much you can receive. The cap is set at £20,000 plus 300% of the company’s total PAYE and NIC liability for the period.

In plain terms: the smallest claims are protected. A company receiving a payable credit under £20,000 in a 12-month period won’t be affected by the cap at all. Above that, your PAYE and NIC bill becomes the limiting factor — so a company with very few employees on payroll but a large R&D claim could find the cap restricts what’s actually paid out.

There are exemptions where employees are involved in creating or managing intellectual property, so it’s worth checking your specific position rather than assuming the cap applies in full.

What Costs Qualify

Not every cost linked to a project counts. HMRC allows specific categories:

- Staff costs — salaries, employer NIC, and pension contributions for staff directly working on the R&D

- Externally provided workers (EPWs) — agency staff working under your direction on the project

- Software and cloud computing costs — licences and cloud costs used directly for the R&D, a category expanded to include data acquisition and cloud computing costs for periods starting on or after 1 April 2023

- Consumables — materials used up during the R&D process

- Subcontracted R&D costs — payments to subcontractors carrying out qualifying work on your behalf

The Subcontracting Rule Flip

This is one of the most overlooked changes from 2024. Under the old rules, subcontractors doing R&D work could often claim the relief themselves.

Under the merged scheme, that’s reversed. The company commissioning the R&D — not the subcontractor doing the work — is generally the one entitled to claim. If you outsource technical development work, check who holds the claim rights under your current contracts. Getting this wrong is a common reason claims get challenged.

How to Claim — Step by Step

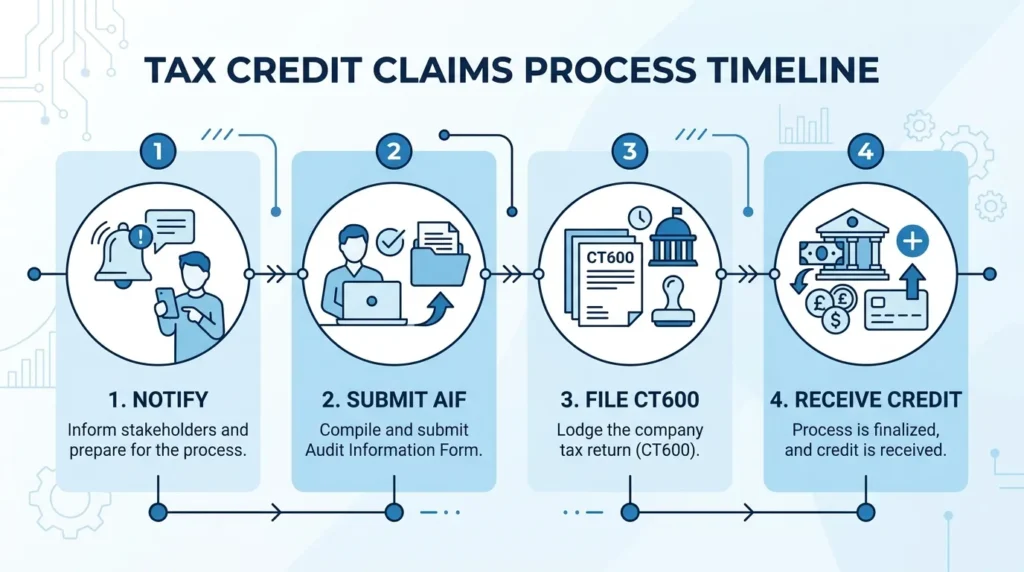

- Check if you need to notify HMRC in advance. First-time claimants, and companies that haven’t claimed in the last three years, generally need to notify HMRC before the claim window opens.

- Submit the Additional Information Form (AIF). This digital form has to be filed before you submit your Company Tax Return. It sets out your projects, costs, and the technical case for why the work qualifies. Skip this step and HMRC will strip the claim from your return automatically — there’s typically no grace period.

- File your CT600. Your R&D claim is included as part of your Corporation Tax return, referencing the AIF you’ve already submitted.

- Receive your credit or reduction. Depending on your scheme and profit position, this arrives as a reduced tax bill, a cash payment, or a combination of both.

You can also claim retrospectively. The standard deadline is two years from the end of the accounting period you’re claiming for. Miss that window and the claim is gone — there’s no extension process.

If you’re catching up on filings generally, it’s worth reviewing your wider self assessment tax return deadlines at the same time, since R&D claims often surface during a broader review of the business’s tax position.

Common Mistakes That Trigger HMRC Enquiries

HMRC has tightened scrutiny on R&D claims significantly. A few mistakes show up repeatedly:

- Missing the AIF — still the single most common reason claims get rejected outright

- Claiming the wrong scheme — applying the 27% ERIS rate without meeting the 30% intensity threshold is a frequent and costly error

- Weak technical narrative — vague descriptions like “we improved the product” don’t meet HMRC’s evidence bar; the claim needs to explain the specific uncertainty and how you tried to resolve it

- Treating routine work as R&D — standard customisation or applying well-known techniques doesn’t qualify, even if it was time-consuming

Getting flagged for an enquiry doesn’t just delay payment. It can lead to a clawback of relief already paid, plus the time cost of responding to HMRC’s questions.

Should You Use a Specialist or Claim Yourself

Smaller, more straightforward claims are sometimes manageable in-house, particularly if your accountant already has a clear picture of your costs and project work.

That said, R&D claims sit in an unusual spot — they need both tax knowledge and a genuine technical understanding of the work itself. A specialist adviser earns their fee mainly through two things: building a technical narrative that holds up to HMRC scrutiny, and correctly identifying every qualifying cost, which is easy to underclaim if you’re doing this for the first time.

If your claim is small, your projects are simple to describe, and your accountant is comfortable with the AIF process, doing it yourself is realistic. For larger or more technically complex claims, the cost of getting it wrong — a clawback, an enquiry, lost time — usually outweighs the specialist’s fee.

Frequently Asked Questions

Can I claim if my project failed? Yes. What matters is that you genuinely tried to resolve a scientific or technological uncertainty. The outcome of the project doesn’t affect eligibility.

Can I claim if my business isn’t profitable? Yes. Loss-making companies can claim, and may receive a cash payment rather than a reduction in Corporation Tax. Loss-making, R&D-intensive SMEs may also qualify for the higher ERIS rate.

How far back can I claim? You can claim retrospectively for the previous two accounting periods. The deadline is two years from the end of the period you’re claiming for, with no extensions.

Does the R&D tax credit count as taxable income? Under the merged scheme, the credit is brought into account as taxable trading income. The net benefit figures already account for this.

Can a sole trader claim R&D tax credits? No. Both the merged scheme and ERIS are only available to companies subject to UK Corporation Tax. If you’re operating as a sole trader, you won’t be eligible under either scheme as things stand — this is one of several practical differences worth weighing when deciding between a sole trader and limited company structure.

Where This Leaves You

The rules changed substantially in 2024, and a lot of the small business guidance still in circulation hasn’t caught up. If you’re spending money trying to solve genuine technical problems — in software, manufacturing, food production, construction, or anywhere else — it’s worth checking whether that spend qualifies before you assume it doesn’t.

Start by mapping your qualifying costs against the categories above, confirm whether the merged scheme or ERIS applies to your situation, and get the Additional Information Form sorted before your filing deadline. If you’re newer to running a limited company and still setting up your tax processes, it’s worth reading alongside our guide on registering a company in the UK and understanding how Corporation Tax rates apply to your business overall.

{kind=link}