For the 2025 to 2026 tax year, you start paying the 40% higher rate of income tax once your taxable income goes above £50,270 in England, Wales and Northern Ireland. That figure hasn’t moved since 2021/22, and it isn’t moving again until at least April 2028. If your pay has crept up since then, even by a small annual raise, you may already be paying more tax than you think.

This guide sets out the exact 2025/26 figures, shows you the maths behind a real payslip, and walks through the legal ways to keep more of your income below the line.

What Is the Higher Rate Tax Threshold for the 2025/26 Tax Year?

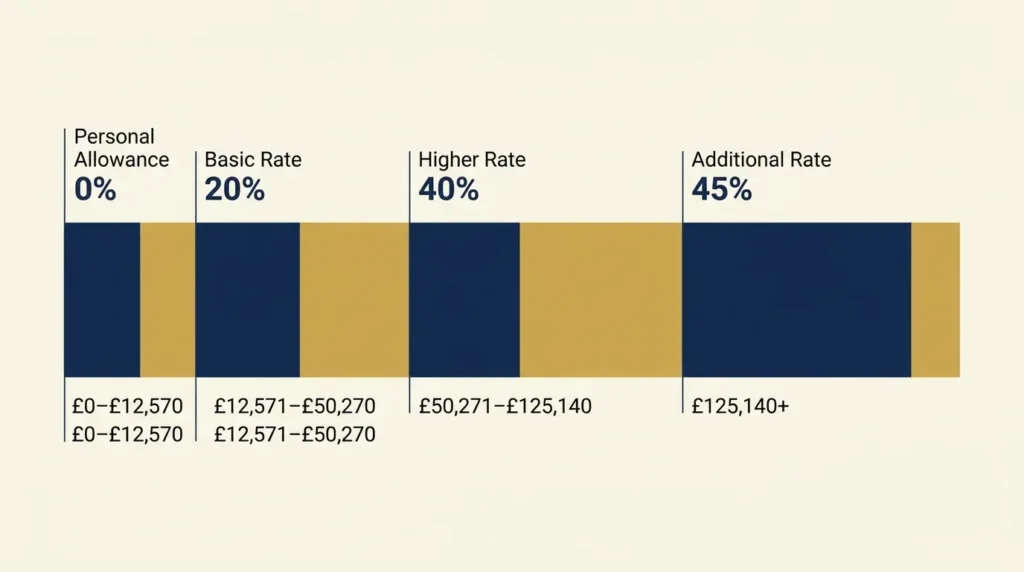

The higher rate threshold is £50,270 for 2025/26 across England, Wales and Northern Ireland. It’s made up of the £12,570 tax-free Personal Allowance plus the £37,700 basic rate band sitting on top of it. Once your taxable income passes £50,270, everything above that point is taxed at 40%, up to £125,140.

Quick Summary of Income Tax Bands 2025/26 (England, Wales & Northern Ireland)

| Band | Taxable Income | Rate |

|---|---|---|

| Personal Allowance | Up to £12,570 | 0% |

| Basic rate | £12,571 – £50,270 | 20% |

| Higher rate | £50,271 – £125,140 | 40% |

| Additional rate | Over £125,140 | 45% |

These figures are unchanged from 2024/25 and will stay unchanged through 2026/27, as confirmed at the 2025 Budget.

The “Frozen” Threshold Dilemma: Understanding Fiscal Drag

Fiscal drag happens when tax thresholds are held flat while wages rise with inflation. More of your pay ends up sitting above the frozen line each year, even though nothing about the tax rules themselves has changed.

The Personal Allowance and higher rate threshold have been frozen since 2021/22, and that freeze now runs to April 2031. The Office for Budget Responsibility expects the policy to pull millions more people into paying income tax altogether, and millions more into the higher rate band specifically, by the end of the decade. If you’ve had a “standard” pay rise over the past few years and never touched £50,270 before, this is very likely why you’re closer to it now — not because you’ve become dramatically better paid in real terms, but because the goalposts stopped moving.

How Is the 40% Higher Rate Tax Calculated?

You only pay 40% on the slice of income that sits above £50,270 — never on your whole salary. Income tax in the UK is marginal, so each band of your earnings is taxed at its own rate before the next band kicks in.

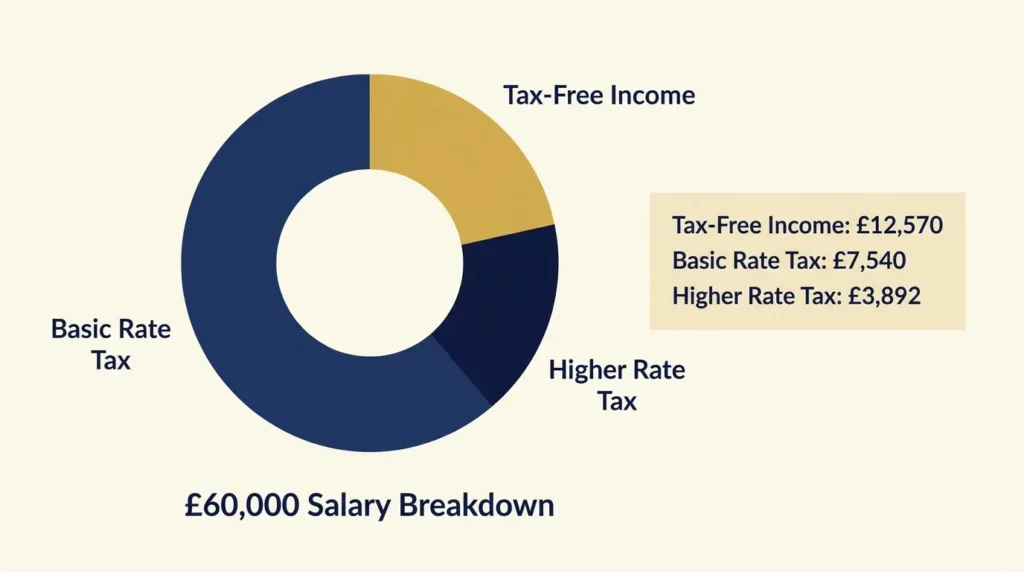

Step-by-Step Example of a £60,000 Salary

Take someone earning £60,000 in 2025/26 with a standard tax code and no other income:

- The first £12,570 is tax-free (Personal Allowance).

- The next £37,700 (£12,571 to £50,270) is taxed at 20% — £7,540.

- The remaining £9,730 (£50,271 to £60,000) is taxed at 40% — £3,892.

- Total income tax: £11,432.

Their marginal rate — the rate on their next £1 of income — is 40%. But their effective rate, tax as a share of the whole £60,000, works out at just over 19%. That gap is the single most misunderstood point in UK income tax, and it’s worth remembering before you turn down a pay rise or bonus out of fear it will “cost more than it’s worth.” It never does — only the amount above the threshold is ever touched by the higher rate.

If you’re weighing up how a pay rise, bonus, or move from employment into self-employment affects your take-home pay, our guide to sole trader tax in the UK breaks down how the same bands apply outside PAYE.

Personal Allowance Tapering: The 60% “Invisible” Tax Trap

Between £100,000 and £125,140, your effective marginal tax rate isn’t 40% or 45% — it’s 60%. This happens because your £12,570 Personal Allowance is withdrawn at £1 for every £2 you earn above £100,000, so you’re paying 40% tax on the income itself and losing tax-free allowance at the same time.

Worked example: Someone earning £110,000 has £10,000 of income above the £100,000 line. Their Personal Allowance shrinks by £5,000 (£1 for every £2), meaning £5,000 that used to be tax-free is now taxed at 40%, on top of the 40% already due on the extra £10,000 of salary. The combined effect on that £10,000 slice is a 60% marginal rate — for every extra £100 earned in this band, only £40 lands in your pocket.

This trap fully resolves at £125,140, where the Personal Allowance reaches £0 and the straightforward 45% additional rate takes over.

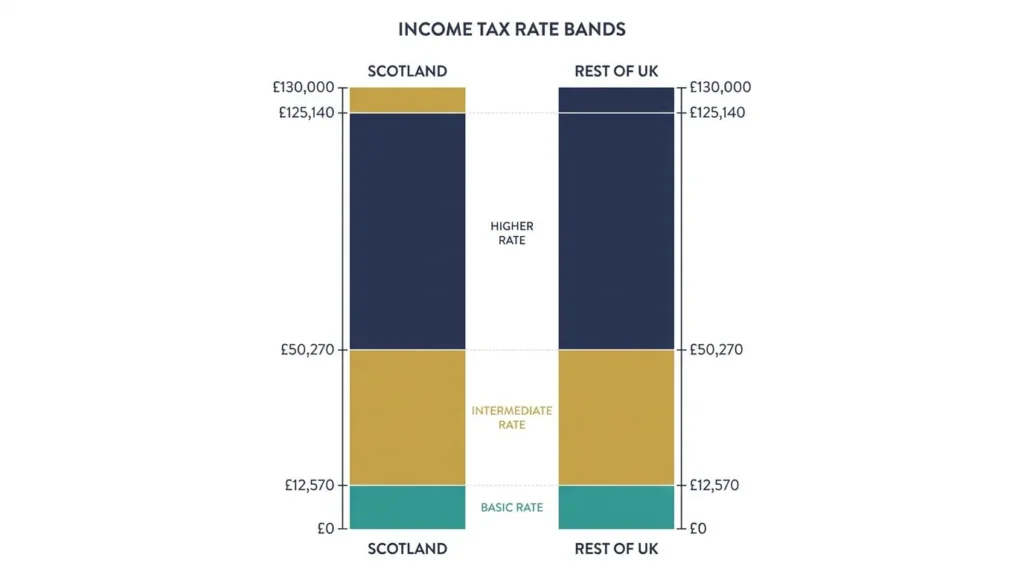

Regional Variations: Devolved Income Tax in Scotland vs. Rest of the UK

Scotland sets its own income tax rates and bands, and they diverge sharply from the rest of the UK once you pass roughly £27,500 of income. Wales, by contrast, has kept its rates aligned with England and Northern Ireland.

Scottish Income Tax Rates and Bands 2025/26

| Band | Taxable Income | Rate |

|---|---|---|

| Personal Allowance | Up to £12,570 | 0% |

| Starter rate | £12,571 – £14,876 | 19% |

| Basic rate | £14,877 – £26,561 | 20% |

| Intermediate rate | £26,562 – £43,662 | 21% |

| Higher rate | £43,663 – £75,000 | 42% |

| Advanced rate | £75,001 – £125,140 | 45% |

| Top rate | Over £125,140 | 48% |

The gap that catches most people out: Scotland’s higher rate starts at £43,662 — nearly £6,600 lower than the £50,270 threshold used in the rest of the UK. Between those two figures, a Scottish taxpayer pays 42% while someone with the same salary in England pays 20%, a 22-percentage-point difference on that slice of income. The Scottish Government has frozen the Higher, Advanced and Top rate thresholds in cash terms through 2026/27, so this gap is set to persist rather than narrow.

Scottish income tax only applies to non-savings, non-dividend income such as salary and self-employment profit. Interest and dividends are still taxed at the UK-wide rates wherever in the UK you live — our guide to UK dividend tax rates covers those figures in full.

Welsh Income Tax Rates

Wales has the power to set its own rates but has chosen to keep them aligned with England and Northern Ireland for 2025/26. So Welsh taxpayers use the same £12,570 Personal Allowance, £50,270 higher rate threshold, and 20% / 40% / 45% rates as the rest of the UK outside Scotland.

The Hidden Costs of Becoming a Higher Rate Taxpayer

Crossing £50,270 doesn’t just change the rate on your next pound of income. It quietly triggers several other changes that most guides gloss over.

Reduction in the Personal Savings Allowance (PSA)

Basic rate taxpayers can earn £1,000 of savings interest tax-free each year. Once you become a higher rate taxpayer, that allowance halves to £500. Additional rate taxpayers (over £125,140) get no Personal Savings Allowance at all. With savings rates still comparatively high, this is an easy trap for anyone with a large cash ISA-ineligible savings pot who tips into the 40% band for the first time.

The High Income Child Benefit Charge (HICBC) Taper

If you or your partner claims Child Benefit and either of you has an adjusted net income over £60,000, the High Income Child Benefit Charge starts clawing the benefit back. It tapers gradually: you repay 1% of the Child Benefit received for every £200 of income above £60,000, and the benefit is fully withdrawn once income reaches £80,000.

This is a common source of confusion, because a lot of older content still quotes the pre-April 2024 figures of £50,000 to £60,000. The current, correct 2025/26 range is £60,000 to £80,000, and the charge is based on the higher earner’s individual income — not combined household income. That means two parents each earning £59,000 (£118,000 combined) pay nothing, while a single-earner household on £65,000 faces a partial clawback.

Anyone newly liable for HICBC also needs to register for Self Assessment if they don’t already file one — our guide to completing a Self Assessment tax return covers the registration deadlines and how to avoid a late filing penalty.

Capital Gains Tax and Dividend Tax Implications

Whether you’re a basic or higher rate taxpayer also decides the rate you pay on gains and dividends outside your ISA and pension wrappers. Higher rate taxpayers pay a higher percentage on both capital gains and dividend income than basic rate taxpayers do on the same gain or payout. If you run a limited company and take income as dividends, or you’re planning to sell shares or a second property, it’s worth checking your total taxable income first — crossing into the higher rate band changes the rate on those gains too. Our guides to capital gains tax on business assets and paying yourself as a limited company director go through the calculations in detail.

How to Legally Avoid the 40% Higher Rate Tax Band

You can’t move the threshold, but you can legally reduce the taxable income that gets measured against it. Here are the four most effective, HMRC-approved levers.

1. Maximise Pension Contributions (SIPP and Workplace)

Pension contributions reduce your taxable income pound for pound, up to your annual allowance. If your salary is £54,000, contributing £3,730 into a pension brings your taxable income back down to £50,270 — below the higher rate threshold entirely. Contributions made through a workplace “net pay” scheme reduce your taxable income automatically before tax is calculated. Personal pension contributions made via “relief at source” get topped up by basic rate relief automatically, with higher rate taxpayers able to claim the extra relief through Self Assessment.

2. Utilise Salary Sacrifice Schemes (EVs, Cycle to Work)

Salary sacrifice lets you give up part of your gross salary in exchange for a non-cash benefit, such as extra pension contributions, an electric vehicle lease, or a Cycle to Work scheme. Because the sacrifice happens before tax and National Insurance are calculated, it reduces your taxable income more efficiently than making the same payment after tax.

3. Transfer Assets to a Spouse or Civil Partner

Assets — and the income they generate — can be transferred between spouses and civil partners without triggering a tax charge. If one partner is a basic rate taxpayer and the other is higher rate, moving income-generating assets like savings accounts or dividend-paying shares to the lower earner can mean that income is taxed at 20% instead of 40%.

4. Charitable Donations and Gift Aid

Gift Aid donations extend your basic rate band, which has the effect of pushing more of your income back under the 40% line. As a higher rate taxpayer, you can also claim back the difference between basic and higher rate tax on the donation through Self Assessment — our guide to filing a Self Assessment tax return explains how to claim this.

Quick summary — ways to reduce taxable income below £50,270:

- Increase workplace or personal pension contributions

- Use salary sacrifice for pensions, EVs or Cycle to Work

- Transfer income-generating assets to a lower-earning spouse

- Make Gift Aid donations and claim the higher rate relief

- Time bonuses or self-employed income across tax years where possible

If you’re self-employed or run a limited company, the same principles apply to profit rather than salary — see our guides on National Insurance for the self-employed and business expenses you can claim for further ways to legitimately reduce your taxable profit.

Frequently Asked Questions

What is the higher rate tax threshold for 2025/26? £50,270 in England, Wales and Northern Ireland. Income above this, up to £125,140, is taxed at 40%.

Has the 40% tax threshold changed for 2025/26? No. It’s unchanged from 2024/25 and frozen until at least April 2028.

Do I pay 40% on my whole salary once I cross £50,270? No. Only the portion of income above £50,270 is taxed at 40%. Everything below that is still taxed at 0% or 20%.

What is the higher rate threshold in Scotland? £43,662. Scottish taxpayers pay 42% on income between £43,663 and £75,000, a lower starting point and higher rate than the rest of the UK.

Does the Personal Allowance reduce once I’m a higher rate taxpayer? Not automatically. It only starts tapering once your income exceeds £100,000, reducing by £1 for every £2 earned above that, and reaching £0 at £125,140.

What is the High Income Child Benefit Charge threshold for 2025/26? £60,000, with the benefit fully withdrawn at £80,000. This is a common point of confusion, since the threshold was £50,000 before April 2024.

Can pension contributions bring me below the higher rate threshold? Yes. Pension contributions reduce your taxable income directly, so increasing contributions can take your taxable income back under £50,270 even if your gross salary is above it.

{kind=link}